GE Vernova Stock And 2 Nuclear Power Picks For AI Infrastructure

GE Vernova Inc. GEV | 0.00 |

AI infrastructure, inflation concerns and the push for carbon-free power are all converging to put reliable 24/7 electricity at the center of the investment conversation. While rate moves, inflation signals and uneven global growth keep headlines busy, the Nuclear Renaissance screener focuses on companies tied to nuclear power that aim to support long term energy demand for data centers and climate goals. This article highlights 3 stocks from that screener that stand out on quality and exposure to this theme, providing a focused starting list for deeper research into the nuclear backbone of the intelligence era.

AtkinsRéalis Group (TSX:ATRL)

Overview: AtkinsRéalis Group is a Montreal based engineering and project management company that works across the full infrastructure spectrum, from designing and running major transport, water, power and defence projects to managing assets and capital investments. It also has deep expertise across the nuclear life cycle, including new reactor builds, life extensions, decommissioning and waste management, making it closely tied to long term decarbonization and energy security trends.

Operations: AtkinsRéalis generates most of its CA$11.5b business revenue from Engineering Services in the UKI (CA$2.8b), USLA (CA$2.1b), Canada (CA$1.5b) and AMEA (CA$1.3b) regions, with a sizeable Nuclear segment at about CA$2.5b and additional segment adjustments of CA$1.2b.

Market Cap: CA$14.5b

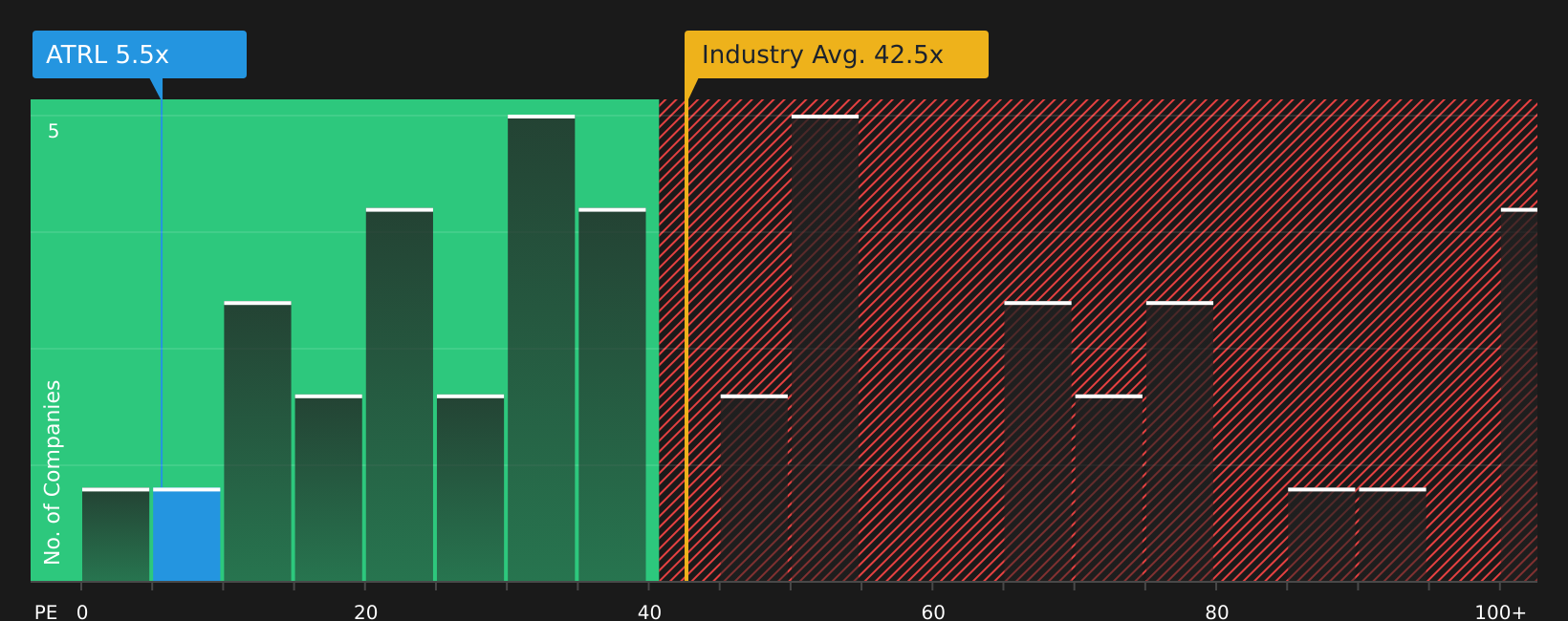

Investors looking at the Nuclear Renaissance theme may find AtkinsRéalis Group interesting because it combines a large contracted nuclear and infrastructure backlog with high margin engineering and advisory work, while still trading on what looks like a low P/E next to both its industry and analyst expectations. The company is deeply involved in UK and Canadian nuclear programs, U.S. CANDU licensing and emerging SMR partnerships, which tie it directly to long dated power needs for data centers and decarbonization. At the same time, reliance on big nuclear contracts, past lump sum project issues, heavy use of external borrowing and a sharp forecast pullback in earnings mean that execution and capital discipline really matter. Understanding how those trade offs stack up is where the real opportunity may lie for AtkinsRéalis Group.

