GameStop Stock Faces A Harder Future As PlayStation Goes Fully Digital

GameStop Corp. Class A GME | 0.00 |

Sony’s move to end physical PlayStation game discs from 2028 puts a spotlight on companies still tied to boxes on shelves rather than downloads on consoles. With digital already accounting for over 80% of Sony’s game sales, the shift away from packaging, shipping, and retailer margins could reshape where money is made and where it dries up. This article breaks down 3 stocks that appear on the wrong side of that transition, each exposed to the same news in different ways, so you can decide which business models may face pressure as gaming goes fully digital.

Nintendo (TSE:7974)

Overview: Nintendo is a Kyoto based gaming company that creates and sells home consoles like the Switch, game software, accessories, and related online and mobile services built around its well known game franchises.

Operations: Nintendo generates about ¥2.3t in revenue from hardware and software for mobile and home console games.

Market Cap: ¥8,227.7b

Investors should care about Nintendo because it sits at the heart of the console market. Sony’s 2028 move away from discs raises hard questions about how much longer physical game sales can support its model. The stock trades below one estimate of fair value and carries a P/E of 19.4x against peers at 23.5x. However, revenue and earnings growth forecasts are modest, recent earnings strength follows a weak 5 year trend, and margins have already slipped from 23.9% to 18.3%. In addition, an unstable dividend record, heavy use of non cash earnings and reliance on external funding make the story look far less reassuring than headline brands and recent Switch 2 buzz might suggest.

Nintendo’s brand strength may be masking tougher questions around shrinking margins, modest forecasts and an unstable dividend record. Get the context behind that gap with the 3 key rewards and 2 important warning signs (1 is major!)

GameStop (GME)

Overview: GameStop is a Grapevine, Texas based specialty retailer that sells new and pre-owned gaming consoles, physical and digital games, in game currency, and a wide range of collectibles and pop culture merchandise through its GameStop, EB Games, Micromania, and Zing Pop Culture stores and e commerce sites across the United States, Europe, and Australia.

Operations: GameStop generates around US$2.8b of revenue from the United States, with a further US$512.4m from Australia and US$439.2m from Europe.

