Franklin Resources (BEN) Valuation Check After Strong Recent Shareholder Returns

Franklin Resources, Inc. BEN | 26.63 26.63 | +0.76% 0.00% Post |

Event context and recent performance snapshot

Franklin Resources (BEN) has drawn fresh attention after recent trading, with the share price at $28.16 and total return figures of 18.3% year to date and 47.8% over the past year.

The recent 1-day share price return of 1.73% and 90-day share price return of 22.17% sit alongside a 1-year total shareholder return of 47.79%, suggesting momentum has been building rather than fading.

If Franklin Resources has caught your eye, this could be a good moment to widen your watchlist and check out 23 top founder-led companies as potential next ideas to research.

So with Franklin Resources trading near analyst targets yet still showing an intrinsic discount, is the current share price leaving you a margin of safety, or is the market already pricing in any future growth?

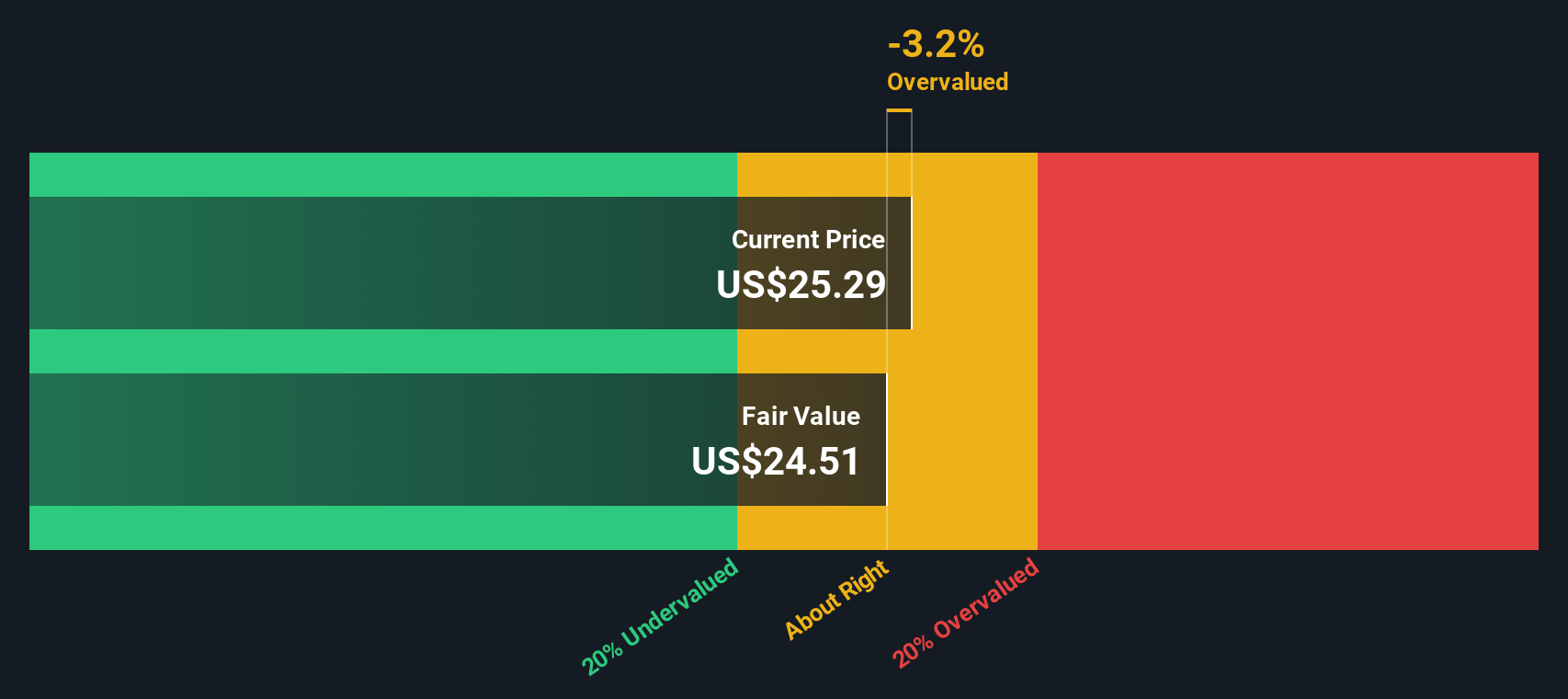

Most Popular Narrative: 13.9% Overvalued

Against the last close at $28.16, the most followed narrative pegs Franklin Resources' fair value at about $24.73, pointing to a valuation gap that hinges on how its business mix and expansion plans play out over time.

The integration of acquired platforms (e.g., Legg Mason, Apera, Putnam, Alcentra) has broadened Franklin's global product suite, especially in fixed income, ETFs, and alternatives. Cost synergies and improved distribution are anticipated to further drive net inflows and scale-driven efficiency, supporting long-term revenue and margin growth.

Curious what kind of earnings path and margin profile need to line up for that fair value to make sense? The narrative leans on specific revenue trends, profitability targets and a future valuation multiple that is very different from today. If you want to see exactly which assumptions carry the most weight in this story, the full narrative lays them out in black and white.

Result: Fair Value of $24.73 (OVERVALUED)

However, there are still watchpoints, including ongoing fee pressure and persistent net outflows at Western Asset Management, which could undercut the assumptions behind this fair value story.

Another way to look at valuation

The most popular narrative has Franklin Resources as about 13.9% overvalued against a fair value of $24.73, but our DCF model tells a different story, with fair value closer to $31.94 and the current $28.16 price sitting at a discount instead. Which set of assumptions do you find more convincing?

Build Your Own Franklin Resources Narrative

If you are not fully on board with either valuation view, or simply prefer to test your own assumptions with the numbers, you can build a custom Franklin Resources thesis in just a few minutes and Do it your way.

A great starting point for your Franklin Resources research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Franklin Resources is on your radar, do not stop there. Broaden your opportunity set with a few focused screens that can surface very different types of ideas.

- Target potential value opportunities by checking companies our screener tags as 51 high quality undervalued stocks so you are not relying on just one name or narrative.

- Zero in on income ideas by reviewing 14 dividend fortresses, especially if regular cash payouts matter as much to you as price movement.

- Prioritise resilience by scanning 83 resilient stocks with low risk scores and see which businesses currently line up with a more defensive risk profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.