AtkinsRéalis Group’s mix of nuclear backlog, high margin engineering work and what looks like a low P/E raises a clear question: is the market missing something in the 5 key rewards and 3 important warning signs around this story in the 5 key rewards and 3 important warning signs (2 are major!)

Worley (ASX:WOR)

Overview: Worley is a Sydney based professional services company that plans, designs and manages complex projects for the energy, chemicals and resources sectors worldwide, ranging from oil and gas and petrochemicals to nuclear power, hydrogen, battery materials and mine development, as well as decommissioning and sustainability consulting.

Operations: Worley reports A$12.4b in segment adjustments at the business level, alongside A$0.4b of unallocated procurement revenue at nil margin and a A$1.7b reduction from its unallocated share of revenue from associates, while regionally its largest markets are the Americas at A$6.2b and Europe, Middle East and Africa at A$4.0b.

Market Cap: A$5.3b

Worley sits at the center of the energy transition theme, with management indicating that a growing majority of revenue is tied to sustainability work such as renewables, hydrogen, carbon capture and low carbon fuels, alongside more traditional oil, gas and LNG projects. The company has experienced recent pressure on professional services revenue, modest net margins around 3.1% and relies on external borrowing, which keeps risk firmly on the table. For investors, the combination of an A$13.9b revenue target case, analyst price targets above the current share price and active contract wins in areas like copper and energy transition materials makes Worley a company worth a closer look in the Nuclear Renaissance context.

Worley’s push into energy transition work, combined with modest 3.1% net margins and external borrowing, raises a bigger question about how the risk and reward really stack up in the 2 key rewards and 1 important warning sign

GE Vernova (GEV)

Overview: GE Vernova is an energy infrastructure company that supplies equipment and services to generate, move, convert and store electricity worldwide, spanning gas, nuclear, hydro and steam power, wind turbines and grid hardware and software that connect power plants to data centers, factories and homes.

Operations: GE Vernova generates most of its revenue from Power at US$20.3b, alongside US$10.8b from Electrification and US$8.7b from Wind, with smaller eliminations and other items of US$0.4b.

Market Cap: US$291.7b

GE Vernova is attracting attention because it sits at the heart of the AI and electrification buildout, supplying gas turbines, nuclear and grid technology that underpin power hungry data centers, with an installed base of roughly 7,000 gas turbines and over US$31b in unearned service revenue creating long dated, service driven cash flows. Earnings growth has been very strong recently, net margins sit at 23.8% and ROE is an exceptional 62.2%. Yet the stock trades on a P/E below many Electrical peers, which raises questions about how much of the AI and grid upgrade opportunity is already reflected in the price. At the same time, a troubled Wind segment, reliance on external borrowing, insider selling and governance growing pains mean this is far from a risk free story and worth a deeper look for investors focused on the Nuclear Renaissance theme.

GE Vernova’s powerful mix of 23.8% net margins and 62.2% ROE suggests a story the market may not fully be pricing, but the real twist sits inside the 4 key rewards and 2 important warning signs (1 is major!)

The three Nuclear Renaissance stocks in this article are only a small sample of the opportunity, with the full screener surfacing 86 more companies whose stories around baseload power, grid upgrades and long dated data center contracts may be just as compelling. Unlock the full picture by using the Nuclear Renaissance screener to identify and analyze the specific catalysts and narratives that matter most to you, so you can focus on the highest conviction ideas for this theme.

Take Control of Your Investment Journey

If Worley or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh stock ideas do not stay under the radar for long. As momentum builds and prices start flying, the cleanest entry points can become harder to find, so consider researching potential opportunities early.

- Spot potential breakout growth stories early by scanning 8 high quality undiscovered gems curated for stronger balance sheets and quality fundamentals before they get fully caught in the spotlight.

- Target steadier income opportunities by reviewing the curated 6 dividend fortresses focused on companies with higher yields that some investors overlook while prices still look reasonable.

- Ride powerful automation momentum by checking the hand picked 29 robotics and automation stocks that zeroes in on companies tied to industrial efficiency and long term productivity themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.