Has Huron Consulting Group’s New Strategic Partnership Unlocked Value for Investors?

Huron Consulting Group Inc. HURN | 127.49 127.49 | +1.13% 0.00% Pre |

- Ever wondered whether Huron Consulting Group is a bargain or priced for perfection? If you are curious about where the stock stands on value right now, you are not alone.

- Recently, the stock has been anything but quiet, climbing 8.2% this past week, 9.7% over the last month, and delivering a remarkable 33.7% gain year-to-date.

- These sharp moves have been drawing attention, especially following Huron’s recent announcement of a new strategic partnership and industry accolade. Both of these developments have helped fuel investor optimism. Headlines around management initiatives and market recognition have provided fresh context for why the shares have been on the move.

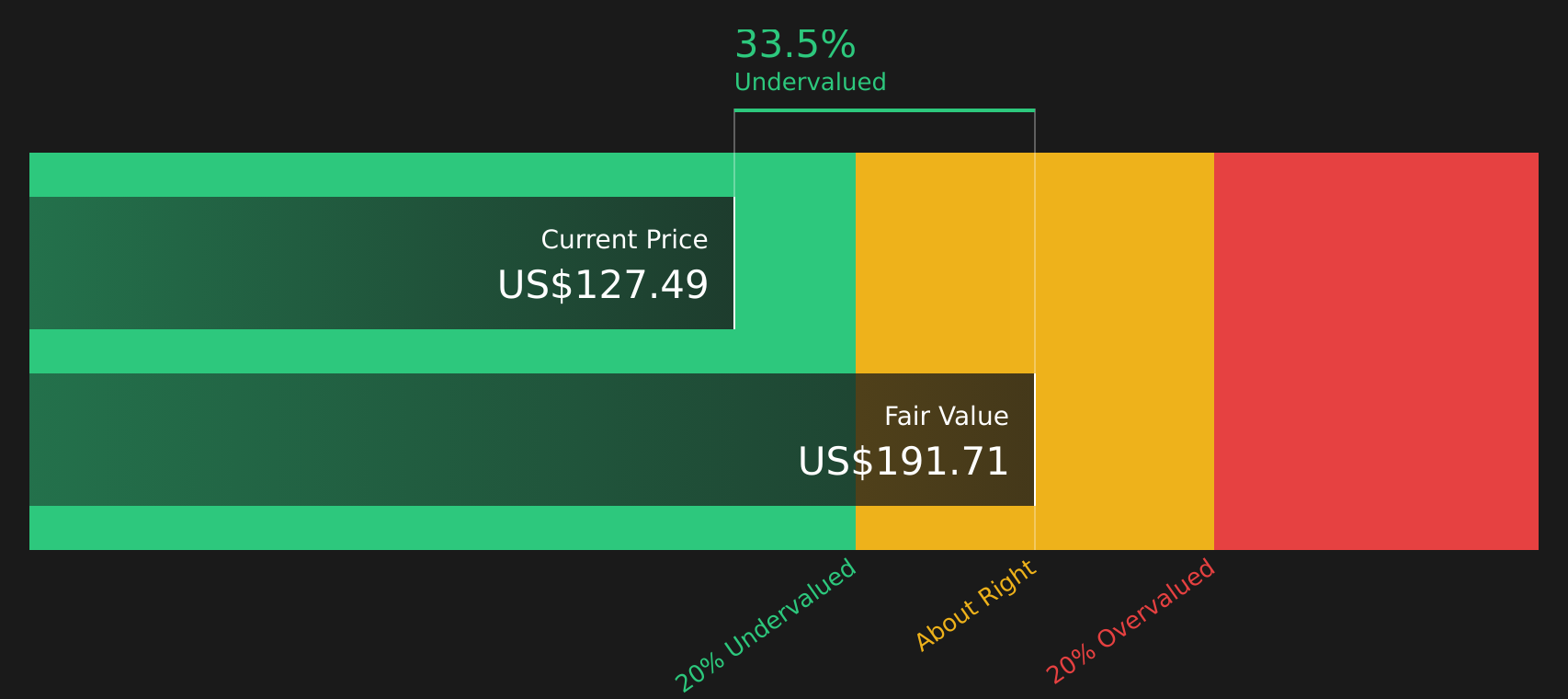

- On our broad value assessment, Huron Consulting Group scores a solid 5 out of 6, meaning the stock appears undervalued on most traditional checks, which is something we will dig into next. Yet, there is more to valuation than just the usual numbers, and our article will end with a perspective that could change how you judge value entirely.

Approach 1: Huron Consulting Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by forecasting its future cash flows and discounting them back to today’s value. This approach helps investors understand what the business is fundamentally worth, regardless of the current market mood.

For Huron Consulting Group, the DCF analysis starts with the company’s latest Free Cash Flow of $170.2 million. Analysts provide direct estimates for several years, projecting continued growth in Free Cash Flow. Over the next decade, Simply Wall St extrapolates these estimates, with 2035’s cash flow projected at $333.8 million and discounted accordingly.

Based on these projections, the resulting intrinsic value for Huron is calculated to be $357.30 per share. When compared to today’s price, this implies the stock is trading at a 53.8% discount to its intrinsic value, suggesting a meaningful undervaluation at this time.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Huron Consulting Group is undervalued by 53.8%. Track this in your watchlist or portfolio, or discover 842 more undervalued stocks based on cash flows.

Approach 2: Huron Consulting Group Price vs Earnings

For established, profitable companies like Huron Consulting Group, the Price-to-Earnings (PE) ratio is generally the go-to valuation metric. It is straightforward, comparing the company's stock price to its per-share earnings, making it especially useful for companies with steady profits and a history of growth.

A company’s PE ratio tells you what investors are willing to pay per dollar of earnings. Generally, higher growth expectations and lower risks justify a higher PE ratio, while slower growth or greater risk tends to lower what is considered a “normal” multiple. That means not every company should command the same PE. Context is key.

Huron’s current PE ratio is 24.3x. That is slightly below the Professional Services industry average of 25.1x, and well under the peer average of 40.7x. However, using Simply Wall St’s proprietary “Fair Ratio,” which models an expected multiple based on Huron’s earnings growth, profit margins, industry factors, market cap, and specific risks, the fair PE for Huron is estimated at 26.6x. This approach goes deeper than standard industry or peer comparisons by accounting for what is unique about Huron instead of using a one-size-fits-all benchmark.

With the current PE of 24.3x below the Fair Ratio of 26.6x, Huron appears undervalued by this measure, suggesting some potential upside if the stock were to re-rate toward fair value.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1409 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Huron Consulting Group Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story about a company, a way to connect your view of Huron Consulting Group’s prospects to the numbers behind its fair value. Rather than focusing purely on today’s data, Narratives let you explain why you think future revenue, earnings, and profit margins will move in a certain direction, creating a living link between the company’s story and what you believe it should be worth.

Narratives are easy to create and follow on Simply Wall St’s Community page, where millions of investors share their perspectives. They empower you to make confident decisions about when to buy or sell, since you can compare your own Fair Value estimate to the current share price at a glance. Best of all, Narratives update dynamically as the latest news, earnings, and data arrive, helping your analysis stay in sync with real events.

For example, some investors believe Huron’s digital transformation push and disciplined acquisitions will drive high double-digit earnings growth and value the stock at $214 per share. Others, concerned by heavy reliance on healthcare clients and competition, see fair value closer to $152. Narratives put these perspectives and how they shape fair value right at your fingertips.

Do you think there's more to the story for Huron Consulting Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.