Has DoorDash (DASH) Become Attractive After Its Recent Share Price Slump?

DoorDash, Inc. Class A DASH | 156.45 | +3.95% |

- If you are wondering whether DoorDash's current share price reflects its true worth, you are not alone. This article will walk you through what the numbers actually say about its value.

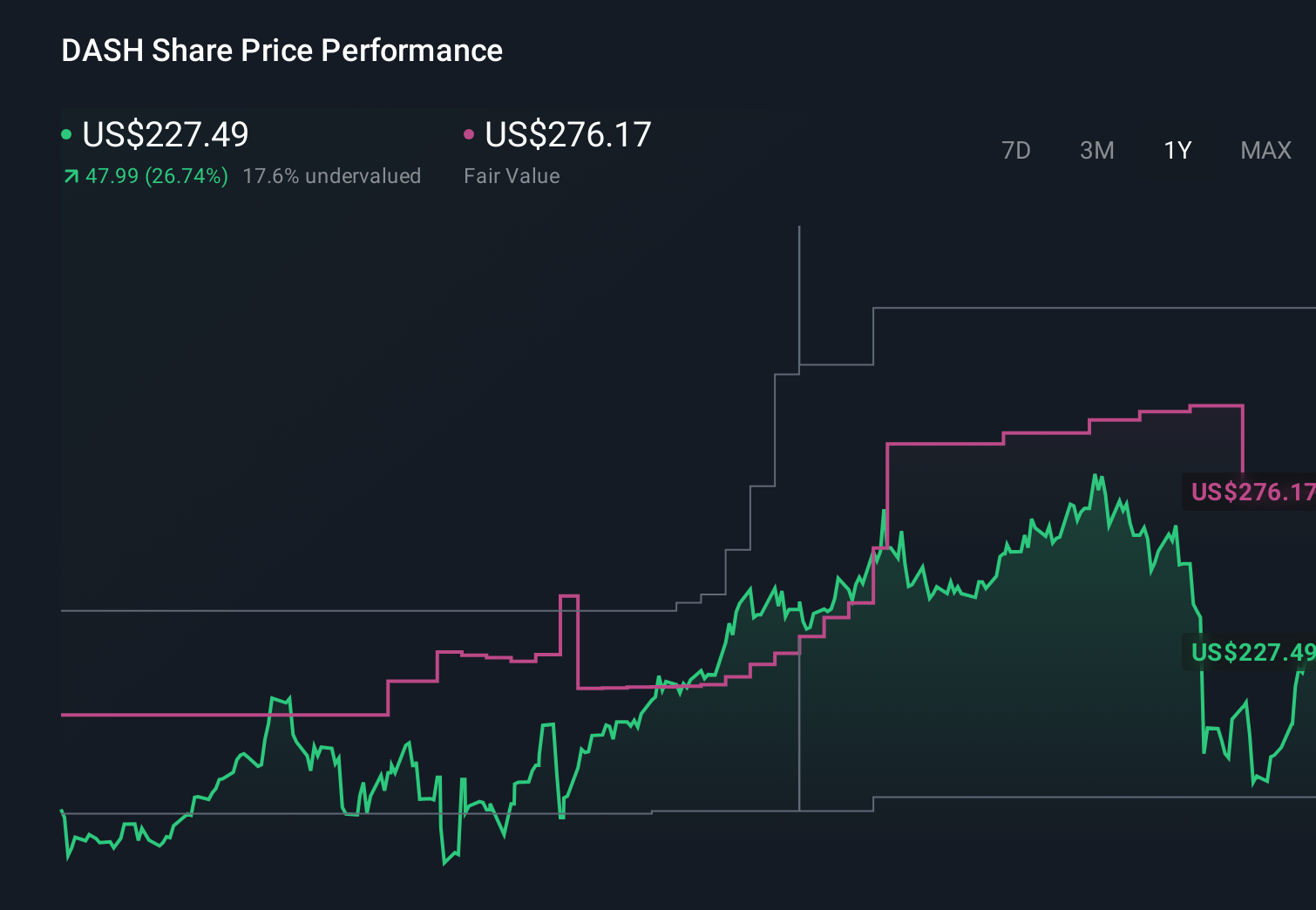

- The stock has been volatile recently, with a 13.6% decline over the last 7 days, a 21.9% decline over the last 30 days, and a 27.0% decline year to date, although its 3 year return sits at 176.2%.

