Ford (F) Valuation Check As EV Pivot, One Time Charge And Earnings Outlook Refocus Investor Attention

Ford Motor Company F | 12.44 12.44 | -2.12% +0.01% Post |

Ford Motor (F) is in focus after deciding against an all electric F-150 and recording a one time $19.5 billion charge tied to its EV pivot, just as it heads into closely watched earnings.

At a share price of $13.59, Ford has had a softer recent patch, with a 30 day share price return of 4.3% and a 7 day share price return of 1.6%. The upcoming earnings release, the recent dividend affirmation and the launch of the new Ford Energy battery storage unit are keeping attention on the stock, and a 1 year total shareholder return of about 58% points to momentum that has built over a longer horizon.

If Ford’s EV rethink has you reassessing the auto sector, this could be a good moment to scan beyond traditional manufacturers and check out 24 power grid technology and infrastructure stocks as a potential source of future growth themes.

With the shares near the average analyst price target and a 1 year total return close to 58%, the key question now is whether Ford’s EV reset and new energy push leave hidden value on the table, or if the market is already paying up for future growth.

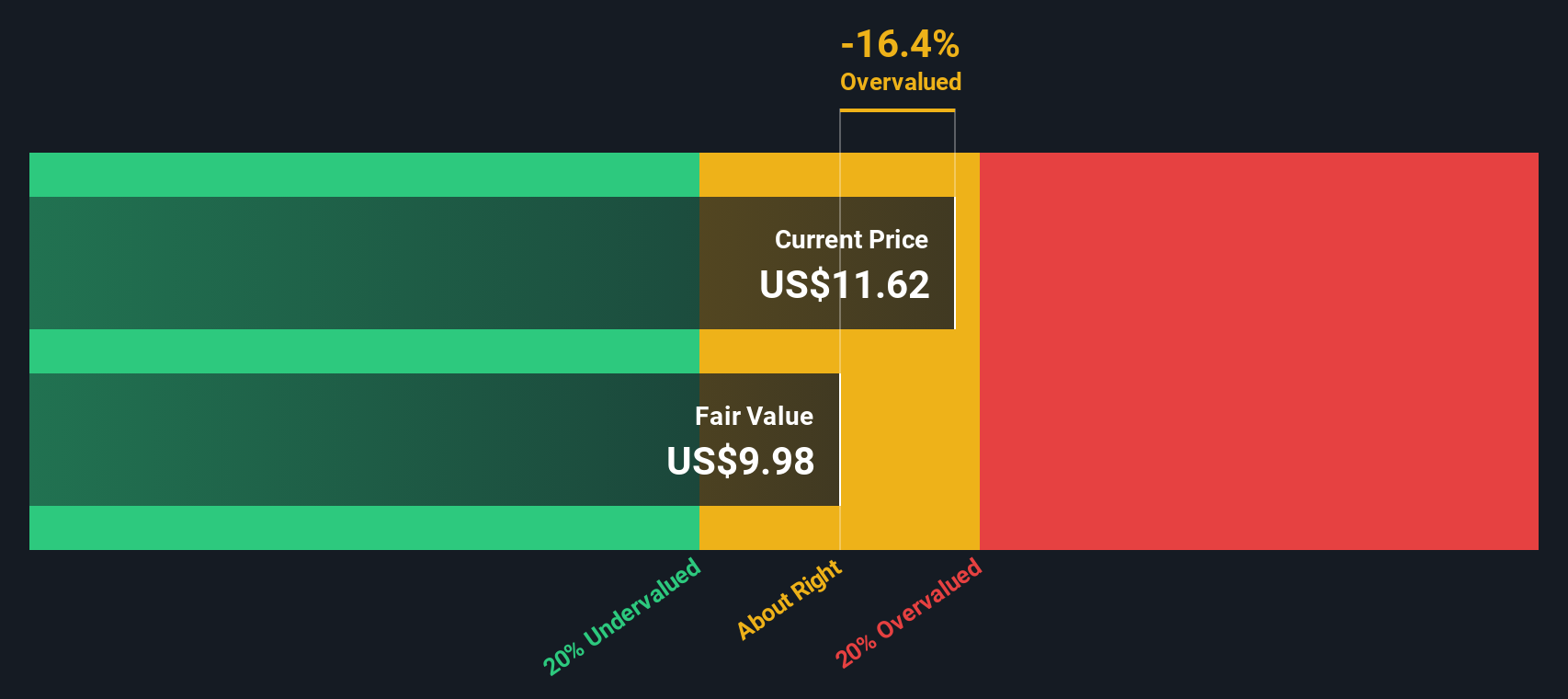

Most Popular Narrative: 1.2% Undervalued

At $13.59, Ford Motor is trading a touch below the most followed fair value estimate of $13.76, which is built using a 12.33% discount rate and long term cash flow assumptions.

Ford's ongoing transformation of its Ford Pro commercial platform, which emphasizes high-margin, recurring revenues from software, telematics, and aftermarket services, continues to outperform, with paid software subscriptions up 24% year-over-year and aftermarket approaching 20% of Pro EBIT. This shift toward recurring digital revenues supports structurally higher net margins and enhances earnings durability.

Want to see what is behind that recurring revenue story and higher margin view? The detailed narrative leans on specific revenue mix, margin and earnings bridge assumptions that are not obvious from the headline numbers.

Result: Fair Value of $13.76 (ABOUT RIGHT)

However, you still need to weigh the risk that tariff costs and a slower, more complicated EV rollout could pressure margins and challenge the current fair value case.

Another View: Cash Flows Paint A Harsher Picture

While the fair value narrative sits at about $13.76 per share, our DCF model takes a tougher line. It provides a future cash flow value estimate of roughly $9.90 per share. That gap suggests cash flow assumptions are less forgiving than the earnings-based story, so which do you put more weight on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ford Motor for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ford Motor Narrative

If you are not fully on board with these views or you simply prefer to test the numbers yourself, you can build a custom Ford story in just a few minutes, starting with Do it your way.

A great starting point for your Ford Motor research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas beyond Ford?

If this Ford analysis has sparked new questions, do not stop here. A broader watchlist can help you spot opportunities and manage risk more effectively.

- Target income first by checking companies in our 14 dividend fortresses that focus on higher yields with an eye on resilience.

- Hunt for quality at a sensible price through the 52 high quality undervalued stocks, built around companies with strong fundamentals that may not be fully appreciated.

- Stay one step ahead on downside risk by reviewing the 82 resilient stocks with low risk scores, which highlights businesses with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.