Gartner (IT) Margin Reset To 11.2% Challenges Bullish Earnings Narratives

Gartner, Inc. IT | 152.39 | +2.21% |

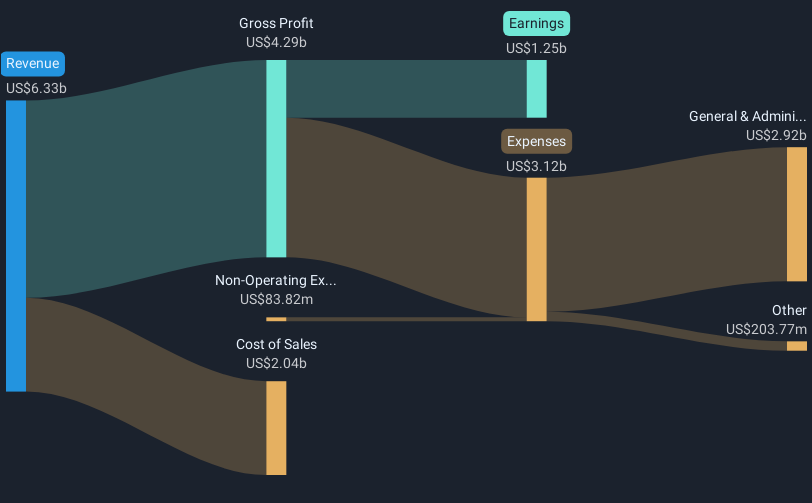

Gartner FY 2025 earnings snapshot

Gartner (IT) has wrapped up FY 2025 with Q4 revenue of US$1.8b and basic EPS of US$3.36, alongside net income of US$242.2m, setting the tone for how investors will read the year as a whole. Over recent quarters, the company has seen revenue move from US$1.5b in Q1 2025 to US$1.7b in Q2 and US$1.5b in Q3. Basic EPS has ranged from US$2.73 to US$3.36 across the year, giving you a clear view of how earnings are tracking through the cycle. With trailing net profit margins softer than the prior year, the key question now is how investors weigh that margin profile against the broader growth story and potential long term rewards.

See our full analysis for Gartner.With the headline numbers on the table, the next step is to line these results up against the most common narratives around Gartner to see which stories the data supports and which ones start to look less convincing.

Margins reset from 20% to 11.2%

- Over the last 12 months, Gartner’s net profit margin sat at 11.2%, compared with 20% in the prior year, while trailing twelve month net income was US$729.2m on US$6.5b of revenue.

- Bears point to this margin compression as a sign that high fixed costs and changing client behavior could weigh on profitability longer than expected.

- The bearish narrative highlights pressure on EBIT and net margins if large enterprise and government clients keep tightening external spend. This is consistent with margins moving from 20% to 11.2% on roughly US$6.5b of trailing revenue.

- At the same time, that US$729.2m of trailing net income still reflects what analysis data describes as high quality earnings, so the numbers do not yet match the more severe margin stress that some cautious investors worry about.

Steady revenue, softer earnings trend

- Across FY 2025, quarterly revenue ranged from US$1.5b to US$1.8b, while trailing twelve month revenue reached US$6.5b but trailing EPS moved from US$16.4 at the start of the year to US$9.7 by Q4.

- Consensus narrative suggests AI driven demand and secular themes like cybersecurity should support recurring revenue, yet the recent EPS pattern gives a more muted picture than the long term story implies.

- Analysts reference five year earnings growth of about 14.6% per year and forecast about 6.1% annual earnings growth ahead, but the drop in trailing EPS from over US$16 to US$9.7 shows that recent profit performance has not followed that longer term growth pace.

- The consensus view expects AI tools such as AskGartner to support margins over time, yet the latest year shows profit margins and EPS moving in the opposite direction. As a result, investors may wait for clearer evidence that these products are feeding through to stronger earnings.

Valuation gap versus slower growth

- At a current share price of US$158.58, Gartner trades at a trailing P/E of 15.3x, slightly below the 15.8x peer average and well below the 22.9x US IT industry level, while also sitting under a DCF fair value of about US$237.29.

- Bullish investors argue that this discount undervalues Gartner’s data assets and AI rollout, yet the growth inputs behind that view are more modest than you might expect for a stock trading against a US$237.29 DCF fair value and a consensus analyst target of US$193.83.

- Revenue is forecast to grow around 2.7% per year with earnings at roughly 6.1% per year, which is slower than the cited US market averages. The gap between the current price and both the DCF fair value and the US$193.83 target therefore assumes those forecasts still justify paying up versus a simple P/E comparison.

- Bulls point to high quality past earnings and multi year growth of about 14.6% per year, but the latest trailing net income of US$729.2m and 11.2% margin show a cooler phase than that history. The earnings trend will be key to whether the current discount closes.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Gartner on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If the story you are seeing does not quite match the consensus, shape your own view in a few minutes and Do it your way

A great starting point for your Gartner research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Gartner’s softer net margins and earnings, alongside only modest forecast growth, raise questions about how much compensation you are truly getting for the risk.

If that mix of cooler profitability and valuation questions is making you hesitate, compare it with companies our screener flags as 85 resilient stocks with low risk scores. This can help you quickly focus on potentially steadier options.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.