Freeport McMoRan (FCX) Valuation After Analyst Upgrades And Earnings Estimate Revisions

Freeport-McMoRan, Inc. FCX | 0.00 |

Freeport-McMoRan (FCX) is back in the spotlight after analysts raised earnings estimates and upgraded their views. The stock still trades at a discount to peers, drawing fresh attention from investors.

Recent trading reflects that shifting sentiment. Despite a 5.22% one day share price decline to US$62.04, Freeport-McMoRan still posts a 54.48% 90 day share price return and a 56.40% one year total shareholder return. This indicates that momentum has been building rather than fading.

If this upgrade is prompting you to look across mining and metals, it could be a good time to scan other producers using our screen of 8 top copper producer stocks as potential ideas to research next.

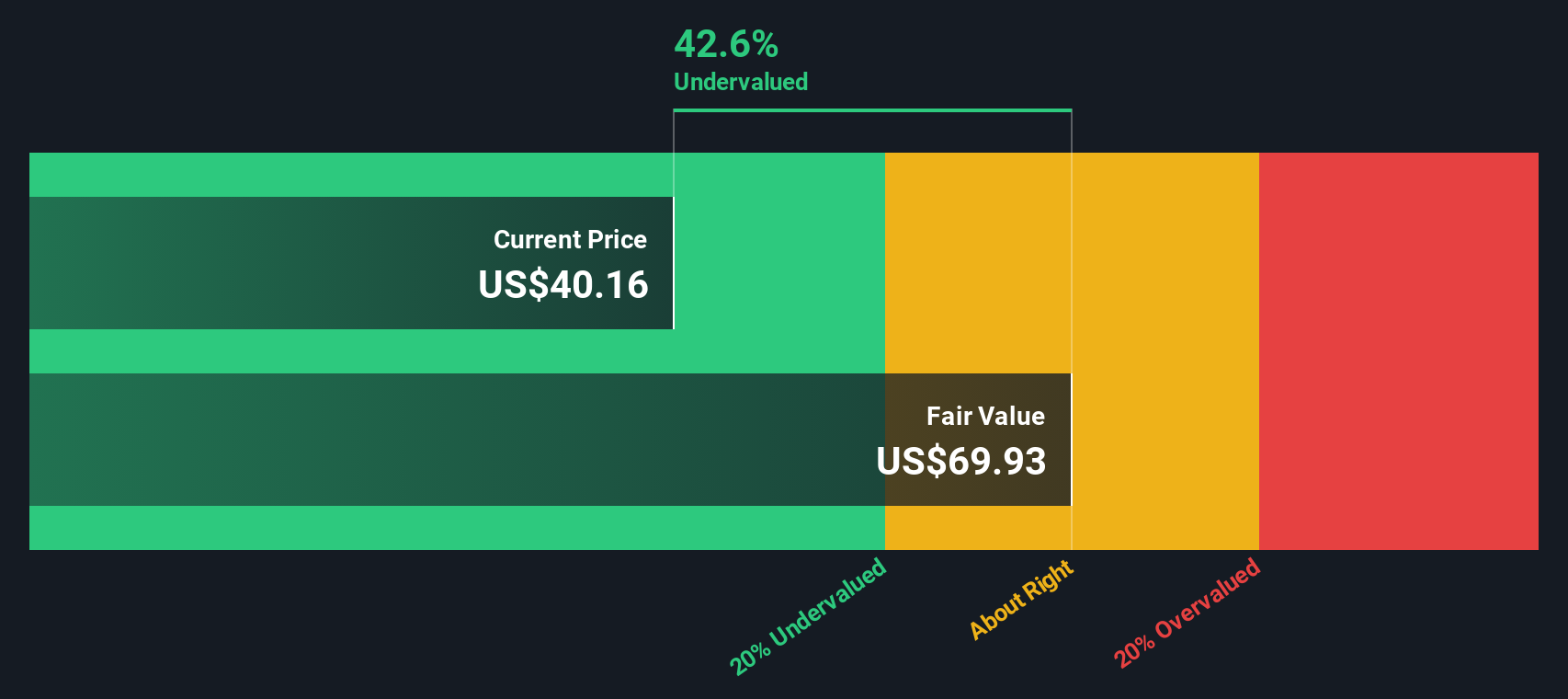

With earnings estimates moving higher, an intrinsic value suggesting a 27.52% discount and the share price only slightly below analyst targets, you have to ask: is Freeport-McMoRan still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 40.7% Overvalued

According to the most followed narrative, Freeport-McMoRan's fair value sits at $44.08, well below the last close of $62.04, which sets a cautious tone around valuation.

Global demand for copper, especially from EVs, AI, and green infrastructure

Grasberg mine in Indonesia and large-scale U.S. operations (e.g., Morenci, Bagdad)

U.S. legislation may classify copper as a "critical mineral", possibly introducing 10% tax credit

Want to see how this narrative gets from today’s earnings to that future valuation gap? It leans heavily on sustained revenue growth and a richer profit margin profile. Curious which long term earnings assumptions sit at the heart of that fair value and how they link to a higher future earnings multiple? The full narrative lays out those numbers in black and white.

Result: Fair Value of $44.08 (OVERVALUED)

However, this story can break if copper prices weaken, or if operational issues at key mines like Grasberg disrupt production and squeeze margins.

Another View: Cash Flows Point the Other Way

The popular narrative calls Freeport-McMoRan 40.7% overvalued at a fair value of $44.08, but our DCF model points in the opposite direction. On that view, the shares at $62.04 sit 27.5% below an estimated value of $85.59, which raises a very different question about upside potential.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Freeport-McMoRan for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Freeport-McMoRan Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to run your own checks, you can build a custom view in just a few minutes, starting with Do it your way.

A great starting point for your Freeport-McMoRan research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about sharpening your portfolio, do not stop with one stock. Use targeted screens to surface fresh ideas that actually fit your goals.

- Hunt for quality at a discount with our list of 55 high quality undervalued stocks, built to highlight companies where fundamentals and price appear out of step.

- Strengthen your income stream by reviewing 16 dividend fortresses, focusing on businesses built around higher yielding and consistent payouts.

- Prioritise resilience by scanning 84 resilient stocks with low risk scores, which filters for companies with lower risk scores so you can focus research where downside may be more limited.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.