Gold Stocks With Strong Balance Sheets As Investors Look For Safety

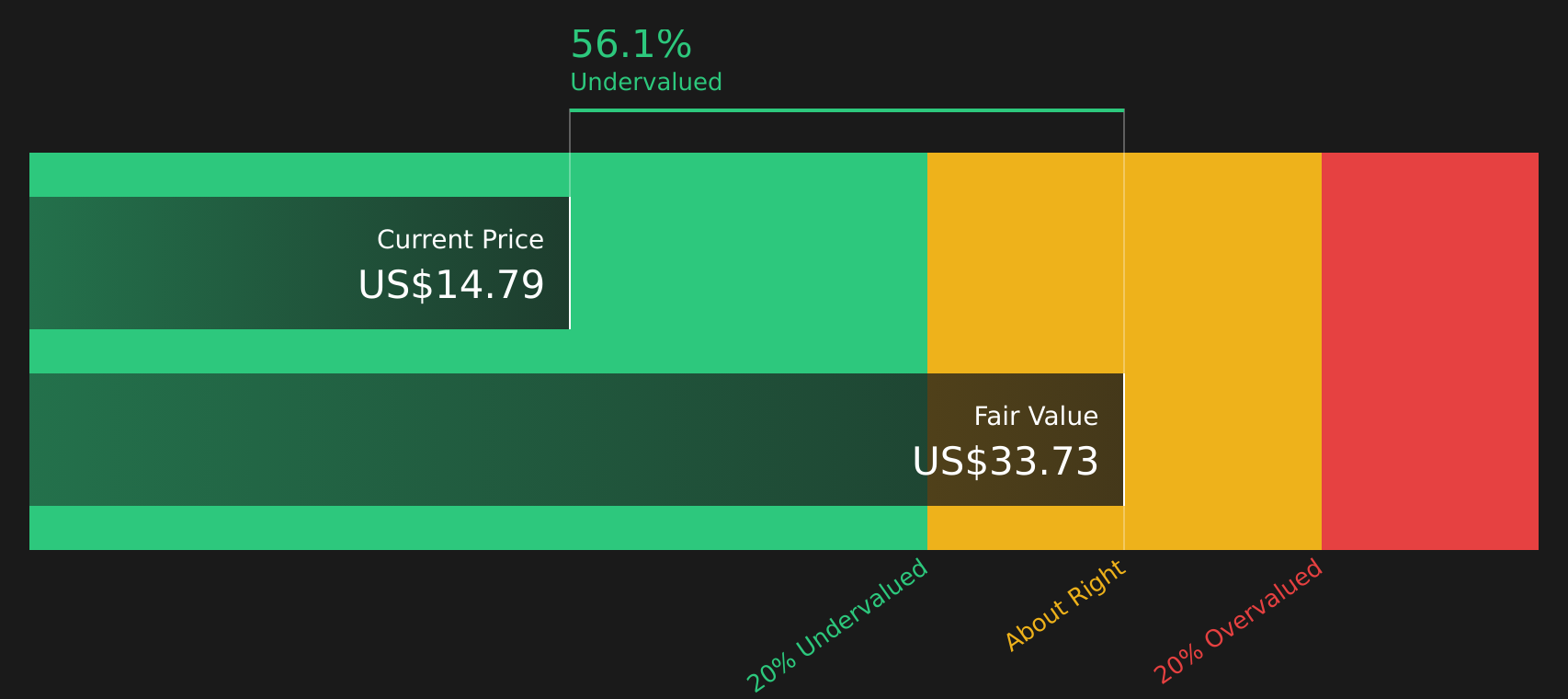

Coeur Mining, Inc. CDE | 0.00 |

With inflation readings shifting across regions, central banks weighing their next moves and oil and geopolitical tensions keeping investors on edge, attention is turning to assets that some see as potential stores of value. Gold sits at the heart of that discussion, and the Elite Gold Stocks screener focuses on miners with stronger balance sheets and relatively lower production costs. These companies can be better placed to handle swings in the gold price and operational pressures. This article highlights 3 stocks from the Elite Gold Stocks screener that stand out on those quality filters.

Orla Mining (TSX:OLA)

Overview: Orla Mining is a Vancouver based gold producer and developer with a portfolio of open pit and underground projects across Mexico, Panama, Nevada and Ontario, focused on gold and silver with additional exposure to zinc, lead and copper. Its core assets include the producing Camino Rojo project in Mexico, the Cerro Quema and South Railroad development projects, and an interest in the Musselwhite Gold Mine in Canada.

Operations: Orla Mining generates most of its revenue from the Mussel-White Mine at about $817.2m and Camino Rojo at about $348.3m, with around $130.6m reported under Corporate activities.

