Grid Dynamics (GDYN): Profit Margins Jump to 3.4%, Challenging Market Skepticism on Sustained Growth

Grid Dynamics Holdings, Inc. Class A GDYN | 5.70 | +0.35% |

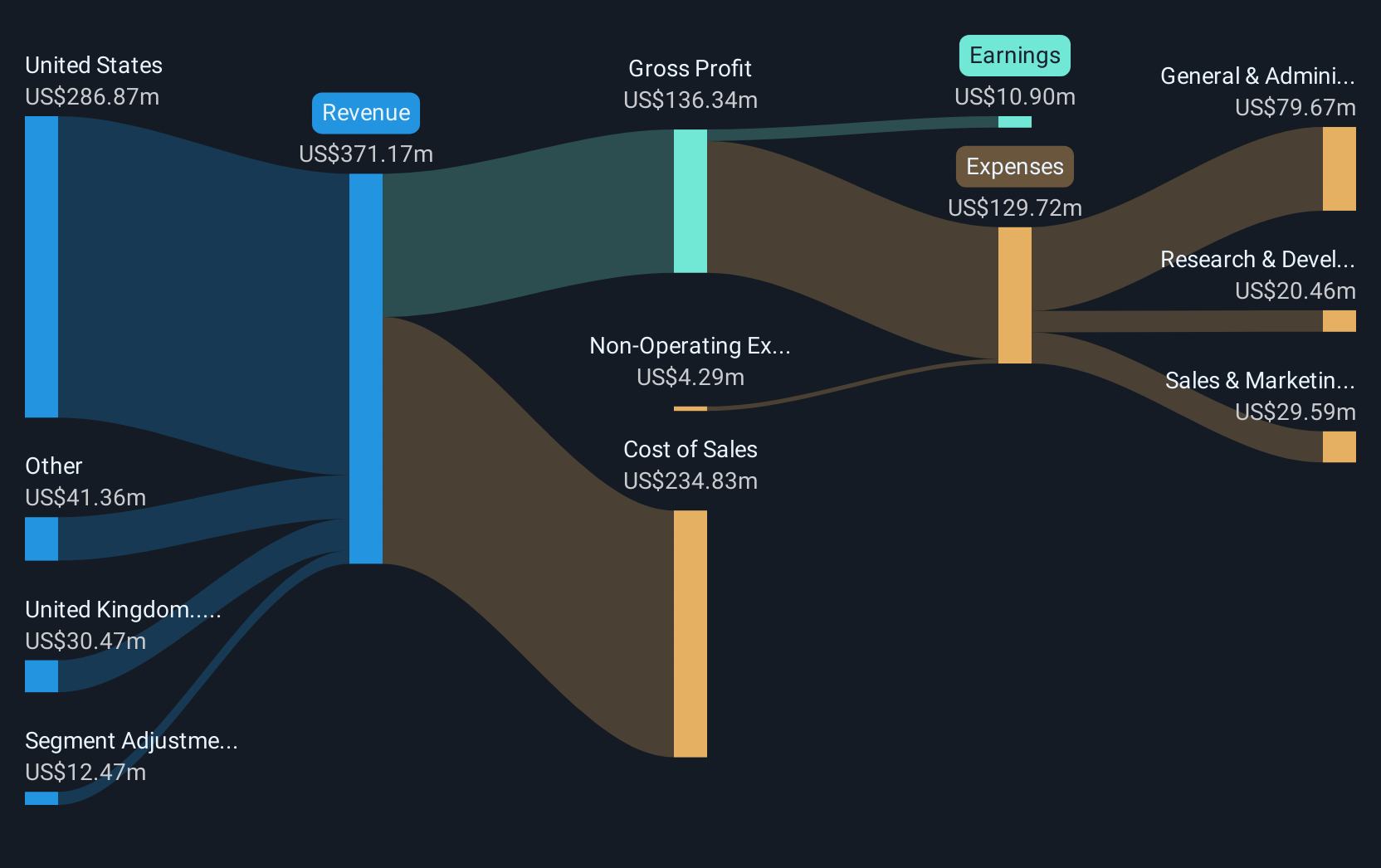

Grid Dynamics Holdings (GDYN) delivered a standout year, averaging 41% annual earnings growth over the past five years, and recently accelerating to a dramatic 474% gain as net profit margins climbed from 0.7% to 3.4%. While forward profit growth of 10.8% per year trails the US market forecast, revenue is projected to rise 11% annually, just ahead of the broader market benchmark. With shares trading below discounted cash flow estimates and rewards in the form of consistent profit growth and improving value relative to peers, investors are sharpening their focus on the company’s expanding profitability and steady margin gains.

See our full analysis for Grid Dynamics Holdings.Now it’s time to see how these headline figures measure up against the market narratives. Let’s dive into where the numbers back up the story and where they might surprise.

AI and Data Projects Fueling Durable Growth

- AI and data projects now make up 23% of Grid Dynamics Holdings' business and are expanding almost three times faster than the rest of the company, shifting the revenue mix toward more recurring, high-value engagements.

- Analysts' consensus view emphasizes that early leadership in enterprise AI and strategic tech partnerships are unlocking faster growth and a more diversified client base.

- Expansion into high-value verticals like financial services and industrial robotics is driving multi-year contracts and increasing average deal value.

- Recurring revenue from AI-centric platform builds and automation projects helps soften the impact of macro slowdowns in specific sectors.

- Insider tip: See how analysts balance these growth drivers against future profit expectations in the full consensus narrative. 📊 Read the full Grid Dynamics Holdings Consensus Narrative.

Margin Pressures Ahead Despite Recent Gains

- Despite net profit margins climbing from 0.7% to 3.4% this year, analysts now model these margins to compress back down to 1.7% by 2027, highlighting growing cost pressures and competitive headwinds.

- Analysts' consensus view flags that rapid international expansion and ongoing investment in proprietary AI solutions could stretch operating leverage.

- Rising global labor costs and wage inflation, especially in India and Europe, may offset efficiency wins from technology upgrades.

- Shrinking client base and greater sector concentration risk could amplify impacts on earnings if major contracts are lost.

Trading Well Below DCF Fair Value

- With the share price at $9.34, Grid Dynamics trades at a 38% discount to its DCF fair value of $15.0, and at a price-to-earnings ratio of 57x, which is less than the peer average (65.6x) but nearly double the broader US IT industry (29.3x).

- Consensus narrative notes this valuation disconnect is striking, as analysts' average price target sits at $12.4 (33% above the current price).

- To justify that target, you would need to believe revenues can reach $551.2 million and earnings hold at $9.5 million by 2028.

- Even then, the projected 191.4x PE multiple in 2028 would be far above industry norms, despite today's lower peer-relative valuation.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Grid Dynamics Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique take on the figures? In just a few minutes, you can craft and share your own market perspective. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Grid Dynamics Holdings.

See What Else Is Out There

Grid Dynamics faces intense cost pressures, shrinking margins, and sector concentration risks. These factors could undermine its earnings growth and long-term profitability.

If you want more dependable performance, turn to stable growth stocks screener (2103 results) to discover companies delivering steady growth even when market conditions get tough.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.