- Recent coverage has focused on DoorDash's position in food delivery and local commerce, including debates around how sustainable its scale and growth investments might be in a competitive sector. These discussions help frame whether the recent share price weakness is a reset in expectations or simply part of a longer term story that investors are still pricing.

- Our valuation checks currently give DoorDash a 3 out of 6 valuation score. Next, we will compare different methods to judge whether that feels fair, before finishing with a more holistic way to think about value that many investors overlook.

Approach 1: DoorDash Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes forecasts of a company’s future cash flows and discounts them back to today using a required return, to estimate what the business might be worth right now.

For DoorDash, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $2.0b. Analysts provide the nearer term estimates, and Simply Wall St extrapolates further out, with projected free cash flow of about $8.9b by 2030 and a series of annual projections between 2026 and 2035 that feed into the valuation.

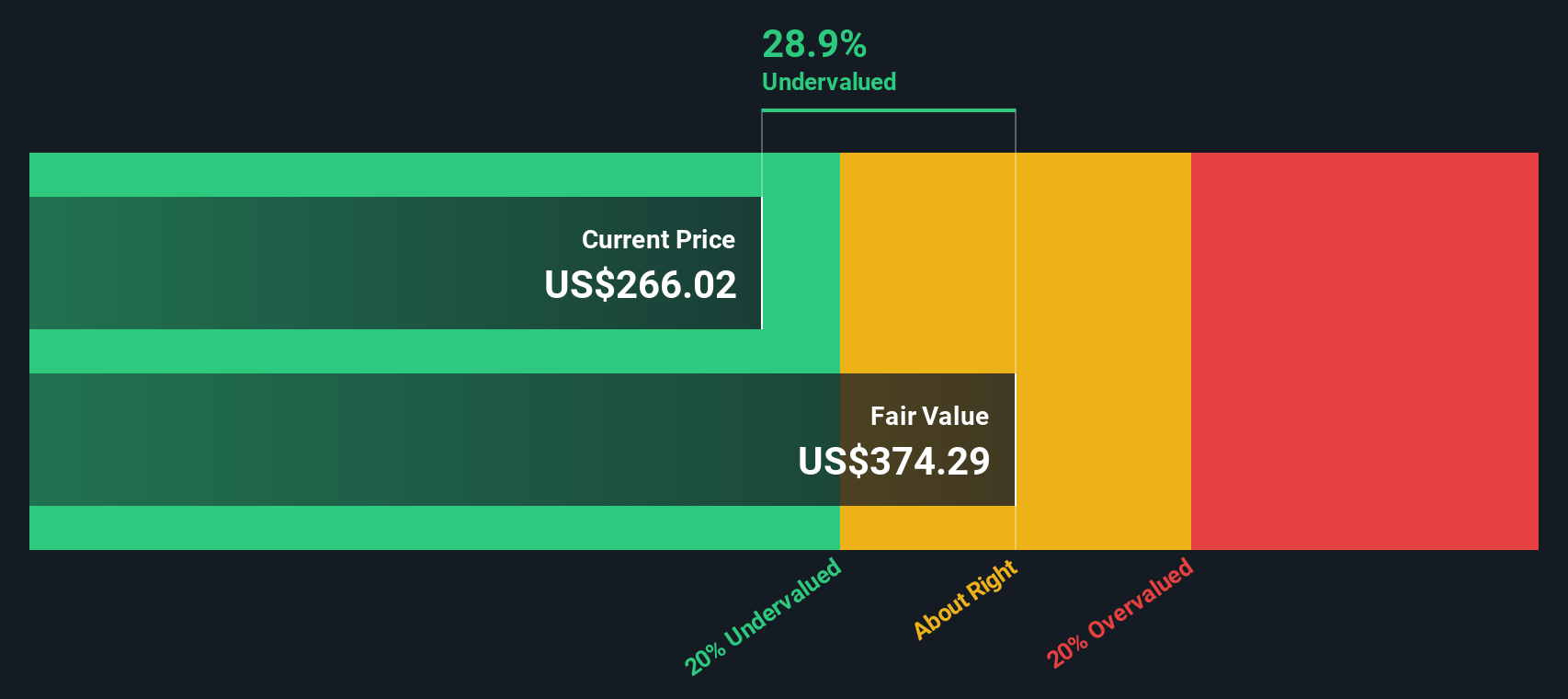

Putting these cash flows together, the DCF model points to an estimated intrinsic value of about $436.76 per share. Compared with the current share price, this implies the stock is 63.3% undervalued according to this specific set of assumptions and cash flow projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DoorDash is undervalued by 63.3%. Track this in your watchlist or portfolio, or discover 55 more high quality undervalued stocks.

Approach 2: DoorDash Price vs Earnings

For a profitable company, the P/E ratio is a useful shorthand because it connects what you pay per share with the earnings that support that price. It lets you compare companies of different sizes on the same earnings based yardstick.

What counts as a fair P/E usually reflects growth expectations and risk. Higher expected earnings growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk tends to go with a lower one.

DoorDash currently trades on a P/E of 80.08x. That sits well above the Hospitality industry average of 21.36x and also above the peer group average of 40.69x. Simply Wall St’s Fair Ratio for DoorDash is 47.25x, which is its proprietary estimate of what a reasonable P/E could be given factors such as earnings growth, profit margins, industry, market cap and specific risks.

Because the Fair Ratio blends these fundamentals rather than relying only on broad peer or industry comparisons, it can give a more tailored view of what investors might be willing to pay for each dollar of earnings.

With DoorDash’s actual P/E of 80.08x sitting well above the Fair Ratio of 47.25x, this approach points to the shares being expensive on an earnings basis.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your DoorDash Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company linked directly to your own assumptions for fair value, future revenue, earnings and margins, and then compared with the current price.

