Harley Davidson (HOG) Index Reshuffle Puts Valuation Back In Focus

Harley-Davidson, Inc. HOG | 0.00 |

Index reshuffle puts Harley-Davidson in focus

Harley-Davidson (HOG) has shifted across several Russell indexes, moving out of Russell 1000 and Midcap benchmarks and into multiple Russell 2000 value and defensive indexes, prompting index fund trading adjustments.

Alongside the index reshuffle and a recent leadership change in its legal and compliance role, Harley-Davidson's share price has moved to US$24.46, with a 90-day share price return of 20.31% but a 5-year total shareholder return that is down 40.49%. This suggests that shorter term momentum contrasts with weaker long term outcomes.

If index moves have you thinking about where capital might shift next, it could be worth broadening your watchlist with 20 top founder-led companies

With Harley-Davidson now sitting in small cap value and defensive indexes, a share price near US$24, and long term returns that trail its recent bounce, the key question is whether the stock is undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 4.6% Undervalued

On the most followed narrative, Harley-Davidson's fair value of $25.64 sits modestly above the $24.46 last close, framing a small undervaluation that depends on execution, capital allocation, and product mix shifts.

The new partnership in HDFS unlocks significant cash ($1.25B) and reduces leverage, enabling accelerated share buybacks and freeing up $300M for growth investments, which can directly bolster EPS and future revenue streams through both financial engineering and new business initiatives.

Want to see how this cash injection is modeled into Harley-Davidson's future earnings and margins, and what kind of valuation multiple the narrative needs to make the numbers work?

Result: Fair Value of $25.64 (UNDERVALUED)

However, Harley-Davidson still faces weak motorcycle demand and an aging core rider base, while tariff costs and slow LiveWire uptake could quickly challenge this view of the company as undervalued.

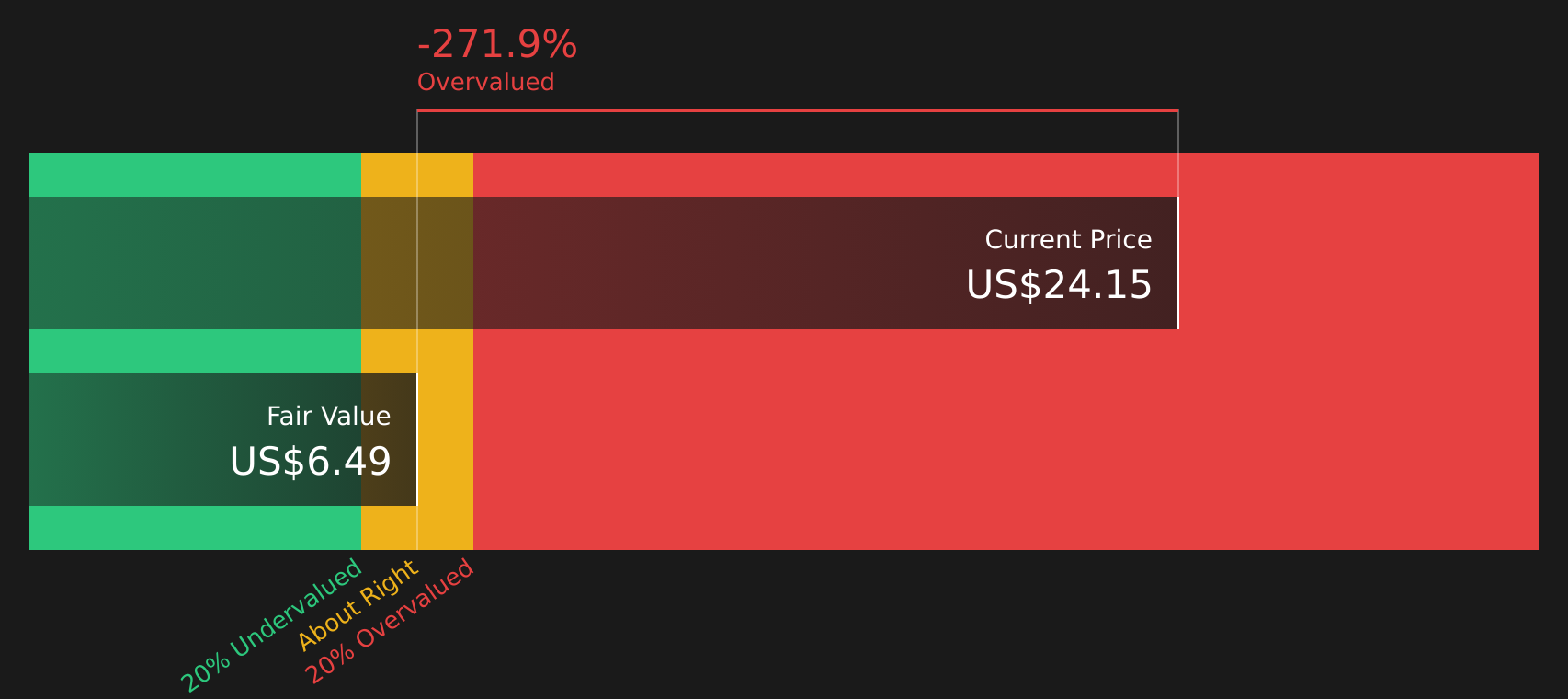

Another View on Harley-Davidson's Valuation

The earlier narrative framed Harley-Davidson as about 4.6% undervalued using analyst assumptions around earnings, margins, and a future P/E near 13.4x. The SWS DCF model tells a very different story, with an estimated future cash flow value of $9.31 compared with the current share price of $24.46, implying the stock is trading well above that cash flow based estimate and raising questions about how dependable those longer term forecasts really are.

For readers who want to see how this cash flow based view is built line by line, take a closer look at the SWS DCF model behind Harley-Davidson's valuation: Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Harley-Davidson for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of risks and rewards around Harley-Davidson leaves you uncertain, act promptly and test the assumptions against your own expectations, then weigh the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Harley-Davidson?

Consider expanding your research beyond Harley-Davidson so you are not relying on a single story when fresh ideas could be one screen away.

- Target dependable income and cash flow resilience by checking companies in the 10 dividend fortresses.

- Look for quality at a reasonable price by scanning the 43 high quality undervalued stocks.

- Identify potential future standouts early by reviewing the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.