Market Cap: CA$5.0b

Orla Mining stands out in the Elite Gold Stocks screener because it combines producing assets like Camino Rojo and Musselwhite with a pipeline of projects that could reshape its scale. It is also part of a proposed at market merger with Equinox Gold that would create a larger North American producer. Analysts highlight expectations for very strong earnings growth and high future returns on equity, supported by improving margins and a dividend that introduces income alongside growth potential. At the same time, investors need to weigh meaningful risks, including permitting in Mexico and Nevada, labor disputes at Camino Rojo and higher all in sustaining cost guidance, which could pressure cash flow if gold prices soften.

Orla Mining’s mix of producing mines and growth projects is getting attention, but the real question is how that earnings story balances with its risks, which is exactly what the 3 key rewards and 1 important warning sign examines.

Coeur Mining (CDE)

Overview: Coeur Mining is a Chicago based precious metals producer that operates gold and silver mines across the United States, Mexico and Canada, selling concentrates and refined metal to smelters and refiners. Its portfolio includes operations such as Palmarejo, Rochester, Kensington, Wharf and Las Chispas, along with exploration for zinc, lead and related metals.

Operations: Coeur Mining generates most of its revenue from Palmarejo at about US$566.2m, Las Chispas at about US$557.0m, Rochester at about US$556.8m, Kensington at about US$421.3m and Wharf at about US$330.7m, with total revenue primarily split between Mexico at about US$1.1b and the United States at about US$1.3b.

Market Cap: US$16.6b

Coeur Mining is attracting fresh interest because it combines a large producing base, including the Rochester expansion and Las Chispas acquisition, with strong recent profitability, such as Q1 2026 revenue of US$856.2m and net income of US$246.8m. The company is still being priced below some analyst and DCF value estimates. Upcoming index inclusion, an active capital structure reshaping and growing production guidance give the stock more visibility. At the same time, investors also need to weigh dilution, a higher risk funding mix and exposure to permitting, currency and jurisdictional issues in Mexico, the United States and Canada. How those competing forces could affect Coeur Mining’s earnings, cash flow and valuation over the next few years is where the real story starts to get interesting.

Coeur Mining’s expanding production base and recent profitability are only half the story; the real twist sits in how the 3 key rewards and 1 important major warning sign captures where valuation optimism meets one stubborn risk investors often gloss over

Wheaton Precious Metals (TSX:WPM)

Overview: Wheaton Precious Metals is a Vancouver based precious metals streaming company that finances mines in return for the right to buy gold, silver and other metals at pre agreed prices and then sells that production on the open market. It has streams tied to mines across the Americas, Europe and Africa, giving investors exposure to multiple commodities without the direct operational risks of running mines.

Operations: Wheaton Precious Metals generates most of its revenue from the Salobo gold stream at about $1.1b, with additional contributions from silver at Peñasquito at about $360.3m and Antamina at about $328.8m, other silver streams at about $277.1m, and several smaller gold and cobalt contracts.

Market Cap: CA$69.3b

Wheaton Precious Metals catches attention because its streaming model ties it to high quality mines like Salobo while avoiding direct exposure to operating and capital cost blowouts. This structure has supported net margins of 65.6% and recent operating cash flow of $766m. At the same time, the company is leaning on a relatively concentrated asset base and faces questions over long term precious metal demand as investors consider alternatives such as digital assets. Taken together with a premium P/E multiple, a growing dividend and production guidance that points to higher gold equivalent ounces through 2030, investors are left to assess whether that mix of cash generation and growth plans justifies the current valuation over time.

Wheaton Precious Metals’ high margin streaming model and premium P/E are only part of the story; the real question is whether future volumes justify today’s pricing, which is where the analyst forecasts for Wheaton Precious Metals quietly changes the narrative.

The 3 Elite Gold Stocks covered here are just a starting point, and the full screener uncovered 30 more companies with equally compelling balance sheet strength, cost profiles and growth narratives that you can access through the Elite Gold Stocks screener. Use Simply Wall St to identify, filter and analyze the exact catalysts that matter to you, from production costs and funding mix to jurisdiction risk and earnings quality, so you can focus on your highest conviction gold ideas.

Take Control of Your Investment Journey

If Coeur Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About What You Might Be Missing?

Fresh ideas move fast. The next breakout, momentum shift or quietly dropping laggard can get away before the crowd wakes up. While the data still matters, act now.

- Spot fast moving opportunities that still look under the radar using the curated 10 high quality undiscovered gems before momentum sends valuations flying beyond your preferred entry range.

- Lock onto cash generative companies with room to grow by scanning the 6 high quality undervalued stocks while they stay mispriced and sentiment has not fully caught up.

- Secure potential income ideas built on stronger financial footing with the hand picked 6 dividend fortresses before yields compress and prices move away from your comfort zone.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.