GE Aerospace’s Defense Backlog And Earnings Outlook Might Change The Case For Investing In General Electric (GE)

GE Aerospace GE | 0.00 |

- In recent days, GE Aerospace has drawn attention ahead of its April 21, 2026 earnings release, amid strong demand for aircraft engines, aftermarket services, and potential new defense-related production roles discussed with US officials.

- With a roughly US$190.00 billion backlog and increased global defense spending supporting its commercial and military programs, GE Aerospace’s existing order book and possible expansion into munitions and equipment production are becoming central to how investors view its future resilience.

- We’ll now examine how expectations for the upcoming earnings release and GE Aerospace’s large defense-linked backlog shape its current investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

General Electric Investment Narrative Recap

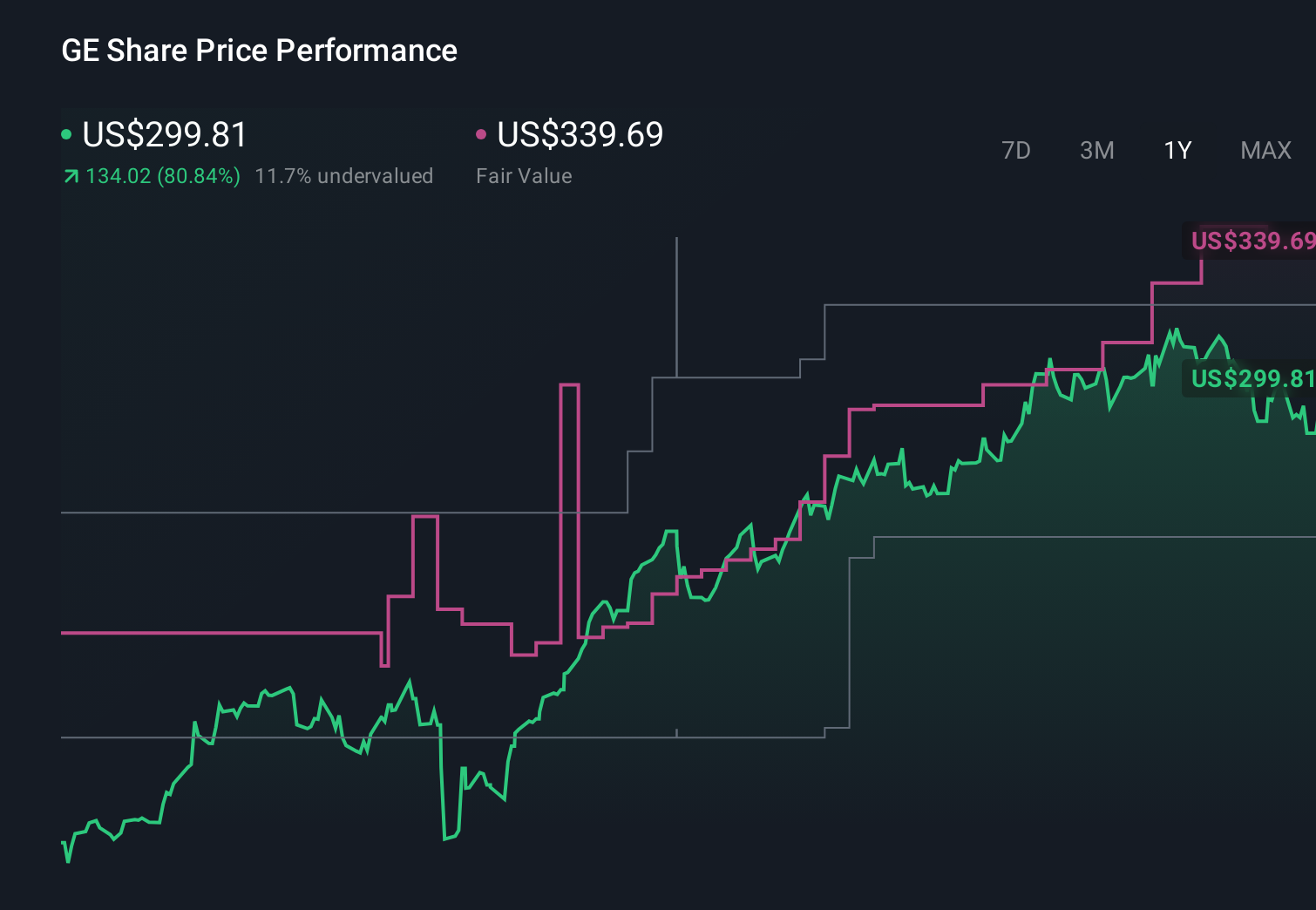

To own GE Aerospace today, you need to believe its large installed base, US$190.00 billion backlog, and mix of commercial and defense programs can support resilient earnings, even as the company is more exposed to aviation cycles as a pure-play aerospace name. The latest headlines around potential peace talks with Iran and a modest share price rebound do not materially change the near term earnings catalyst or the key risk of a downturn in global air travel and engine demand.

What does matter more right now is the upcoming April 21, 2026 earnings release, where analysts expect roughly 9.4% year over year earnings growth and 17.86% revenue growth. That report, set against GE Aerospace’s strong engine and aftermarket demand and the possibility of added defense manufacturing roles discussed with US officials, is likely to be the main reference point investors use to judge whether the backlog and defense exposure are being converted into profitable, sustainable growth.

Yet beneath the strong backlog headlines, investors should also be aware of how quickly a sustained air travel slowdown or faster climate policy shifts could...

General Electric's narrative projects $50.8 billion revenue and $9.5 billion earnings by 2028. This requires 6.9% yearly revenue growth and a $1.9 billion earnings increase from $7.6 billion.

Uncover how General Electric's forecasts yield a $357.24 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most bearish analysts, who were assuming revenue of about US$56.2 billion and earnings near US$10.4 billion by 2029, paint a much more cautious picture than the base case, particularly around climate and technology risks, so it is worth weighing those assumptions against how this week’s defense and earnings related news could reshape expectations.

Explore 8 other fair value estimates on General Electric - why the stock might be worth 9% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Electric research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

No Opportunity In General Electric?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.