Has Clover Health Investments (CLOV) Share Surge Left More Room Based On Cash Flow Value?

Clover Health CLOV | 0.00 |

- Wondering whether Clover Health Investments at US$2.82 is still a bargain or already pricing in its prospects? This breakdown will help you judge what you are really paying for.

- The stock has had a strong run over shorter periods, with returns of 2.5% over 7 days, 48.4% over 30 days and 17.0% year to date. However, the 1 year return sits at a 24.8% decline and the 3 year return is very large at 196.7% compared to a 61.2% decline over 5 years.

- Recent headlines have focused on the company as a healthcare player using technology to manage medical costs and member care. This helps frame how investors think about its potential and risk profile. These themes often influence sentiment around future cash flows and can help explain why the share price has been so sensitive over different time frames.

- Clover Health Investments currently scores 5 out of 6 on our valuation checks. This 5/6 valuation score sets up a closer look at common methods such as DCF and multiples, before turning to a more complete way of thinking about value at the end of this article.

Approach 1: Clover Health Investments Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows and discounts them back to today’s dollars, aiming to estimate what the entire business could be worth right now.

For Clover Health Investments, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections expressed in $. The latest twelve month free cash flow is $55.13 million. Analysts provide estimates for the near term, including an expected free cash flow loss of $63.09 million in 2024, and Simply Wall St extrapolates further out to create a 10 year path.

