FuelCell Energy (FCEL) Stock Could Be Overvalued On EXIM Backed Growth Plans

FuelCell Energy, Inc. FCEL | 0.00 |

FuelCell Energy stock has surged over the past year, yet the valuation checks currently lean expensive, so investors are weighing a strong share price run against signals that the stock is not priced like a clear bargain.

- FuelCell Energy has returned about 302.5% over the past year, which puts extra focus on whether the fundamentals justify that kind of move.

- Investor expectations are being shaped by large project wins in South Korea and potential AI data center power supply contracts, while recent share issuance to fund expansion highlights dilution risk and the need for the business to turn those projects into durable cash flows.

- The company scores 0 of 6 on Simply Wall St's broader valuation checks, which suggests the stock screens as expensive rather than cheap on most standard measures, as shown here.

For investors, the debate is whether FuelCell Energy's sharp re-rating leaves enough valuation support if growth and execution do not meet the market's expectations.

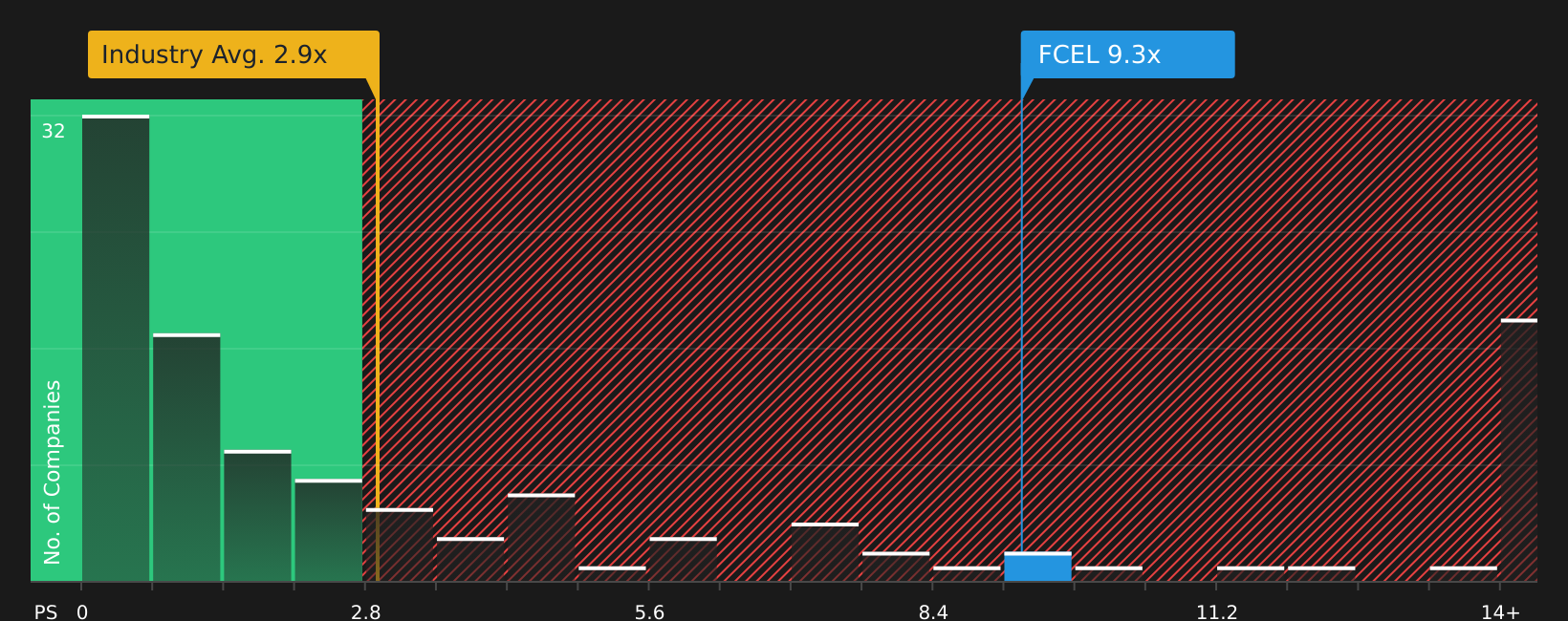

Has FuelCell Energy Run Too Far on Sales?

The P/S ratio is often a cleaner yardstick for a company like FuelCell Energy, where earnings and cash flows are still negative but revenue is visible.

FuelCell Energy trades on a P/S of about 9.1x, compared with an Electrical industry average of roughly 2.6x and a peer average around 2.2x. That puts the stock at a sizeable premium to both its sector and closer peers on a simple sales basis. The tailored fair P/S multiple, which reflects the company’s growth profile, margins, size and risk, is estimated at about 3.0x.

Because this fair multiple is far below the current P/S, the model is effectively flagging that FuelCell Energy screens very expensively on sales, rather than pointing to a precise target level. Despite the recent EXIM financing win and AI data center power agreements lifting enthusiasm, the valuation still implies investors are paying a high price for each dollar of current revenue.

On the P/S yardstick, FuelCell Energy stock appears richly valued relative to what its fundamentals currently support.

The FuelCell Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the FuelCell Energy valuation puzzle leaves off by spelling out which future paths for FuelCell Energy's growth, margins and earnings would need to hold for the stock to be worth materially more or less than today. Rather than relying on a single multiple or model, each Narrative lays out the assumptions that sit behind its view of fair value so you can compare them with the company’s actual results over time.

Community views on FuelCell Energy are sharply split, with some investors focused on data center growth potential and others fixated on execution and dilution risk.

Bull case: 25% undervalued

"By pivoting toward project structures with investment-grade counterparties and Energy-as-a-Service models, including long-term power purchase and service agreements, the company is set to build a high-visibility, recurring revenue stream that reduces risk, enhances predictability, and supports higher valuations on future cash flows…"

Bear case: 182% overvalued

"Although the Dedicated Power Partners (DPP) initiative and new long-term service agreements hint at increased bookings and backlog, actual progress toward ramping Torrington facility utilization from the current 31 megawatts to the target of 100 megawatts is entirely dependent on order flow, and long-standing execution issues raise doubts about whether the company can translate tailwinds into sustained recurring revenues or positive adjusted EBITDA in the forecasted timeframe…"

Do you think there's more to the story for FuelCell Energy? Head over to our Community to see what others are saying!

The Bottom Line

FuelCell Energy screens as overvalued on the current market multiple checks, with the tailored P/S ratio sitting well below where the stock trades today. That gap reflects how much optimism is already priced in around project wins and future cash generation, while the broader valuation score remains low. From here, the key question is whether FuelCell Energy can convert its backlog and new agreements into consistent, higher quality revenues that eventually justify paying such a premium multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.