Has Charter Communications (CHTR) Fallen Far Enough To Look Undervalued?

Charter Communications, Inc. Class A CHTR | 0.00 |

Charter Communications stock has had a tough run over the last few years, yet its valuation checks currently lean cheap. This sets up a clear tension between the share price slide and what the broader metrics imply about value.

- Over the past 5 years, Charter Communications has declined about 81.5%, which means long term holders have seen a substantial erosion in market value.

- For today’s valuation, the key support is whether the core subscription and broadband cash flows can remain resilient. A central risk is that ongoing capital needs and competitive pressure could weigh on margins and investor confidence in those cash flows.

- On Simply Wall St’s checks, Charter Communications screens as undervalued in 5 of 6 areas, so the broader set of valuation metrics currently leans toward the stock being cheap rather than expensive.

The issue now is whether the present share price fairly reflects the risks around Charter Communications, or if the valuation gap suggested by the checks points to a mispricing.

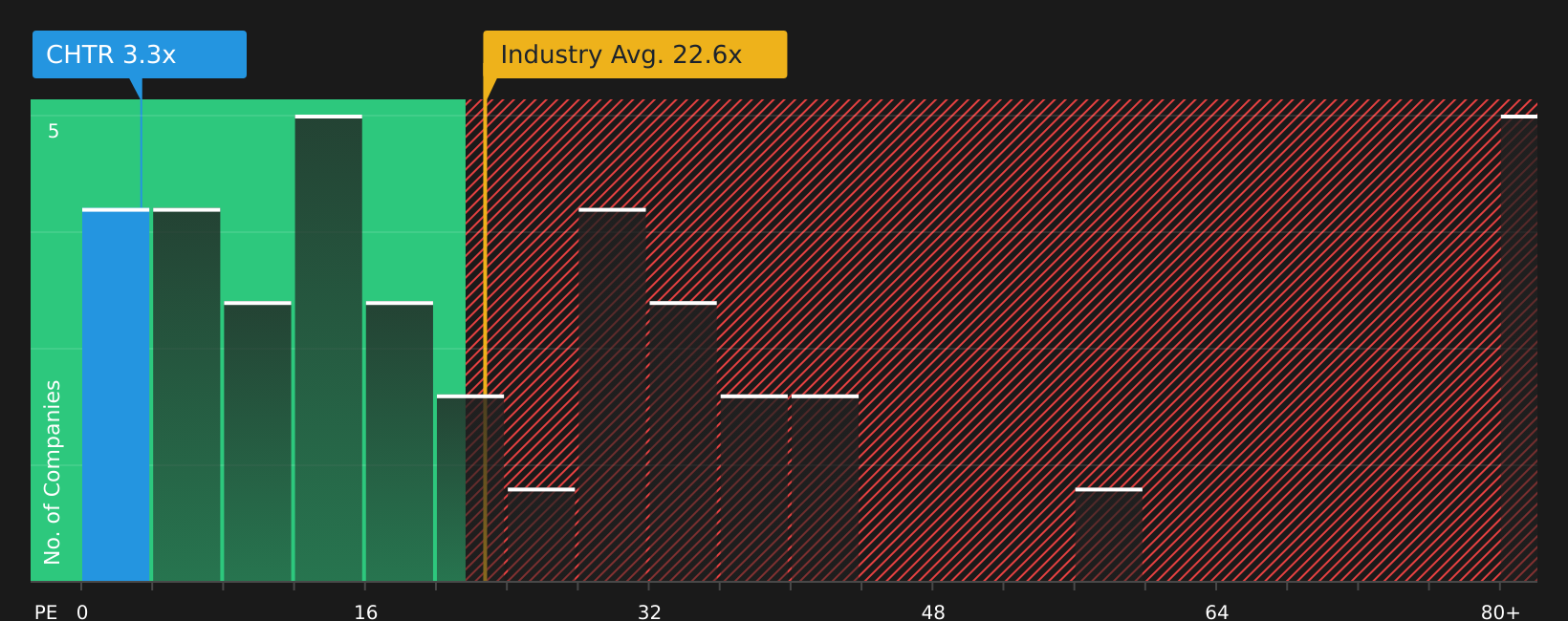

Is Charter Communications a Bargain on Earnings?

The P/E ratio fits Charter Communications well because earnings are still a key reference point for how investors value its subscription and broadband business. On this measure, the stock trades at about 3.3x earnings, which sits far below the Media industry average of roughly 22.6x and also below the broader peer average of about 29.7x.

The fair P/E ratio implied by the checks is 17.6x, which reflects what investors might typically pay for a company with Charter Communications' characteristics rather than just a sector average. The gap between the current 3.3x and this 17.6x fair level is wide, and this suggests the market is pricing in a lot of risk or skepticism relative to what the model implies.

On the P/E multiple alone, Charter Communications stock appears inexpensive compared with both its tailored fair ratio and its industry benchmarks.

The Charter Communications Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around Charter Communications and explain which assumptions on future growth, margins and earnings would need to hold for the stock to be worth materially more or materially less than today’s price. They are available on the company’s Community page. Each narrative links a fair value estimate to a particular set of potential catalysts and risks, so you can see over time which version of Charter Communications' story appears to be taking shape.

Charter Communications investors are weighing two very different stories about where the broadband and cash flow picture could head next.

Bull case: 65% undervalued

"With peak capital intensity passing and new federal tax legislation set to deliver billions in permanent cash tax savings, Charter is entering a phase of rapidly accelerating free cash flow per share, combined with aggressive buybacks and falling share count, suggesting significant outperformance on earnings growth and shareholder returns relative to what is currently priced into the stock..."

Bear case: 8% overvalued

"Charter Communications faces persistent broadband subscriber losses amid heightened competition from 5G and fixed wireless access providers, threatening the company's ability to return to meaningful broadband customer growth and putting long-term revenue expansion at risk..."

Do you think there's more to the story for Charter Communications? Head over to our Community to see what others are saying!

The Bottom Line

Charter Communications screens as undervalued on market multiples, with a P/E that sits well below both sector and tailored fair-value benchmarks, so the current discount is hard to ignore. The tension is whether that gap reflects genuine mispricing or a market that is correctly bracing for pressure on broadband cash flows and ongoing capital needs. For you as an investor, the key question is simple but uncomfortable: whether Charter Communications can keep its core earnings and cash generation resilient enough for the valuation gap to close, or whether this remains a value trap where the low multiple largely mirrors the underlying risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.