FuelCell Energy (FCEL) Could Be 21% Undervalued As Siemens And Fit Energy Deals Lift Views

FuelCell Energy, Inc. FCEL | 0.00 |

FuelCell Energy (FCEL) is back in focus after investors reacted to a new Siemens collaboration on large fuel cell projects and a sizeable Fit Energy power supply agreement, supported by several analyst upgrades.

Those Siemens and Fit Energy deals arrive after a volatile run for FuelCell Energy, with the share price falling 14.8% in the last day and 25.0% over the week but still posting a 138.1% 90-day share price return and a 234.5% 1-year total shareholder return, suggesting strong momentum after a weak multi year total shareholder return.

If you are watching how clean energy partnerships are reshaping power markets, it could be worth broadening your watchlist to include 35 power grid technology and infrastructure stocks

After FuelCell Energy’s sharp swing lower and a US$17.26 share price now sitting well below an average analyst target of about US$22.83, the real tension is where fair value actually sits in that gap.

Most Popular Narrative: 21.5% Undervalued

With FuelCell Energy trading at $17.26 against a widely followed fair value of $22, the current pullback sits in clear contrast to that narrative.

The partnership with Diversified Energy to deliver up to 360 megawatts to data centers in Virginia, West Virginia, and Kentucky is anticipated to drive significant revenue growth as it positions FuelCell Energy at the forefront of powering AI and high-performance computing sectors. The joint development agreement with Malaysia Marine and Heavy Engineering to co develop large scale hydrogen production systems is expected to enhance revenue by expanding FuelCell Energy's market presence in Asia, New Zealand, and Australia, tapping into growing demand for hydrogen.

Want to understand why this fair value sits meaningfully above today’s price? The core storyline leans heavily on fast compound revenue growth, margin repair and a richer future earnings multiple. The tension lies in how those assumptions play out against continued losses and heavy project execution demands. The numbers behind that gap are where the narrative really gets interesting.

Result: Fair Value of $22 (UNDERVALUED)

However, FuelCell Energy’s narrative still hinges on reducing sizable losses and actually converting its 4 GW commercial pipeline into firm, profitable projects, which may prove challenging.

Another View on FuelCell Energy’s Valuation

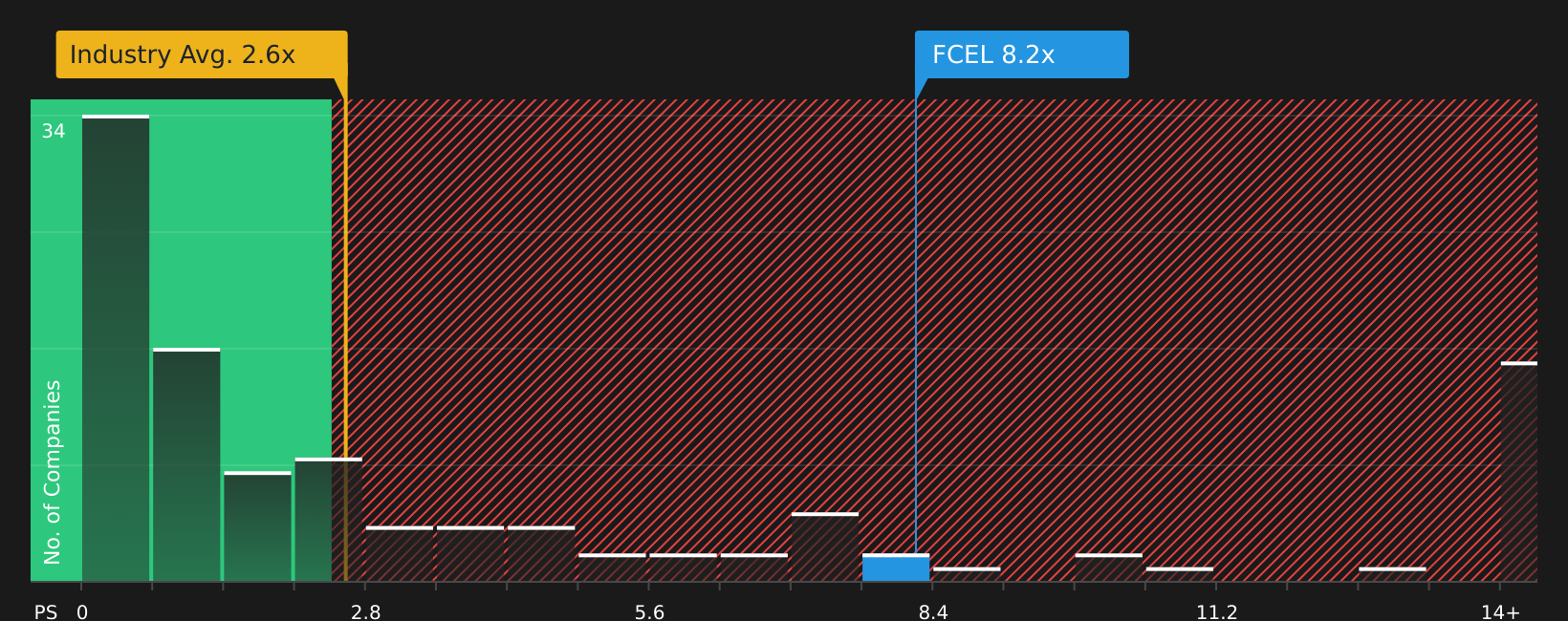

The analyst fair value of $22 for FuelCell Energy leans on strong revenue forecasts and a richer future P/E, yet the current market is already paying a P/S of 8.2x versus 2.7x for the US Electrical industry and a fair ratio of 2.9x. This points to a much more expensive picture. For investors, that gap raises a simple question: is the story strong enough to justify such a premium?

Next Steps

If the mixed sentiment on FuelCell Energy has you torn, take a closer look at both sides of the story and weigh the 1 key reward and 3 important warning signs

Looking for more investment ideas beyond FuelCell Energy?

If you stop with FuelCell Energy, you could miss opportunities that fit your goals even better. Consider putting a few more quality ideas on your radar.

- Target potential mispricings by scanning companies that combine quality fundamentals with attractive valuations through 49 high quality undervalued stocks.

- Build a steadier income stream by reviewing companies with strong payout profiles using the 8 dividend fortresses.

- Prioritize resilience by focusing on businesses with stronger financial footing via the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.