On Simply Wall St, Narratives live in the Community page and are used by millions of investors as an easy tool to connect a company’s story to a financial forecast, so you can see a Fair Value that updates automatically when new news, earnings or guidance arrive.

For DoorDash, one Narrative might be cautious, with a fair value around US$91.21 or US$212.04. A more optimistic Narrative might see fair value closer to US$274.69 or even US$342.22. By comparing any of these Fair Values to the current DoorDash share price you can decide for yourself whether the stock looks expensive or cheap relative to the story you believe.

For DoorDash, however, we will make it really easy for you with previews of two leading DoorDash Narratives:

First is a bullish take built around global scale, AI and higher long term margins.

Fair value: US$274.69

Implied discount to fair value vs last close: about 42%

Assumed annual revenue growth: 24.24%

- The thesis centers on DoorDash as a global commerce and tech platform, expanding beyond restaurants into grocery, retail and other verticals, with AI expected to improve efficiency over time.

- Analysts in this narrative expect higher future profit margins and earnings compared to today, supported by advertising, software tools and international expansion, although they also flag execution and regulatory risks.

- The fair value of about US$274.69 reflects those higher long term earnings assumptions, a future P/E in the high 40s and a discount rate just over 8%, with readers encouraged to test whether those inputs match their own expectations.

On the other side is a more cautious view that focuses on what happens if the market is paying too much for that story.

Fair value: US$91.21

Implied premium to fair value vs last close: about 76%

Assumed annual revenue change: 1.58% decline

- This narrative argues that DoorDash is already priced for very strong success, with the share price viewed as well above a more conservative cash flow based floor that assumes slower growth and lower profitability.

- It highlights upcoming earnings events, heavier investment plans and regulatory or competitive pressures as potential triggers for a reset if profitability or guidance does not keep up with expectations.

- The fair value of about US$91.21 is framed as a downside anchor if growth, margins or capital allocation fall short, suggesting limited room for disappointment at current levels.

These two Narratives use the same company but very different assumptions about revenue growth, margins and what multiple the market might eventually be willing to pay. That is the real power of Narratives, because they make it clear which story you are actually backing each time you look at the DoorDash share price.

If you want to see how other investors are connecting their own expectations to price, you can review the full set of Narratives for DoorDash, compare the inputs and decide which story, if any, lines up with your view before making any moves.

Do you think there's more to the story for DoorDash? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.