Growth Accolades And New Dividend Policy Could Be A Game Changer For Atour Lifestyle (ATAT)

Atour Lifestyle Holdings Limited ATAT | 0.00 |

- Atour Lifestyle Holdings’ sponsored ADR has attracted attention after earning a top Zacks Rank and strong Growth Score, reflecting robust earnings estimate revisions and financial metrics.

- Separately, the company’s US$0.54 per-share dividend, for which shares went ex-dividend on 5 June 2026 and pay on 22 June 2026, adds an income angle that could appeal to both growth and yield-focused investors.

- With this combination of growth recognition and a newly effective dividend, we’ll assess how these developments influence Atour’s investment narrative today.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Atour Lifestyle Holdings Investment Narrative Recap

To own Atour Lifestyle Holdings, you need to believe in its ability to keep scaling an asset light, experiential hotel and retail model across China while maintaining brand quality and profitability. The Zacks upgrade and dividend news reinforce the current growth focused narrative but do not materially change the key near term catalyst, which is continued execution on hotel expansion, or the main risk, which remains Atour’s concentration in the Chinese market and exposure to local economic and regulatory conditions.

The new US$0.54 per ADS dividend, backed by Atour’s policy to distribute at least half of net income for three years, is the most relevant update here, because it adds a recurring income element to what has largely been a growth story. That income layer may influence how investors weigh the growth catalysts against risks such as intensifying competition and execution challenges in maintaining high standards across a fast growing, franchise heavy network.

However, investors should also be aware that heavy reliance on the Chinese market could become a more pressing issue if...

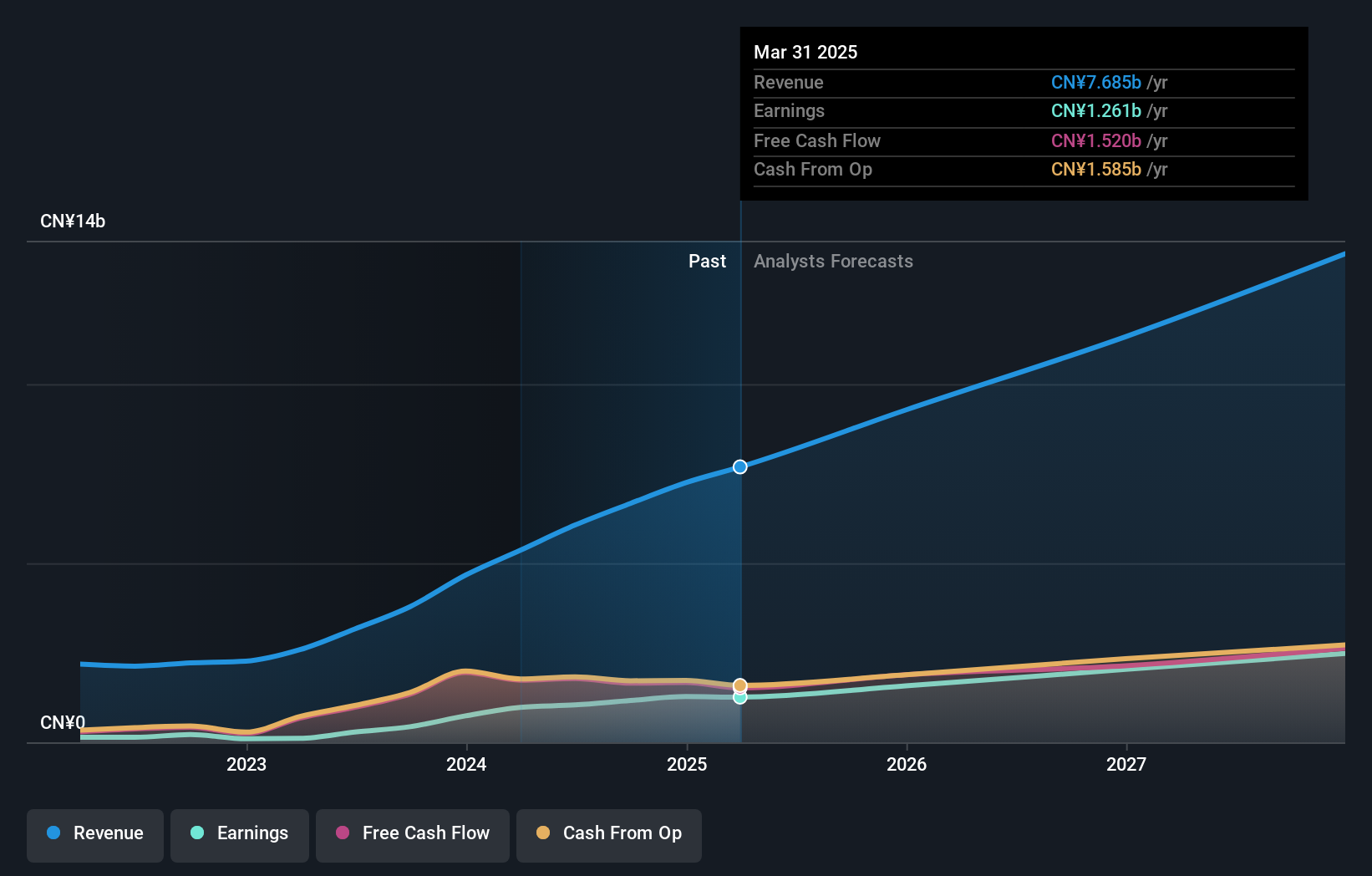

Atour Lifestyle Holdings' narrative projects CN¥18.2 billion revenue and CN¥3.0 billion earnings by 2029. This requires 19.3% yearly revenue growth and about CN¥1.2 billion earnings increase from CN¥1.8 billion today.

Uncover how Atour Lifestyle Holdings' forecasts yield a $50.48 fair value, a 51% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see Atour’s fair value between US$50.48 and US$73.58 per share, highlighting how far opinions can spread. You might weigh those views against the key risk that Atour’s China focused expansion is vulnerable to shifts in domestic demand and policy, then explore which scenarios you find most convincing.

Explore 5 other fair value estimates on Atour Lifestyle Holdings - why the stock might be worth just $50.48!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Atour Lifestyle Holdings research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Atour Lifestyle Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Atour Lifestyle Holdings' overall financial health at a glance.

No Opportunity In Atour Lifestyle Holdings?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.