Globus Medical (GMED) Stock Looks Like A Bargain At This Price

Globus Medical Inc Class A GMED | 0.00 |

Globus Medical stock has delivered a 39.0% return over the past year, and the current valuation checks lean toward the shares looking inexpensive rather than stretched, which creates a clear question about how much of that strength is supported by fundamentals.

- Over the past 12 months, Globus Medical is up 39.0%, a move that puts recent share price momentum firmly on investors' radar.

- BMO Capital's recent Outperform rating with a US$94 price target highlights confidence that earnings can be supported by NuVasive acquisition synergies and demand for its robotic supported implant portfolio. Any disappointment on integration or margin trends may weigh on how much investors are willing to pay for that growth.

- On Simply Wall St's broader valuation checks, Globus Medical screens as undervalued in 6 of 6 areas, suggesting the current share price may not fully reflect the fundamentals that model is capturing.

The stock's next move may depend on whether that strong one year return has already absorbed most of the upside implied by these valuation checks, or if there is still a margin between price and what investors are paying for similar businesses.

Is Globus Medical a Bargain on Earnings?

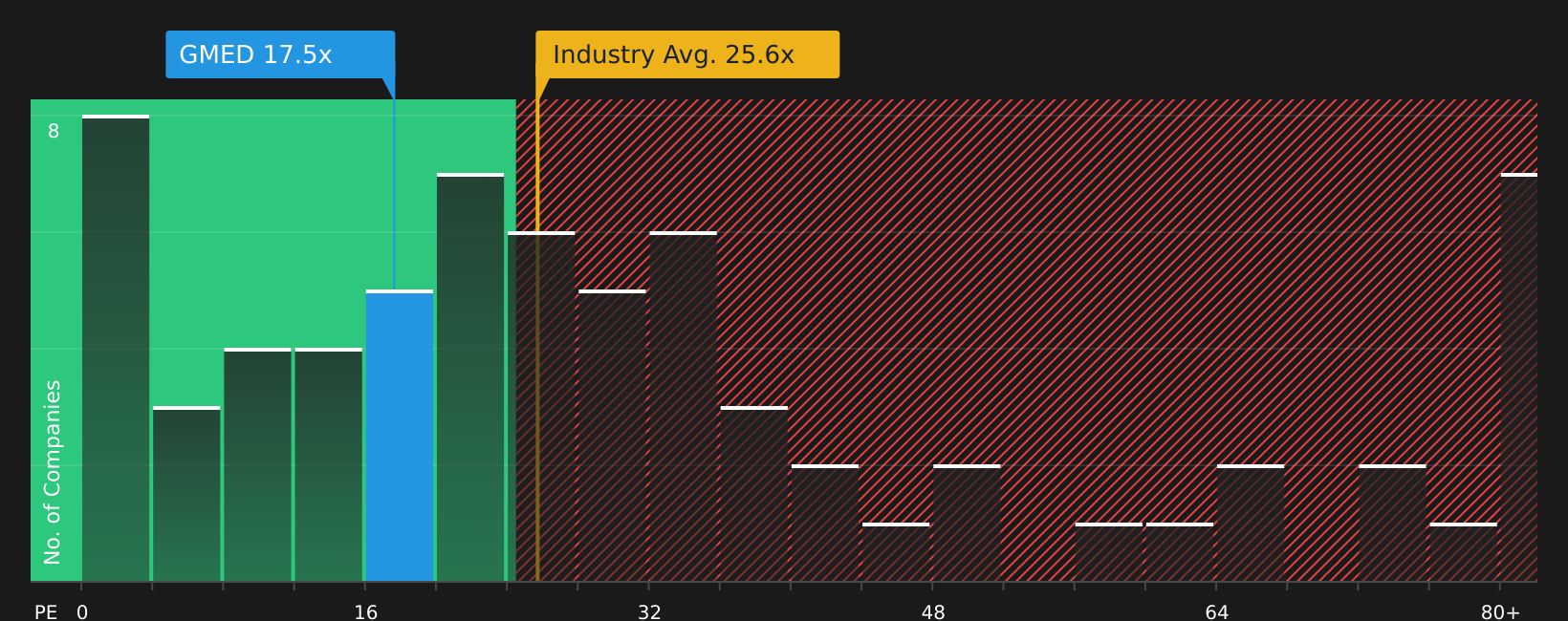

The P/E ratio is a useful way to think about what you are paying today for each dollar of Globus Medical's earnings. On this measure, Globus Medical trades at about 18.5x earnings, which sits well below the Medical Equipment industry average of roughly 26.2x and also under the peer group average of about 40.3x.

A tailored fair P/E multiple for Globus Medical, which accounts for its industry, margins, size and risk profile, sits near 26.4x. The current 18.5x level therefore implies a sizeable discount to what that framework suggests investors might typically pay. Despite BMO Capital's recent Outperform rating and a US$94 price target bringing more attention to the stock, the P/E still prices Globus Medical below both the industry benchmark and this fair ratio estimate.

On the P/E multiple alone, Globus Medical stock appears undervalued relative to both its industry and a more tailored fair-value benchmark.

The Globus Medical Narrative: What Would Justify Today's Price?

Simply Wall St's Narratives for Globus Medical pick up where the valuation puzzle leaves off. They spell out which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price on the Community page. Each narrative ties a fair value estimate to a specific story about Globus Medical's potential catalysts and risks, so you can track over time which version of events seems to be taking shape.

One of the top community narratives on Globus Medical: 26% undervalued

"A robotic ecosystem is viewed as increasingly driving durable implant pull through, which, alongside mid 30s EBITDA margins, supports the case for resilient profitability in valuation work…"

Do you think there's more to the story for Globus Medical? Head over to our Community to see what others are saying!

The Bottom Line

Globus Medical screens as undervalued on its current P/E and broader valuation checks, so the market is still pricing the stock below what comparable businesses command. That gap will likely only close if investors stay confident that synergies from NuVasive and demand for its robotic supported implant portfolio can be translated into resilient margins. For now, the key question is whether the discount reflects an opportunity or lingering concern that integration or profitability could fall short of expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.