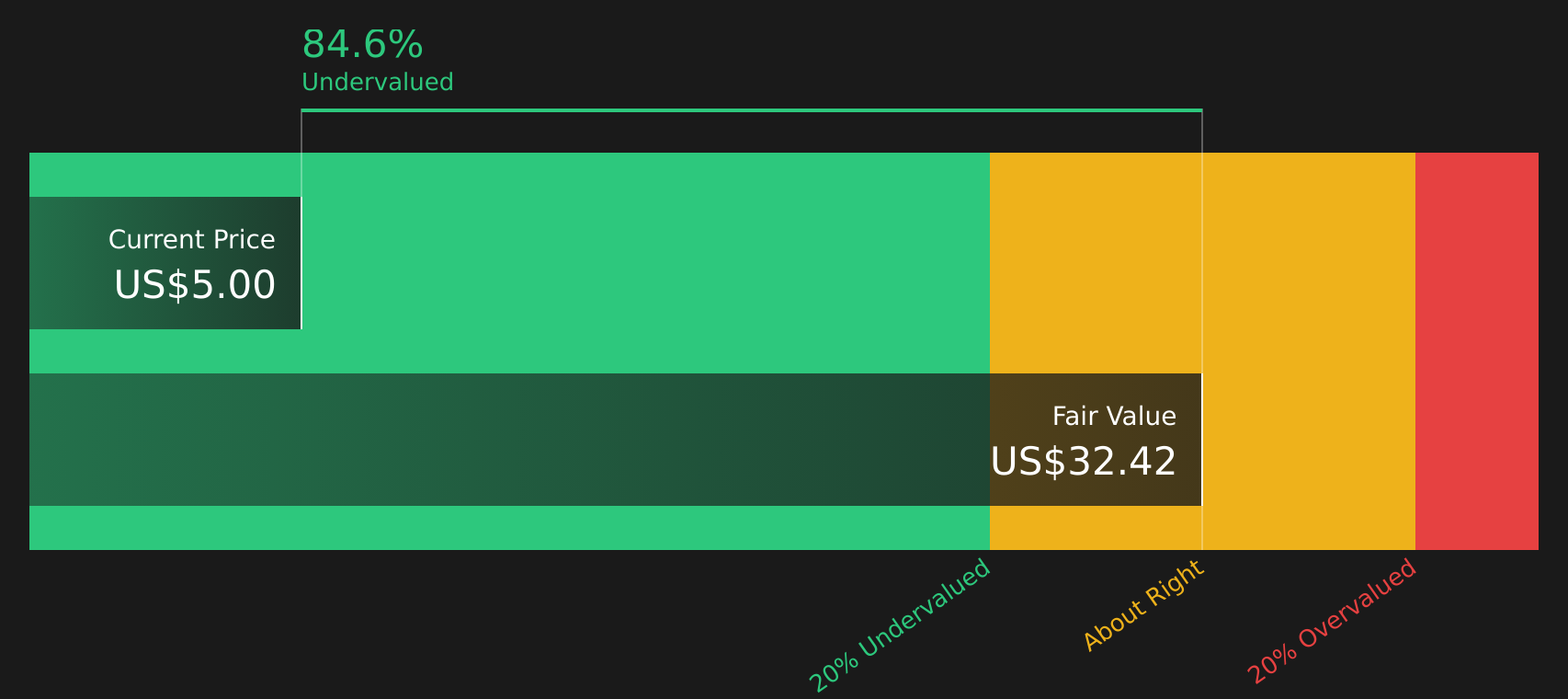

By 2035, the projection in this model reaches $934.41 million in free cash flow, with a discounted value of $470.24 million. Aggregating these discounted cash flows and applying a terminal value gives an estimated intrinsic value of $32.48 per share.

Compared with the current share price of about $2.82, this DCF output implies the stock is 91.3% undervalued on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Clover Health Investments is undervalued by 91.3%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Clover Health Investments Price vs Sales

For companies where earnings are not yet a steady guide, the P/S ratio is often a useful way to think about what you are paying for each dollar of revenue. It is simpler than P/E, but it still reflects how the market balances expectations for growth and the risk that those expectations may not play out as hoped.

Clover Health Investments currently trades on a P/S ratio of 0.67x. That sits below both the Healthcare industry average P/S of 1.21x and a peer group average of 1.92x. On the surface, that suggests the stock is priced more conservatively than many of its listed healthcare peers.

Simply Wall St’s Fair Ratio for Clover Health Investments is 0.82x. This is a proprietary estimate of what a reasonable P/S might be, after considering factors such as earnings growth, profit margins, industry, market value and key risks. Because it adjusts for these company specific traits, the Fair Ratio can be a more tailored reference point than a broad industry or peer average. Comparing the Fair Ratio of 0.82x with the current P/S of 0.67x points to the stock trading below that indicated range.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Clover Health Investments Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring your view of Clover Health Investments together in one place by tying the story you believe in to specific revenue, earnings and margin assumptions, rolling those into a fair value, comparing that to the current price to help you decide whether the stock looks attractive or stretched, and then automatically refreshing that view when new earnings, guidance or news arrive. All of this is available within Simply Wall St’s Community page, where you can see how other investors frame the same stock. For example, you can see one Narrative that aligns with a more optimistic fair value of about US$3.20, and another that aligns with a more cautious fair value of about US$2.50.

For Clover Health Investments, here are previews of two leading Clover Health Investments narratives:

Fair value used in this bullish narrative: US$3.20

Implied discount to this fair value at the last close of US$2.82: about 11.9% undervalued

Revenue growth assumption: 27.68%

- Focuses on Clover Health Investments as a potential beneficiary of wider access to data and interoperability rules, which this narrative links to stronger membership, revenue, and margin potential.

- Highlights the role of Clover Assistant and Counterpart Health in creating possible multi sided platform effects, including recurring SaaS like revenue streams alongside insurance activity.

- Builds its fair value on analyst assumptions for faster revenue growth, a move from a loss to earnings of US$57.9 million by about 2029, and a higher future P/E multiple compared with the broader US Healthcare sector.

Fair value used in this more cautious narrative: US$2.82

Implied premium to this fair value at the last close of US$2.82: 0.0% overvalued

Revenue growth assumption: 24.37%

- Frames Clover Health Investments as closely aligned with analyst consensus, using assumptions that point to solid revenue growth but a more measured path to profitability.

- Emphasises ongoing risks around medical cost trends, regulatory changes, and competition from larger insurers, which this narrative sees as constraints on future margins and earnings.

- Arrives at a fair value that sits close to the recent share price, using earnings of US$31.7 million by about 2029 and a high future P/E multiple as key inputs, while stressing that readers should test these assumptions against their own expectations.

Do you think there's more to the story for Clover Health Investments? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.