Frontline (FRO) Is Up 8.7% After Profit-Fueled 50% Dividend Hike Is Earnings Quality Improving?

Frontline Plc FRO | 0.00 |

- Earlier in 2026, Frontline announced roughly a 50% dividend increase after reporting its strongest quarterly adjusted profit since 2004, helped by disrupted crude shipping routes following the effective closure of the Strait of Hormuz during the Iran conflict.

- This combination of record profitability and a sharply higher, but inherently variable, payout highlights how sensitive Frontline’s income profile is to sudden shifts in global trade flows.

- We’ll now explore how this profit-fueled dividend increase might reshape Frontline’s investment narrative, especially its perceived earnings resilience.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Frontline Investment Narrative Recap

To own Frontline today, you need to believe that tight tanker supply and shifting crude trade routes can continue to support strong spot earnings, even as the global energy transition and regulatory pressures cast a long shadow over future oil demand. The recent profit spike linked to the Strait of Hormuz disruption has clearly amplified the short term earnings catalyst: elevated day rates. It also underlines the biggest risk right now, which is how quickly those rates could normalize if trade routes unclog.

The most relevant recent announcement here is Frontline’s Q1 2026 dividend of US$1.55 per share, coming off revenue of US$929.33 million and net income of US$559.12 million. Set against a history of rapidly rising and falling payouts, this latest increase reinforces how tightly the dividend is tethered to spot-market earnings, which are themselves driven by exactly the sort of sudden route disruptions that boosted this quarter’s results.

Yet behind today’s exceptional profits and dividend, there is a risk investors should be aware of if tanker rates retreat faster than expected...

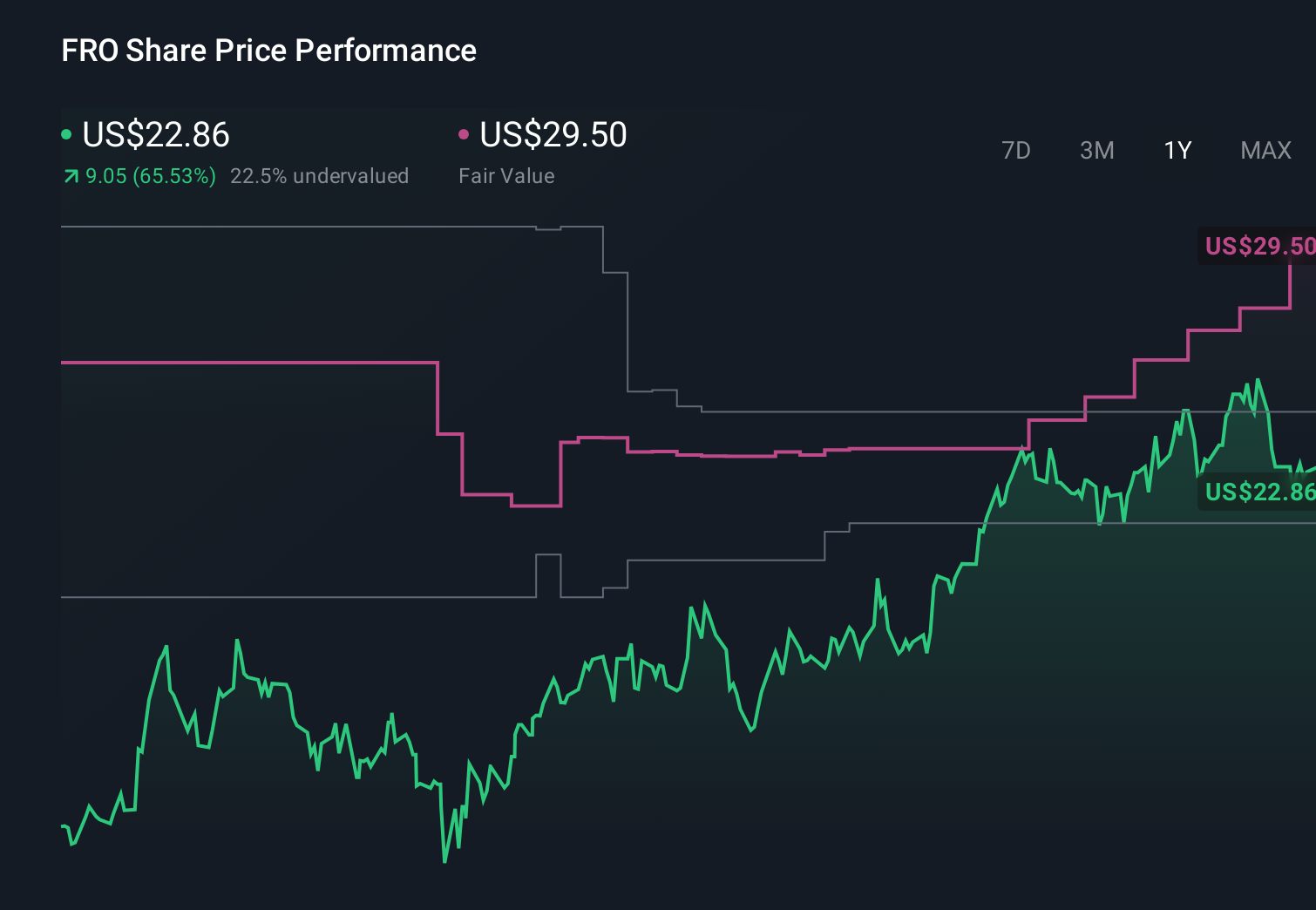

Frontline's narrative projects $1.6 billion revenue and $697.7 million earnings by 2029. This implies a 7.1% yearly revenue decline but an earnings increase of about $318.6 million from $379.1 million today.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 11% upside to its current price.

Exploring Other Perspectives

The lowest ranked analysts paint a much more cautious picture, assuming revenue could fall toward about US$1.3 billion and earnings near US$492.6 million, so if you are focusing on how fragile trade routes and fleet age could pressure margins, this news might eventually shift those expectations in ways that are still far from settled.

Explore 6 other fair value estimates on Frontline - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Frontline research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.