Genesis Energy (GEL) Stock Valuation After Balance Sheet Repair And Offshore Project Ramp Up

Genesis Energy, L.P. GEL | 0.00 |

Conference spotlight: why Genesis Energy is on investors’ radar

Genesis Energy (GEL) is stepping in front of credit and energy investors this week, presenting at Bank of America and RBC conferences as its balance sheet work and offshore growth projects attract fresh attention.

Despite balance sheet progress and the ramp up of the Shenandoah and Salamanca offshore projects, Genesis Energy’s 90 day share price return is down 14.76%, while its 5 year total shareholder return is up 81.64%.

If you are looking beyond midstream and want other ideas tied to energy infrastructure demand, it could be worth scanning 34 power grid technology and infrastructure stocks

With the units down over the past 90 days despite balance sheet repair and large offshore projects ramping up, the key question is whether Genesis Energy is still trading below its fundamentals, or if the market is already pricing in that future growth.

Preferred Price-to-Sales of 1.1x: Is it justified?

Genesis Energy units last closed at $15.13, and on a P/S of 1.1x the stock screens cheaper than many US oil and gas peers, yet still a touch above its own fair P/S estimate.

The P/S multiple compares the total value investors are placing on the equity with the revenue the company generates, which can be particularly useful for businesses that are currently loss making. For Genesis Energy, this lens matters because the company is still unprofitable, so earnings based ratios do not yet tell a clean story.

On one side, Genesis Energy is flagged as good value on a P/S of 1.1x versus both the US oil and gas industry average of 2x and a closer peer set at 2.7x. This suggests the market is assigning a lower revenue multiple than many comparables. On the other side, that same 1.1x P/S sits slightly above an estimated fair P/S ratio of 1x. This is a level the market could move towards if sentiment or growth expectations cool from here.

Result: Price-to-sales ratio of 1.1x (UNDERVALUED).

However, unit price weakness, despite a 3 year total return above 75% and ongoing net losses, could signal that some investors remain cautious on execution and capital discipline.

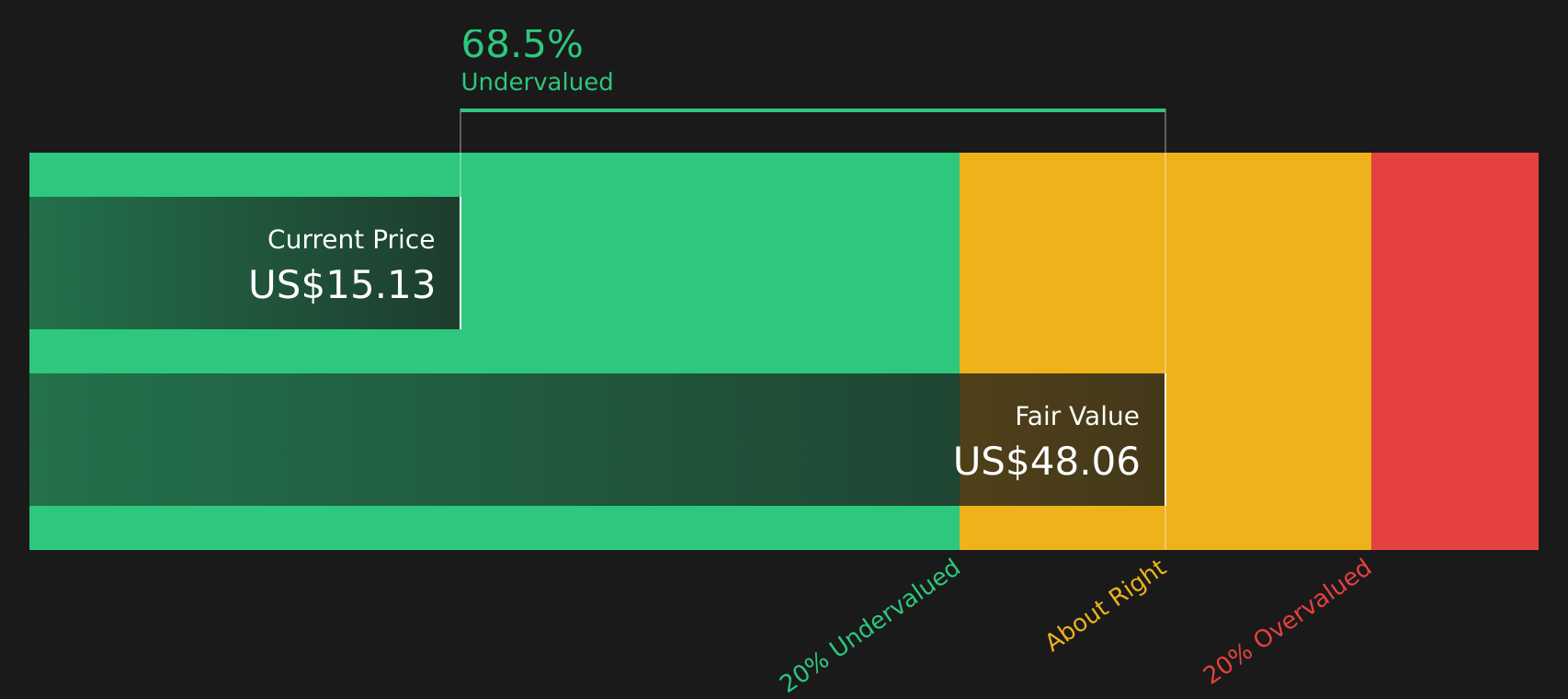

Another view: DCF points to a very different price

While the P/S of 1.1x makes Genesis Energy look inexpensive against peers, the SWS DCF model presents a far more aggressive view, with an estimated future cash flow value of $48.78 per unit compared with the current $15.13. That gap suggests either a large potential valuation difference or very cautious market expectations.

Before relying on the SWS DCF model too heavily, it is worth understanding how it treats long dated offshore cash flows, discount rates, and terminal assumptions, particularly for a company that is still loss making and uses higher risk funding sources. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Conflicted by the mix of risks and rewards in this story? Take a closer look now, weigh the trade offs, and review the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Genesis Energy is on your radar, do not stop there. Casting a wider net across high quality stock ideas could help you build a stronger portfolio.

- Target potential upside in overlooked companies by reviewing the screener containing 20 high quality undiscovered gems that meet strict fundamental checks and might not yet be crowded trades.

- Strengthen your defense by scanning the 70 resilient stocks with low risk scores so you are not caught out when conditions turn and weaker stocks struggle to keep up.

- Focus on quality at a reasonable price by using the 44 high quality undervalued stocks to spot stocks where fundamentals and valuation still look aligned in your favor.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.