Market Cap: US$9.9b

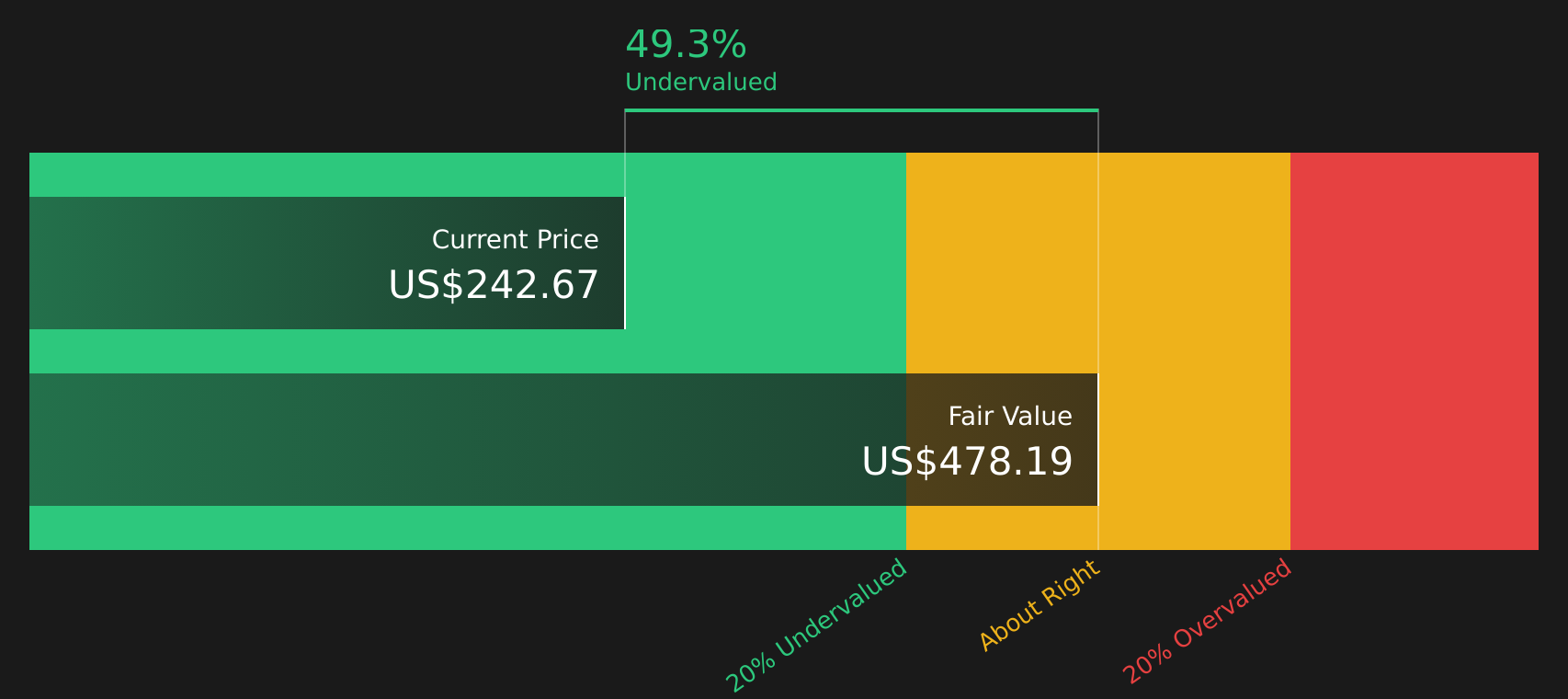

Investors looking at GameStop today are not just weighing a meme stock story; they are assessing a retailer whose core physical game business is under direct threat as Sony moves to end discs and push players fully online. GameStop has rebuilt profitability, holds a large cash reserve and Bitcoin stake, and is led by Ryan Cohen, who has waived major pay packages while pursuing an ambitious and uncertain eBay acquisition. At the same time, the company relies entirely on external borrowing, faces an all digital future that undercuts its historical model, and trades against a backdrop of high short interest and legal disputes over governance. The central question is whether recent earnings strength and a loyal shareholder base can offset the structural challenges in a world where consoles do not need stores like GameStop at all.

GameStop’s meme status and Bitcoin stash may be masking how exposed its core business is if consoles cut stores out entirely. For the fuller story, see the analysis report for GameStop

Amazon.com (AMZN)

Overview: Amazon.com is a Seattle based global retailer and technology company that sells a wide range of products and subscriptions through its online and physical stores, runs the Amazon Web Services cloud platform, offers advertising and digital content, and provides the Prime membership program to consumers and businesses worldwide.

Operations: Amazon.com generates about US$437.6b in revenue from North America, US$168.2b from its International segment, and US$137.0b from Amazon Web Services.

Market Cap: US$2.6t

Amazon.com looks interesting in this screener because it sits at the intersection of e commerce, cloud and advertising, yet still depends on selling boxed games and consoles that could shrink as Sony pushes players toward fully digital libraries. The stock is flagged as trading well below one estimate of fair value and carries strong profitability metrics, including a 20.5% return on equity and net margins of 12.2%. However, that strength comes with high non cash earnings, heavy reliance on external borrowing, and steady regulatory pressure on advertising and platform power. With AWS and AI infrastructure described as key bright spots, the real question is whether these engines can offset structural pressure on physical media sales and rising scrutiny of how Amazon runs its platform and uses customer data.

Amazon.com’s strong margins and fair value flags could be masking the significance of its physical media exposure and regulatory pressure for the story’s next chapter. Get the context in the analysis report for Amazon.com

Take Control of Your Investment Journey

If Nintendo or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Takes Off

Fresh ideas do not stay under the radar for long, and breakouts often fly once the crowd catches on, so review these curated stock lists while it matters and consider them promptly.

- Spot companies quietly building new trends before momentum headlines hit by scanning the 56 high quality undiscovered gems and see which stories still look early.

- Explore income ideas that aim to balance yield and resilience with a curated set of 55 dividend fortresses that could help steady a portfolio when growth stocks drop.

- Review 35 power grid technology and infrastructure stocks to assess which businesses might be positioned to participate if energy systems continue to modernize.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.