Gilead Sciences (GILD) Valuation Check After Oncology And HIV Therapy Momentum

Gilead Sciences, Inc. GILD | 137.64 | -0.66% |

Gilead Sciences (GILD) has returned to focus after a series of company-specific catalysts, including its oncology expansion through Repare Therapeutics, FDA approval of HIV prevention drug Yeztugo, and encouraging updates for Trodelvy and Yescarta.

These company specific catalysts have coincided with a sharp shift in market sentiment, with a 30 day share price return of 23.1% and a 1 year total shareholder return of 56.6% suggesting momentum has been building.

If Gilead’s recent oncology and HIV news has caught your attention, it could be a good moment to scan other healthcare names through our focused list of 25 healthcare AI stocks.

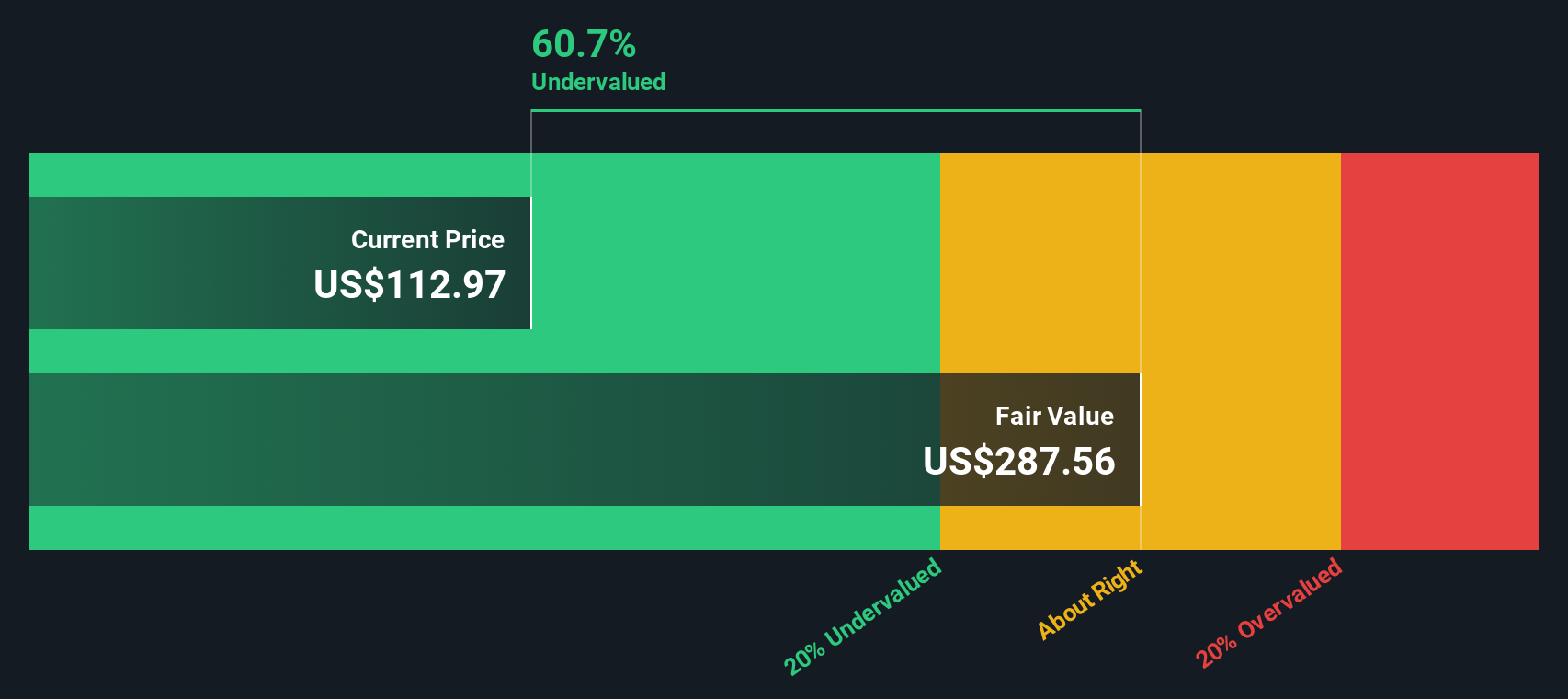

With Gilead shares up 56.6% over the past year and trading above the average analyst price target, yet still flagged by some models as at a 47.7% intrinsic discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 12.7% Overvalued

Gilead Sciences last closed at $149.37, compared with a widely followed fair value estimate of $132.57 that applies a 7.34% discount rate to future cash flows.

The launch and scaling of new products position Gilead to deliver a more favorable product mix and premium pricing, driving higher gross margins and improving long term earnings trajectory as portfolio diversification reduces overexposure to legacy products. Disciplined operating expense management and expanded share buybacks backed by strong free cash flow are increasing efficiency, supporting progressively higher operating margins and earnings, with updated guidance reflecting confidence in operating leverage and capital returns.

Curious what earnings path, margin profile and future P/E multiple need to line up for that fair value? The most followed narrative spells out a detailed glide path for revenue, profitability and capital returns, and shows how those moving parts connect to a higher long run earnings base and a richer valuation multiple than the broader biotech space.

Result: Fair Value of $132.57 (OVERVALUED)

However, this depends on HIV remaining a reliable earnings engine, and on oncology and cell therapy programs avoiding regulatory or uptake setbacks that could challenge those projections.

Another Take: DCF Points the Other Way

Analysts looking at near term earnings and multiples see Gilead as about 12.7% overvalued versus a $132.57 fair value. Our DCF model lands in a very different place, with a future cash flow value of $285.84 per share. This frames today’s $149.37 price as a large discount instead. Which story do you think fits the business better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Gilead Sciences for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Gilead Sciences Narrative

If you look at this and think the assumptions do not quite fit your view, or you prefer testing your own inputs against the data, you can spin up a custom narrative in just a few minutes and Do it your way.

A great starting point for your Gilead Sciences research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Gilead has sharpened your thinking, do not stop here. Use the screener to spot fresh opportunities that match the kind of portfolio you want to build.

- Target potential value opportunities by reviewing companies our models flag as 55 high quality undervalued stocks based on earnings, cash flows and balance sheet support.

- Focus on income potential and cash payouts by scanning 15 dividend fortresses that may appeal if you are building a yield focused portfolio.

- Prioritise resilience and capital preservation by checking 81 resilient stocks with low risk scores that score well on our risk factors and financial strength checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.