Genesis Energy (GEL) Valuation After Q1 Miss, Shenandoah Guidance Cut And Lower Financing Costs

Genesis Energy, L.P. GEL | 0.00 |

Genesis Energy (GEL) is back in focus after first quarter results came in slightly below expectations, with management trimming 2026 Shenandoah field volume assumptions while also outlining lower annual financing costs and greater capital structure flexibility.

Despite the recent conference appearance and insider equity grants, the share price has been under pressure, with a 30 day share price return of down 11.13% and a 90 day share price return of down 16.65%. The 3 year total shareholder return of 77.61% points to a much stronger past run, suggesting momentum has cooled in the short term.

If recent volatility in midstream infrastructure has your attention, it could be a good moment to scan beyond Genesis Energy and check out 33 power grid technology and infrastructure stocks

With units recently under pressure, a value score of 5, an intrinsic value gap indicator, and a discount to the average analyst price target, investors now face a key question: Is Genesis Energy undervalued or already pricing in future growth?

Price to Sales of 1.1x: Is it justified?

On a P/S basis, Genesis Energy trades at 1.1x revenue, which screens as slightly expensive relative to its own fair P/S estimate but cheaper than many peers.

The P/S multiple compares the company’s market value with its revenue, which can be useful when earnings are pressured or loss making, as is the case here. At a market capitalization of about $1.84b against revenue of $1.68b, investors are currently paying a little more than $1 in equity value for every $1 of annual sales.

According to the SWS fair ratio work, Genesis Energy sits above an estimated fair P/S of 1x. This suggests the market is assigning a modest premium to its current revenue base that could compress if sentiment cools, or widen if investors gain confidence in its earnings trajectory. At the same time, the stock trades at a 1.1x P/S compared with around 2x for the broader US Oil and Gas industry and 2.9x for its peer group. This places Genesis Energy at a clear discount to sector and peer averages that could narrow if perceptions shift closer to the fair ratio level.

Result: Price-to-Sales of 1.1x (UNDERVALUED)

However, the recent unit price pressure alongside ongoing net income losses could keep sentiment fragile if investors reassess balance sheet and cash flow resilience.

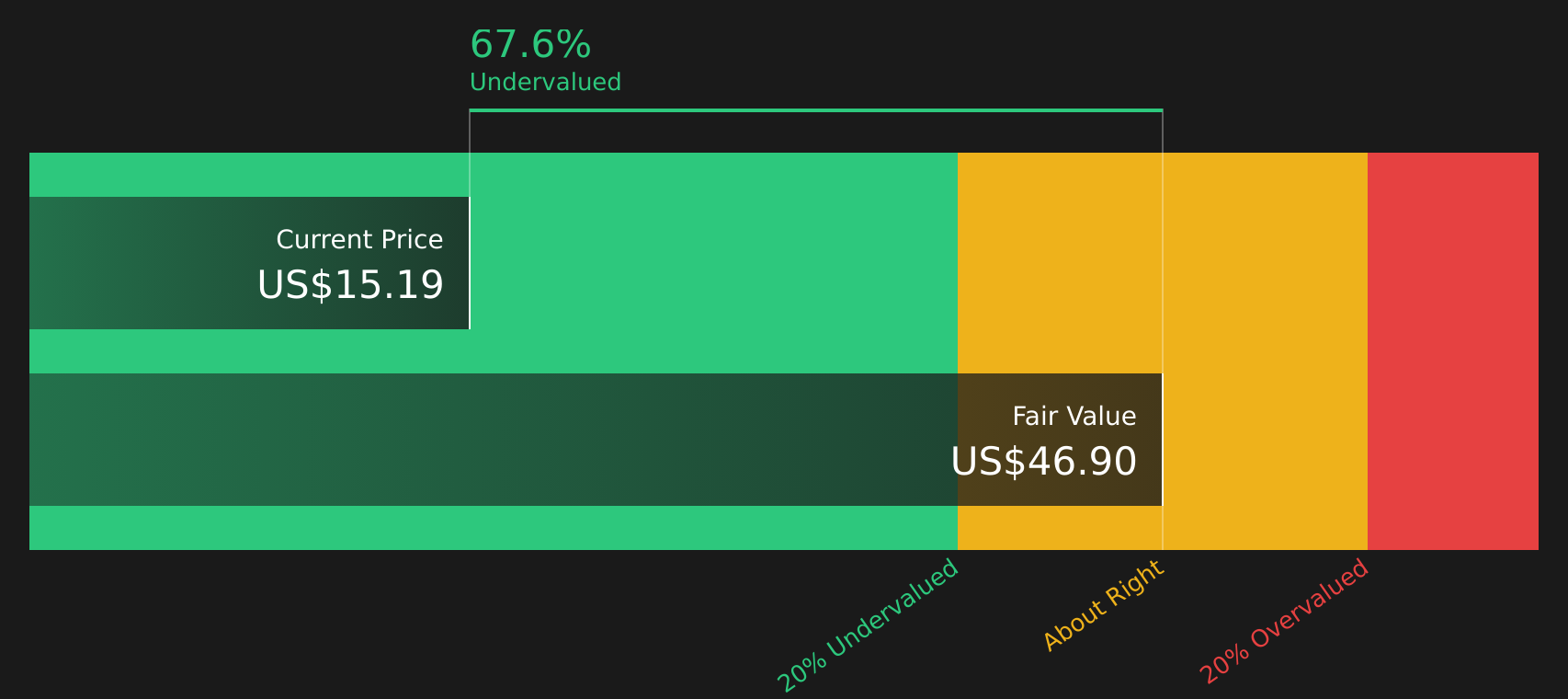

Another View: DCF Signals Much Deeper Value Gap

While the 1.1x P/S ratio hints at only a mild premium to the 1x fair ratio, the SWS DCF model presents a much starker picture, with Genesis Energy units at $15.17 compared with an estimated future cash flow value of $46.39, implying a very wide valuation gap. Which signal appears more informative: a simple sales multiple or a full cash flow model?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed, with both risks and rewards in play, this is the moment to look through the data yourself and decide how the story stacks up. To weigh both sides in one place, start with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you risk missing opportunities that better match your goals, so widen the field and let the numbers work for you.

- Target companies with solid income potential and stress test your yield expectations using the 10 dividend fortresses.

- Hunt for quality at a discount by scanning the 47 high quality undervalued stocks before prices move away from you.

- Prioritize financial strength and reduce surprise risks by focusing on the solid balance sheet and fundamentals stocks screener (45 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.