Flywire (FLYW) Earnings Ramp Narrative Puts Fair Value Back In Focus

Flywire Corp. FLYW | 0.00 |

Recent commentary on Flywire (FLYW) centers on a projected ramp-up in earnings, with analysts pointing to the company’s scalable revenue model and improving operating leverage as key drivers behind higher estimates.

Flywire’s recent momentum has been strong, with a 1 day share price return of 3.91%, a 7 day share price return of 10.66%, and a 90 day share price return of 54.40%. However, the 3 year total shareholder return shows a decline of 43.49%, which highlights how recent optimism around profitability contrasts with a weaker longer term record.

If Flywire’s recent move has you thinking about where else earnings momentum might appear, it could be worth scanning 61 profitable AI stocks that aren't just burning cash for other potential opportunities in cash generating AI related businesses.

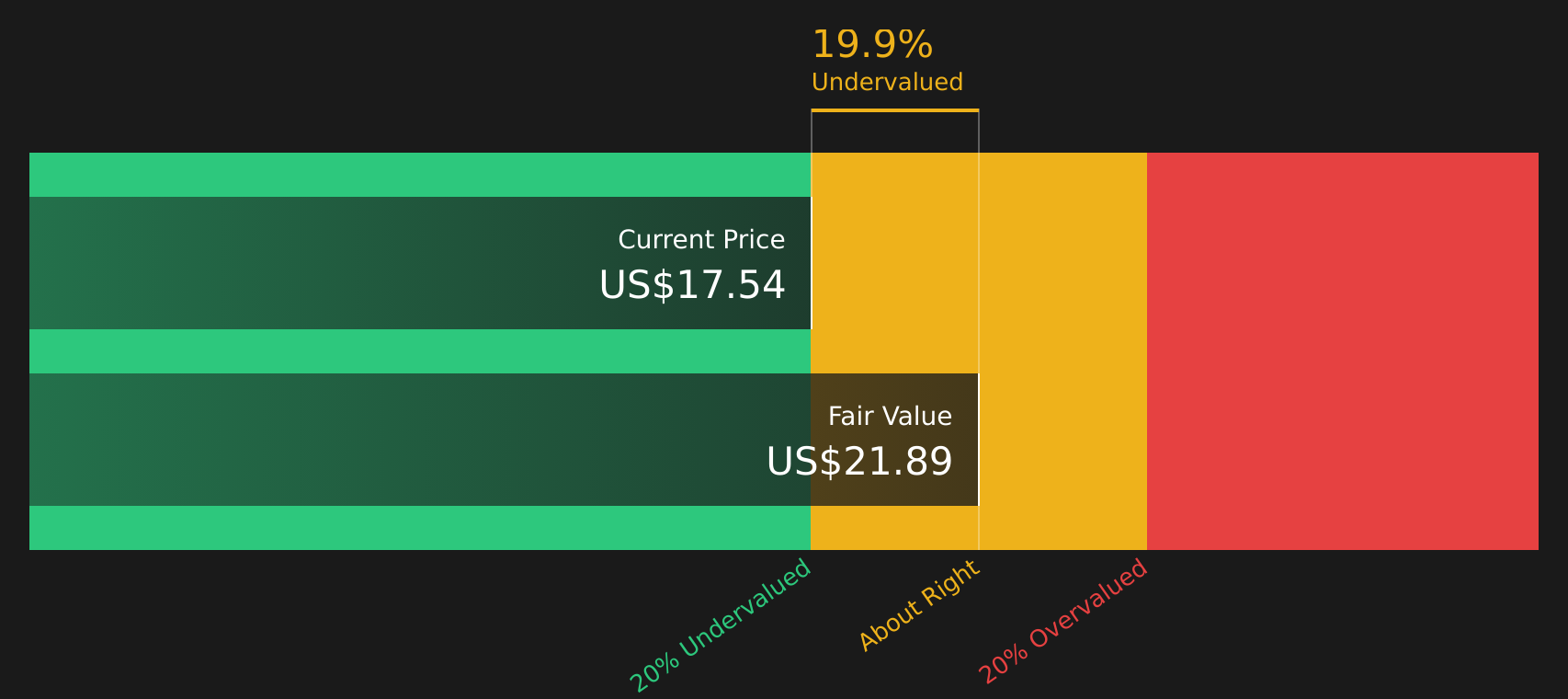

With Flywire shares up sharply in recent months and trading only modestly below analyst price targets, the key question is whether the stock is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 8% Overvalued

With Flywire shares closing at $17.54 against a narrative fair value of $16.31, the most widely followed view sees the stock pricing in slightly more optimism than its modeled cash flows support, using a 7.20% discount rate.

Ongoing investment in proprietary technology, AI-driven automation, and integration capabilities is yielding significant platform efficiencies (e.g., 25% operational cost improvements, 90% automated payment matching, and 40% automated customer service). These efficiencies underpin Flywire's ability to maintain or increase net margins and deliver stronger earnings leverage as scale increases.

Curious what kind of revenue trajectory and margin lift have to line up for that fair value number to make sense? The narrative leans heavily on compounding top line growth, a step change in profitability, and a future earnings multiple that has to stay above the sector norm. The exact mix behind that outcome might surprise you.

Result: Fair Value of $16.31 (OVERVALUED)

However, Flywire’s story could change quickly if tighter student visa policies affect education volumes, or if lower margin travel and B2B growth keeps overall profitability under pressure.

Another View: Flywire Through the SWS DCF Lens

While the most popular Flywire narrative points to an 8% premium to its $16.31 fair value, the SWS DCF model paints a different picture, suggesting the stock is trading about 23% below an estimated future cash flow value of $21.92. Which story feels more reasonable to you?

To see how that cash flow view is built up line by line, including the key assumptions that drive the gap to the narrative fair value, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Flywire for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and caution around Flywire has you on the fence, review the full picture and decide for yourself with 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Flywire?

If Flywire’s setup has sharpened your focus, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target potential mispricings by scanning companies that screen as attractively valued through 43 high quality undervalued stocks.

- Strengthen your income focus by reviewing stocks that feature in 9 dividend fortresses.

- Prioritize resilience by filtering for companies highlighted in 68 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.