Gap (GAP) Is Down 9.6% After Cutting Sales Outlook but Raising Earnings Guidance – What's Changed

The Gap GAP | 0.00 |

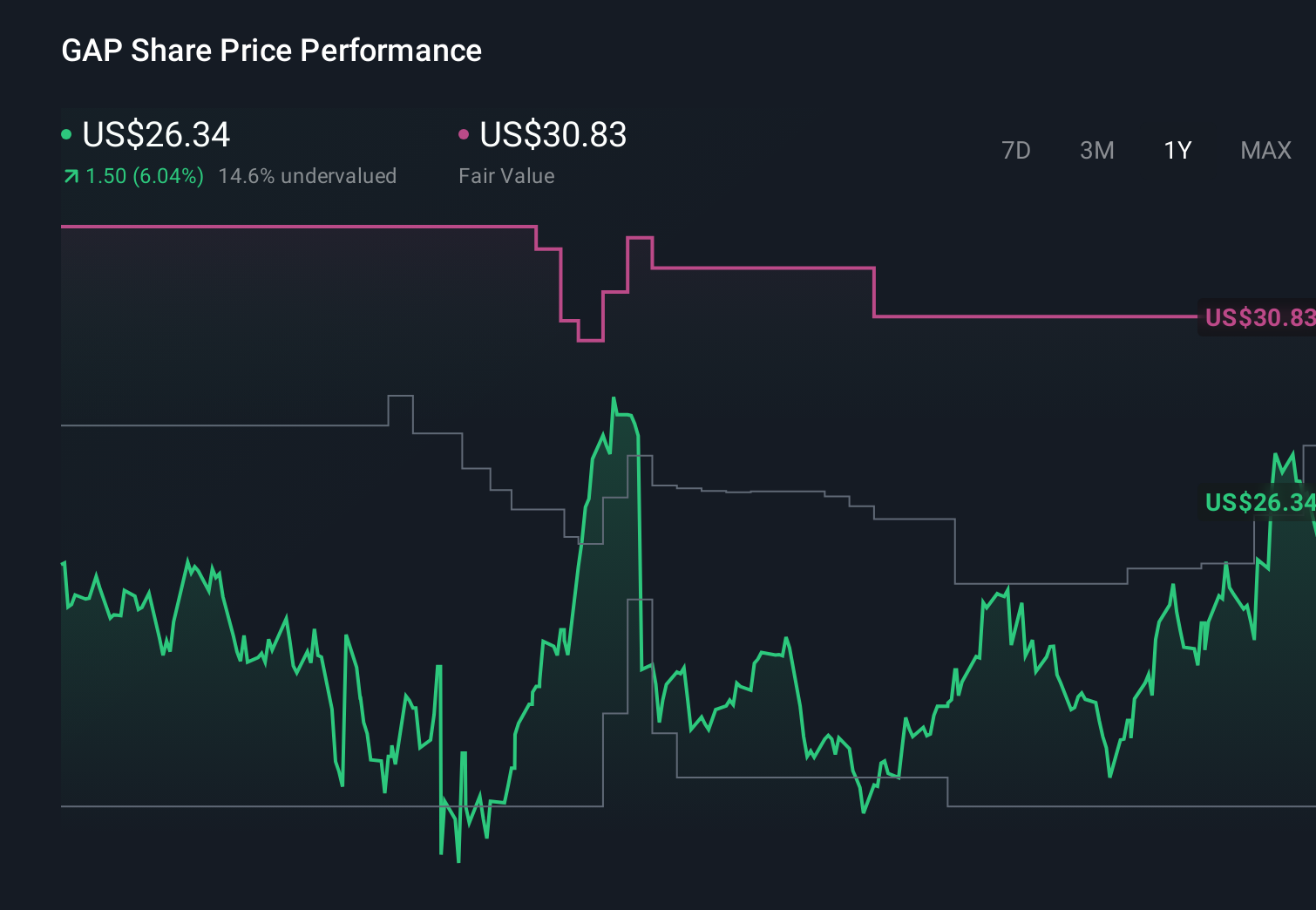

- In late May 2026, Gap Inc. reported first-quarter sales of US$3,497 million and net income of US$339 million, while trimming its full-year net sales growth outlook to 1%–2% and completing a US$401 million share buyback of 16,685,674 shares.

- The results highlighted a split within the portfolio, with the Gap brand delivering strong comparable sales growth but Old Navy’s fashion missteps in women’s apparel prompting corrective action and a reduced sales forecast even as full-year earnings guidance was raised.

- We’ll now examine how Gap’s lowered sales guidance, despite higher earnings expectations, reshapes the company’s investment narrative and risk-reward balance.

Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Gap Investment Narrative Recap

To own Gap today, you need to believe that disciplined execution can turn modest sales growth into healthier earnings, even with uneven brand performance. The latest quarter supports that idea on profitability, but the cut to full year net sales growth to 1%–2% underscores how dependent the story is on fixing Old Navy quickly, while Athleta remains a question mark. The biggest near term risk is that brand missteps at Old Navy persist longer than management expects.

The recent completion of a US$401 million buyback, retiring about 4.5% of shares, matters because it amplifies any earnings progress at a time when guidance calls for operating margin expansion and full year diluted EPS of US$2.83 to US$2.93. That capital return sits alongside raised earnings expectations but lower sales guidance, sharpening the focus on whether operational improvements, interest income and tax benefits can offset softer top line momentum.

Yet investors should also be aware that Old Navy’s fashion miss and slower comps leave Gap more exposed if...

Gap's narrative projects $16.6 billion revenue and $1.0 billion earnings by 2029.

Uncover how Gap's forecasts yield a $30.65 fair value, a 45% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were looking for revenue of about US$17.6 billion and earnings near US$1.2 billion by 2029, which assumes Athleta’s reset becomes a strong growth engine. Given Old Navy’s recent stumble, this more upbeat view sits in clear tension with the risk that persistent brand confusion and dilution could instead limit pricing power and pressure margins, reminding you that opinions can differ widely and may shift as the latest results are digested.

Explore 7 other fair value estimates on Gap - why the stock might be worth just $22.60!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Gap research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gap research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gap's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 12 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.