Has Intuitive Surgical (ISRG) Fallen Below Fair Value After Recall News?

Intuitive Surgical, Inc. ISRG | 0.00 |

Intuitive Surgical stock has slid about 30.8% year to date, yet the Discounted Cash Flow (DCF) intrinsic value estimate still points to meaningful upside while earnings based multiples signal the shares look expensive and the broader valuation checks are weak.

- With the share price down 30.8% year to date, recent weakness has opened up a debate over whether the current level reflects pressure on sentiment more than a reset in long term prospects.

- Growth hopes around expanding robotic procedure volumes and AI driven tools can support richer expectations, but product recall headlines and competition from larger medical device peers may weigh on what investors are willing to pay.

- Intuitive Surgical scores only 2 out of 6 on our valuation checks, which leans more toward an expensive stock than a clear bargain on the wider set of metrics.

The issue now is whether the intrinsic value case or the more cautious market multiple and value score view is a better guide to where Intuitive Surgical stock belongs.

Is Intuitive Surgical a Bargain on Cash Flow?

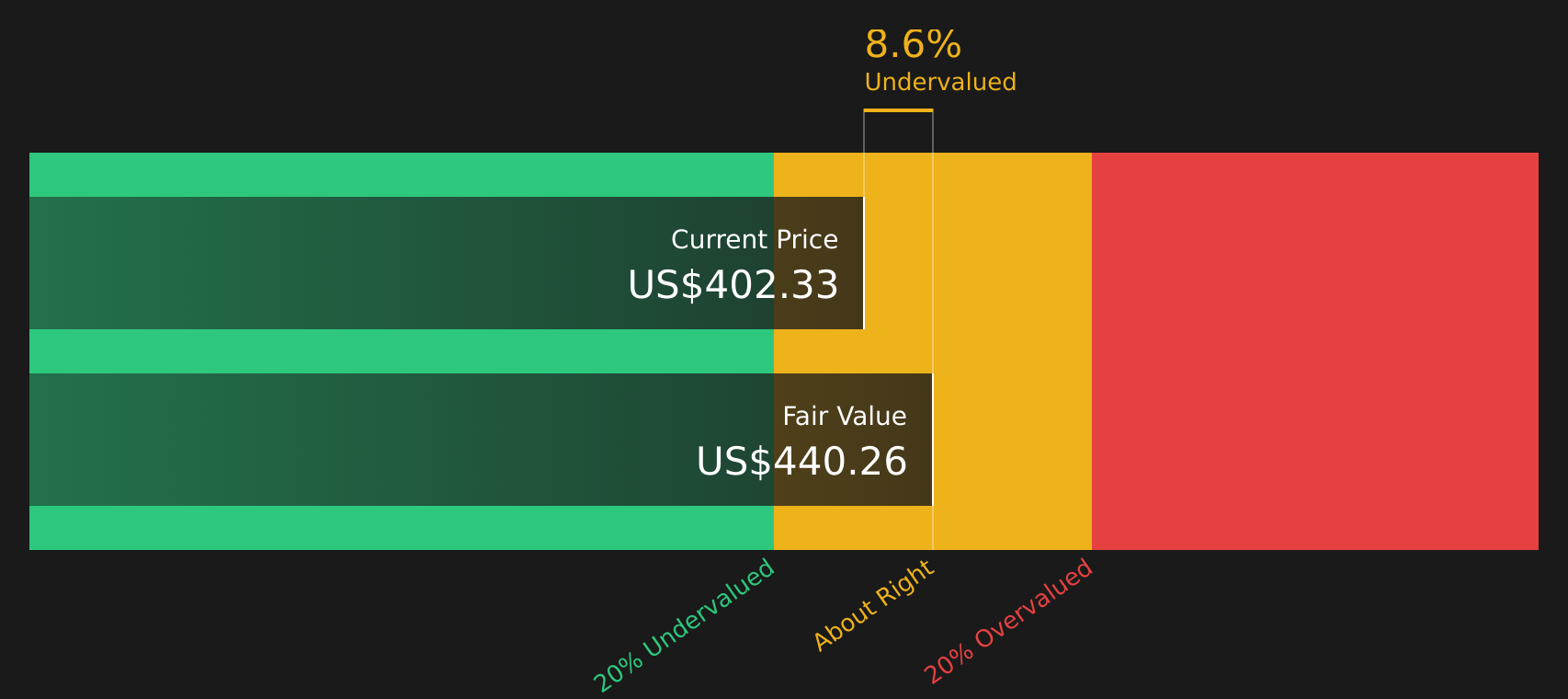

The Discounted Cash Flow (DCF) model estimates what Intuitive Surgical is worth based on the cash it is expected to generate for shareholders over time.

For Intuitive Surgical, the model starts from latest twelve month free cash flow of about $2.3b and applies a growing cash flow profile. This reflects expectations for higher future free cash generation rather than a shrinking business. On these assumptions, the DCF output points to an intrinsic value of around $441 per share, in $ terms. This is compared with a current share price that implies the stock is about 11.8% below that estimate, so it screens as undervalued on this method.

The recent recall of certain da Vinci system components helps explain why the market price may sit below the cash flow based value, as some investors factor in product risk more heavily than the DCF does.

On the Discounted Cash Flow view, Intuitive Surgical stock currently looks undervalued relative to the cash it is projected to generate.

