General Motors (GM) Valuation Check As Data And AI Vendor Approval Targets Dealership Performance

general motors GM | 0.00 |

General Motors (GM) has approved Pinnacle Intelligence as an authorized vendor for Business Development Center services, putting data and AI at the center of efforts to improve dealership operations and customer experience.

Despite the latest move to bring more data and AI into its dealer network, GM's share price sits at US$83.24 after easing 1.32% over the last day. A 9.86% 1 month share price return and 69.50% 1 year total shareholder return point to strong recent momentum.

If you are tracking how technology and automation are reshaping companies like GM, it can be useful to broaden your watchlist with 33 robotics and automation stocks

With GM delivering a 69.50% 1 year total shareholder return and trading at US$83.24 alongside an indicated intrinsic discount of 32.11%, the key question is whether this momentum still leaves upside or if the market is already pricing in future growth.

Most Popular Narrative: 99.2% Overvaluled

According to the most followed narrative, GM's fair value of $41.79 sits well below the last close at $83.24, putting a spotlight on how expectations stack up against the current price.

General Motors faces uncertain market conditions in manufacturing, operations, and ultimately product line decisions. EV development is hugely important in the industry and GM has invested towards this, but under the current administration, along with other impactful costs, GMs EV investments will take years to materialize in significant returns. Eventually these returns will come, but GM will lag much of the industry in this as their focus now has to turn to manufacturing and organizational stability. P/E will eventually increase as the industry flourishes under the eventual excitement of EV development, but GM will lag the industry in this. Overall revenue won't take much of a hit, and could even increase, but profit margins will fall in the near term.

Want to see how this view arrives at a fair value around half the current price? The narrative leans on moderate revenue growth, slimmer margins, and a future earnings multiple that sits below faster growing peers.

Result: Fair Value of $41.79 (OVERVALUED)

However, if GM converts its US$184,623.0m in revenue and US$2,433.0m in net income into steadier profitability or outperforms the assumed 3.4% margin, this overvalued case weakens.

Another View: Cash Flows Point the Other Way

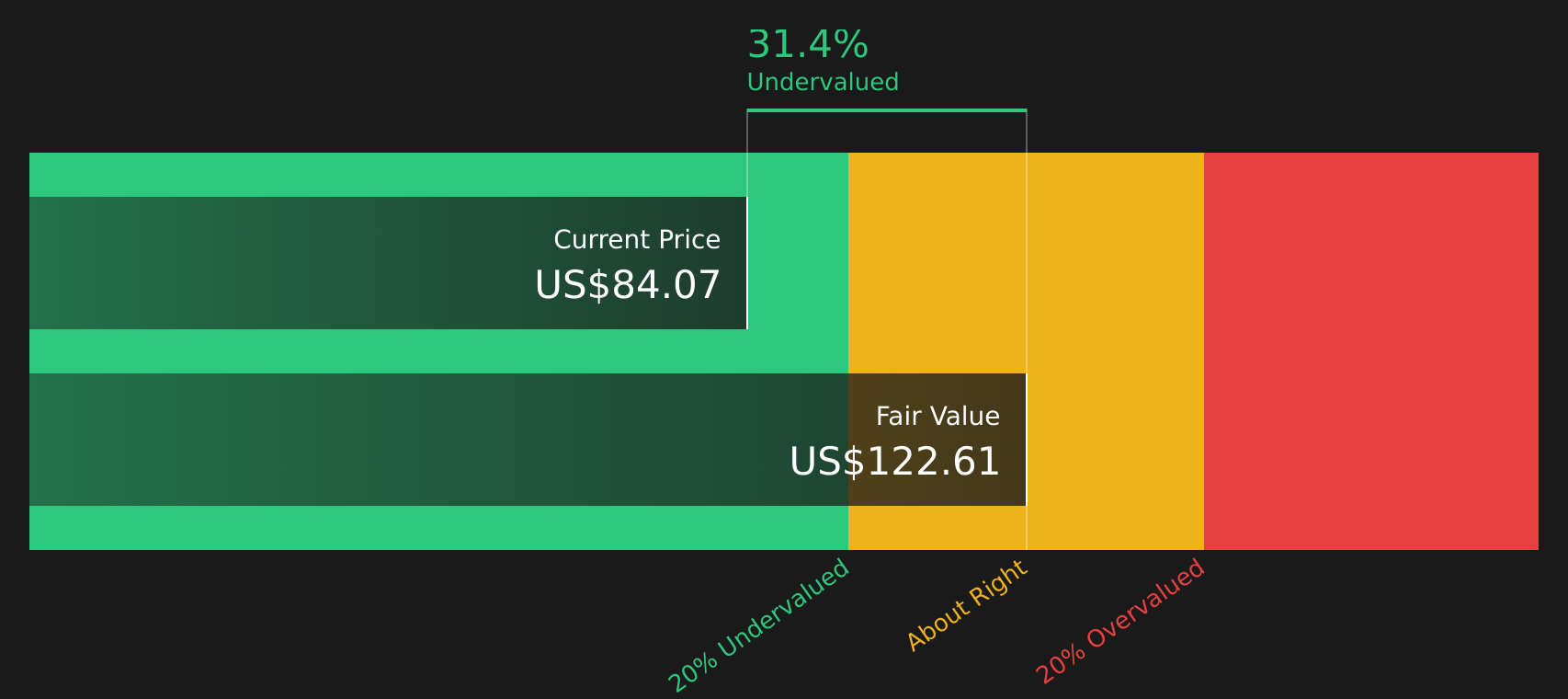

While the popular narrative views GM as overvalued at a fair value estimate of $41.79, our DCF model estimates a value of future cash flows of $122.61 per share. This is above the current $83.24 price and implies the stock is undervalued using this method. Which interpretation do you think better fits the risk profile you are seeking?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out General Motors for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Conflicted by the mixed signals in this article? Act while the data is fresh in your mind and weigh both sides using the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

Do not stop with just one stock. Broaden your opportunity set now so you are not looking back later wishing you had checked a few more options.

- Target dependable income streams by scanning companies labeled as 10 dividend fortresses that may fit a portfolio focused on cash returns.

- Hunt for potential bargains by reviewing 46 high quality undervalued stocks that combine quality fundamentals with prices that differ from intrinsic estimates.

- Prioritize capital protection first by focusing on 63 resilient stocks with low risk scores that may align with a more cautious approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.