Has FMC (FMC) Fallen Far Enough To Be A Bargain?

FMC Corporation FMC | 0.00 |

FMC stock is coming off a difficult stretch, with the share price well below past levels, yet both the intrinsic value estimate using a Discounted Cash Flow (DCF) approach and the market multiples currently point to the shares trading at a discount to underlying value.

- FMC shareholders have seen the stock decline 87.6% over the past 3 years, which puts the current valuation front and center for anyone considering whether the reset has gone too far.

- Recent steps to raise cash, including a planned US$400 million minority investment from Tessenderlo Group and a US$114 million property sale with proceeds earmarked for debt reduction, can support balance sheet repair but also underline that leverage remains a key risk for how the market prices FMC.

- On Simply Wall St's broader checks, FMC screens as undervalued in 5 of 6 measures, which means the overall valuation picture leans cheap based on this 5/6 value score.

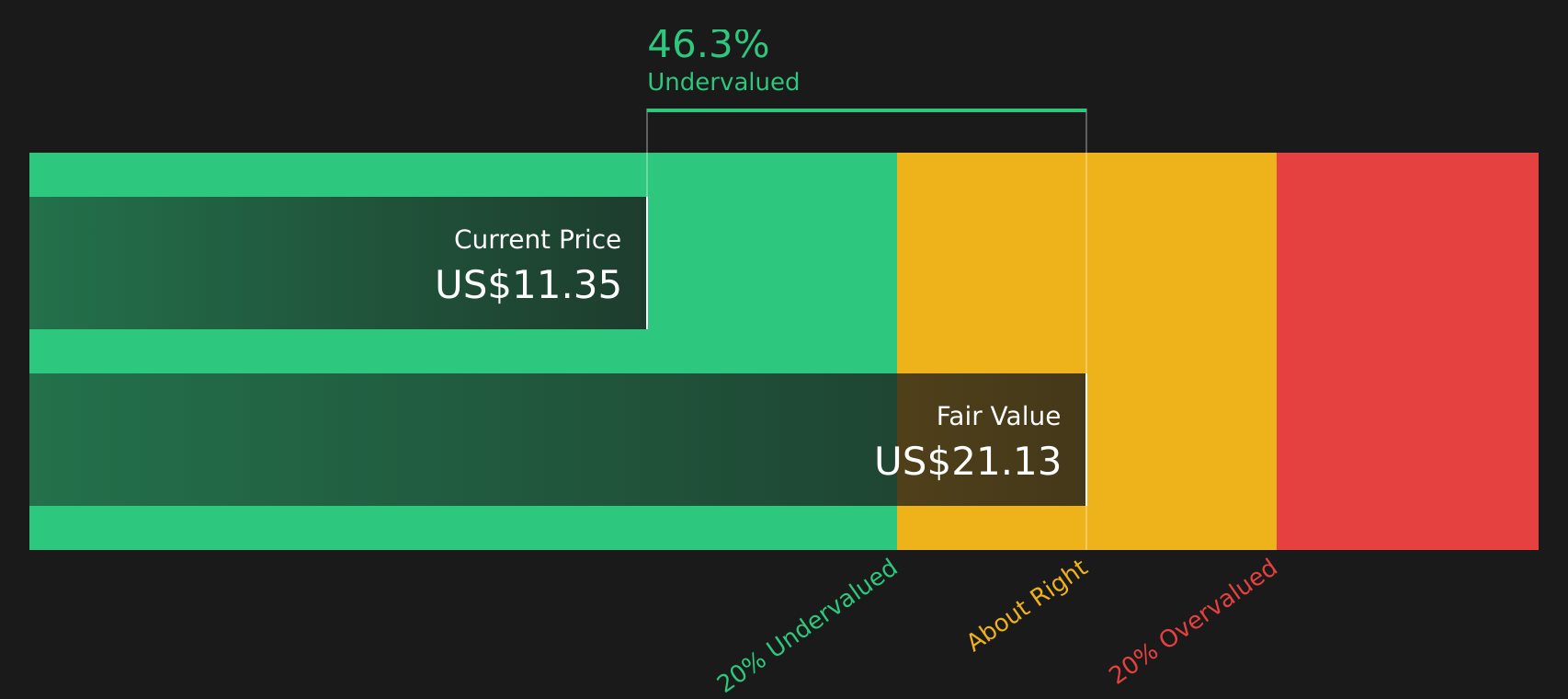

The issue now is whether FMC's current discount, including an intrinsic value estimate that suggests the stock trades roughly 48.7% below its DCF-based fair value, offers enough margin of safety given its recent share price performance and debt reduction plans.

Is FMC a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what FMC might be worth today. For FMC, the latest twelve month free cash flow shows a use of cash of about US$214.0 million. The model assumes free cash flow recovers to positive levels over time and stays in a growing but moderating range.

Based on those cash flow projections, the DCF output suggests an intrinsic value of about $22.14 per share. This implies FMC trades at roughly a 48.7% discount to that estimate. Because the planned US$400 million minority investment from Tessenderlo is earmarked for debt reduction, the market may still be weighing balance sheet risk heavily, even though the cash flow based value screens higher than the share price.

Overall, the DCF workup indicates FMC stock currently appears undervalued relative to the cash flows implied in this model.

Our Discounted Cash Flow (DCF) analysis suggests FMC is undervalued by 48.7%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Is FMC Still Cheap on Sales?

For FMC, the P/S multiple is a useful cross check because it compares the value of the stock to its revenue rather than its current earnings swings.

FMC trades on a P/S of about 0.4x, which is well below the Chemicals industry average of about 1.0x and also under the peer group average of roughly 1.3x. The tailored fair P/S ratio for FMC, which reflects its sector, size and risk profile, is higher at about 1.6x, so the current sales multiple is far under what this framework suggests could be reasonable.

That gap means the market is valuing FMC’s sales at a meaningful discount to both industry norms and the model’s fair ratio, even after the recent funding and asset sale plans aimed at reducing debt.

On this P/S measure, FMC stock appears undervalued relative to both the sector and the fair multiple implied by its profile.

The FMC Narrative: What Would Justify Today's Price?

FMC's valuation story so far raises a clear question, which Simply Wall St Narratives aim to answer by explaining what mix of future growth, margins and earnings would need to align for the stock to be worth meaningfully more or less than today’s price on the Community page. Where a single ratio or model gives a point estimate, these scenarios set out the underlying expectations so you can later judge whether reality is tracking them.

One of the top community narratives on FMC: 35% undervalued

"Cost restructuring and shifts in how FMC goes to market are expected to free up capital and support future earnings growth and cash flow…"

Do you think there's more to the story for FMC? Head over to our Community to see what others are saying!

The Bottom Line

FMC looks cheap on both the Discounted Cash Flow (DCF) intrinsic value estimate and on sales based multiples, which together point to an undervalued stock rather than a one off model quirk. The core question is whether FMC can reduce leverage and stabilise cash flows enough for the market to give it more credit for those cash generation assumptions. If you think balance sheet repair and cash discipline can stick, the current discount may look like mispricing, but if debt and execution worries prove persistent, that gap can just as easily reflect a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.