Our Discounted Cash Flow (DCF) analysis suggests Intuitive Surgical is undervalued by 11.8%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

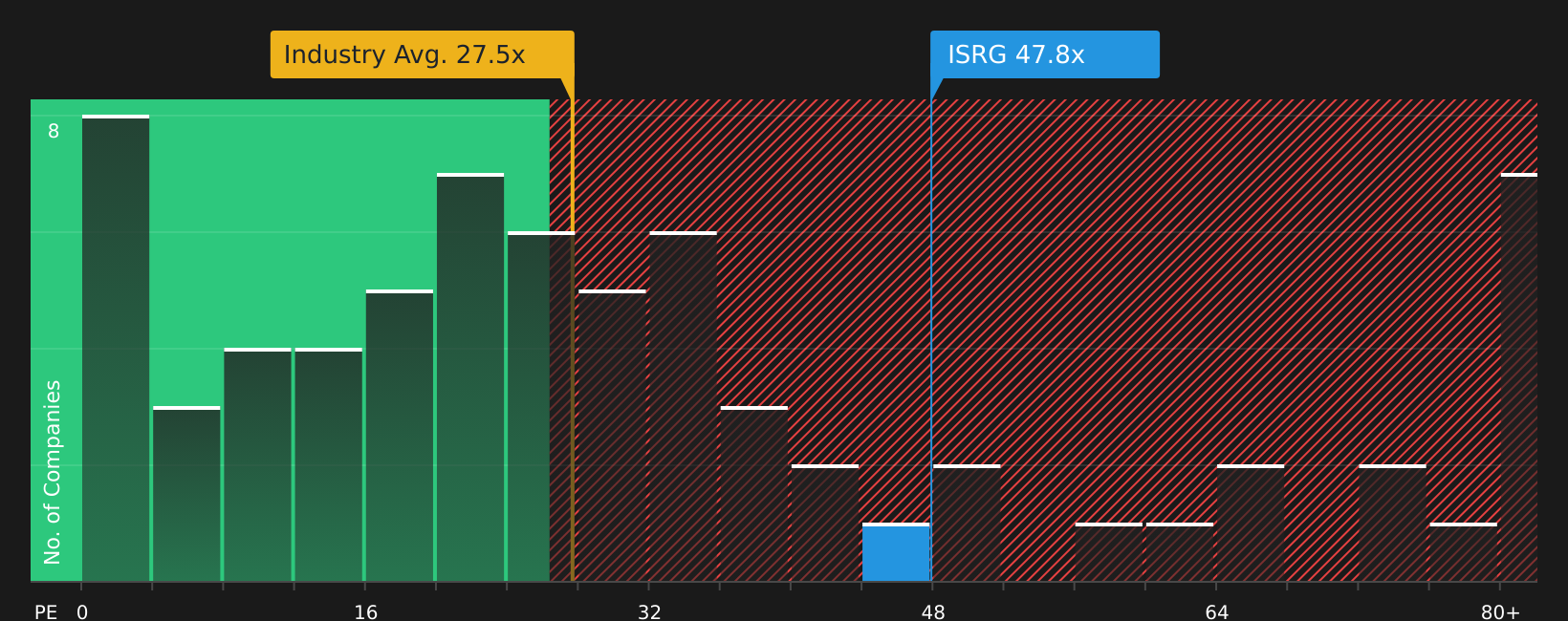

Does Intuitive Surgical Look Pricey on Earnings?

P/E is usually one of the clearest ways to compare Intuitive Surgical with other profitable medical equipment companies. On this basis, Intuitive Surgical trades at about 46.2x earnings, which is well above the broader Medical Equipment industry average of roughly 26.1x and a peer group average near 25.2x.

A P/E multiple that factors in the company’s size, margins and risk profile is estimated at around 33.8x. This still sits meaningfully below the current 46.2x level. The difference indicates that investors are paying a premium for Intuitive Surgical stock that is higher than what this framework suggests is supported by its fundamentals, even before considering recent product recall headlines.

On the P/E multiple, Intuitive Surgical stock appears overvalued relative to both tailored and industry benchmarks.

The Intuitive Surgical Narrative: What Would Justify Today's Price?

Simply Wall St Narratives continue from this valuation gap for Intuitive Surgical by explaining which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. Each narrative links a fair value to a particular view of Intuitive Surgical's potential catalysts and risks, so you can track over time which storyline appears closest to how the company is actually progressing on the Community page.

One of the top community narratives on Intuitive Surgical: 27% undervalued

"ISRG’s robust business model and strong moat come from this recurring revenue, as hospitals must continuously purchase instruments, maintenance services, and software updates to keep their da Vinci systems operational…"

Do you think there's more to the story for Intuitive Surgical? Head over to our Community to see what others are saying!

The Bottom Line

For Intuitive Surgical, the Discounted Cash Flow (DCF) intrinsic value estimate suggests the stock trades at a meaningful discount, while the earnings based multiples argue it is overvalued relative to peers. The low broader value score underlines that this is not a clean bargain and that the cash flow model and market multiples are highlighting different risks and expectations. The gap comes down to how much weight you put on long term cash generation versus what you are willing to pay today for growth, sentiment and recall related uncertainty. The key question from here is whether Intuitive Surgical can sustain growth and margins that keep justifying a premium multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.