Flywire (FLYW) Joins Russell Indices As Investors Revisit Whether The Stock Is Fairly Valued

Flywire Corp. FLYW | 0.00 |

Index additions draw fresh attention to Flywire stock

Flywire (FLYW) has been added to three Russell 2000 segments: the Value-Defensive, Defensive, and Growth-Defensive indices, a shift that can influence index fund flows and institutional interest.

Flywire's recent index additions arrive after a period of strong share price momentum, with a 30-day share price return of 30.21% and a 90-day share price return of 60.39% supporting a 1-year total shareholder return of 57.30%, despite a weaker 3-year total shareholder return.

If this kind of renewed attention has you thinking about where else capital is moving, it could be worth scanning a curated set of 20 top founder-led companies

After Flywire's sharp move and with the stock now close to the average analyst target, yet still at a wider discount to some intrinsic value estimates, where does a reasonable view of fair value actually sit?

Most Popular Narrative: 1.3% Undervalued

The most followed Flywire narrative pegs fair value at $19, a touch above the last close at $18.75, and leans heavily on long term expansion and efficiency assumptions.

Ongoing investment in proprietary technology, AI-driven automation, and integration capabilities is yielding significant platform efficiencies (e.g., 25% operational cost improvements, 90% automated payment matching, and 40% automated customer service), underpinning Flywire's ability to maintain or increase net margins and deliver stronger earnings leverage as scale increases.

Want to see what those efficiency gains really imply for Flywire? The narrative quietly leans on rising margins, faster earnings, and a richer future multiple to justify that fair value.

Result: Fair Value of $19 (UNDERVALUED)

However, there is still real scope for this Flywire narrative to crack if education volumes soften or if a higher growth travel and B2B mix continues to pressure margins.

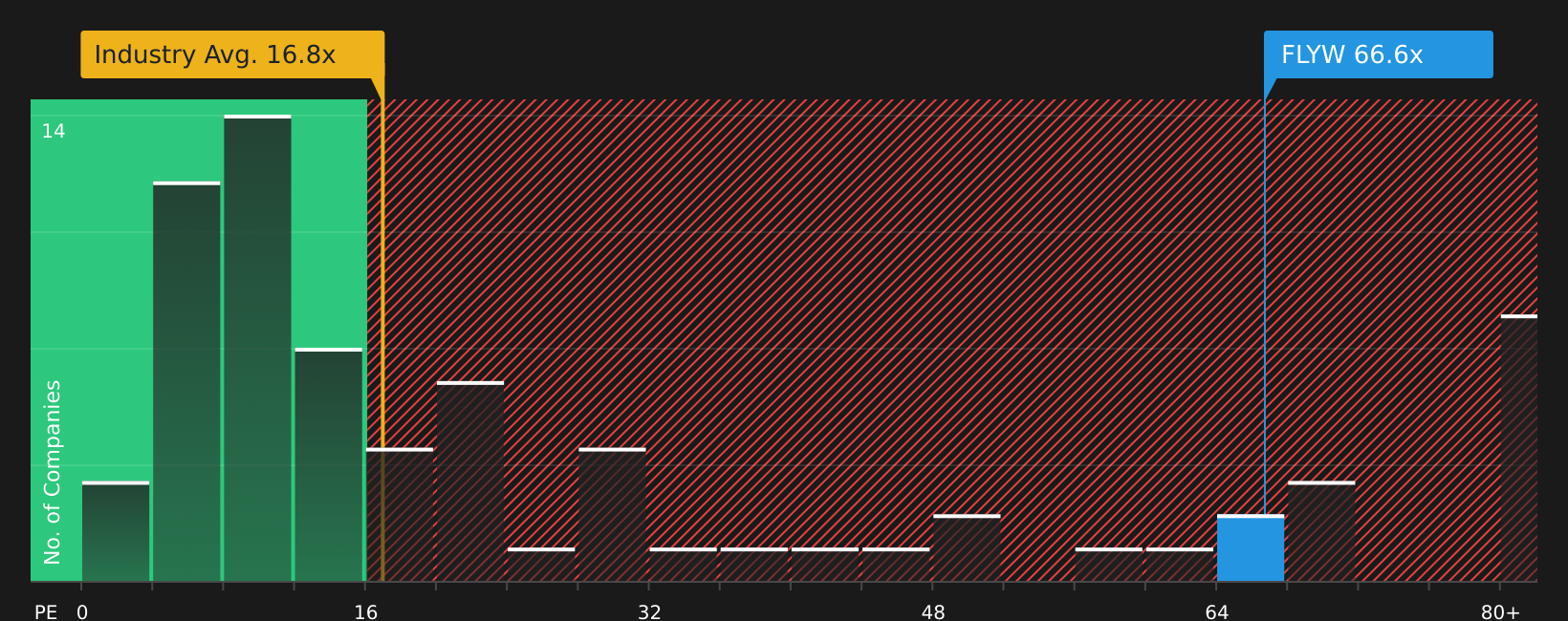

Another View: Flywire looks expensive on earnings multiples

Alongside the SWS DCF view that Flywire is trading about 14.7% below an estimate of its future cash flow value at $21.98, the earnings multiple picture is very different and much harsher.

Flywire currently trades on a P/E of 75.5x, compared with a fair ratio of 24x, a peer average of 14.2x and a US Diversified Financial industry average of 15.7x. That gap points to potential valuation risk if sentiment cools, so which yardstick do you trust more?

Next Steps

Torn between the optimism and the caution around Flywire right now, and keen to make up your mind quickly based on the full picture? It could be worth weighing both sides of the story with the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Flywire?

If Flywire has sharpened your focus on where capital might work harder, do not stop here. Broaden your watchlist with a few targeted ideas while conditions still suit.

- Spot potential mispricings early by scanning 44 high quality undervalued stocks that pair quality fundamentals with room for a re rate.

- Strengthen your income stream by reviewing 7 dividend fortresses offering higher yields with supporting fundamentals.

- Sleep easier at night by focusing on 73 resilient stocks with low risk scores that aim to keep downside risk more contained.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.