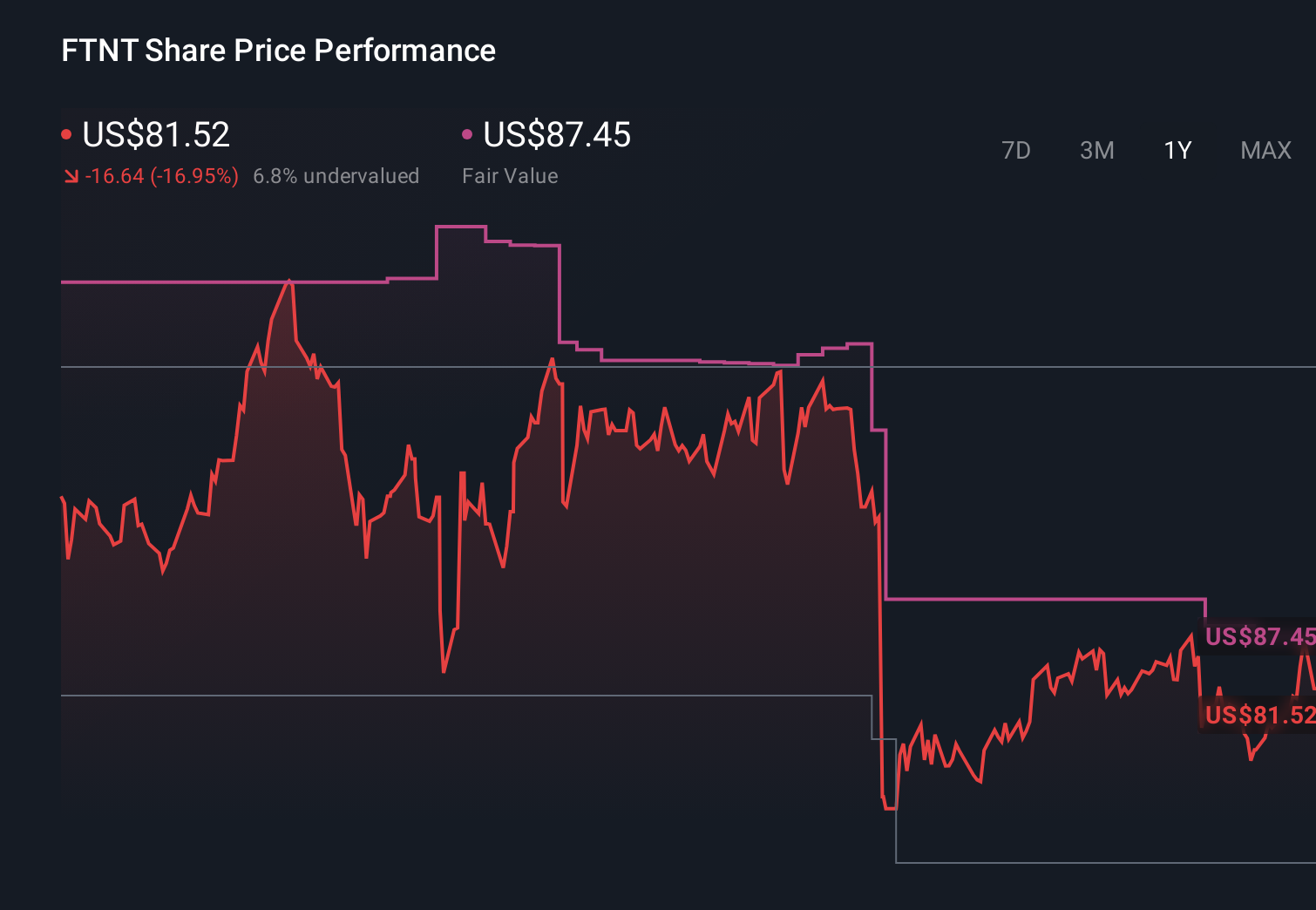

Fortinet (FTNT) Is Up 7.0% After Stronger 2026 Billings Outlook Amid Margin Debate

Fortinet, Inc. FTNT | 82.53 | +1.70% |

- In recent weeks, Fortinet reported quarterly earnings that exceeded consensus expectations and issued a fiscal 2026 billings growth outlook above prior forecasts, while also addressing margin pressures and hardware-model risks highlighted by JPMorgan and Wells Fargo.

- At the same time, Fortinet has maintained strong free cash flow generation and attracted a wide spread of analyst opinions, underscoring the debate around its hardware-centric model, evolving service mix, and exposure to emerging security threats.

- Now we’ll consider how stronger-than-expected billings guidance, alongside margin concerns, may reshape Fortinet’s existing investment narrative and risk-reward profile.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Fortinet Investment Narrative Recap

To own Fortinet, you need to be comfortable with a business that is still heavily tied to hardware while working to grow higher-margin security services. The latest earnings beat and stronger 2026 billings guidance support the near term upgrade cycle as a key catalyst, but they do not remove the central risk that growth may slow once this firewall refresh wave fades and margin pressure from hardware and infrastructure spending remains in focus.

The clearest recent signal for shareholders is Fortinet’s upgraded 2026 billings outlook, which came alongside record free cash flow and continued share repurchases under the US$10.25 billion buyback authorization. That combination reinforces the importance of execution on services and SASE as the company spends heavily on infrastructure and sales capacity, while the slow burn of the short thesis and concerns around hardware model risk keep the debate about Fortinet’s longer term position very much alive.

Yet behind the upbeat billings guidance, the risk that heavier hardware reliance could limit Fortinet’s flexibility is something investors should be aware of...

Fortinet's narrative projects $9.2 billion revenue and $2.4 billion earnings by 2028. This requires 13.1% yearly revenue growth and an earnings increase of about $0.5 billion from $1.9 billion today.

Uncover how Fortinet's forecasts yield a $87.04 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$9.7 billion by 2028, yet the latest billings outlook and ongoing margin concerns may either support that bullish view or force a reset, depending on how you weigh hardware dependence against fast growing SASE and AI driven services.

Explore 21 other fair value estimates on Fortinet - why the stock might be worth just $85.73!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Fortinet research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Fortinet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fortinet's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.