Has Marriott (MAR) Gone Too Far After A 58% One Year Share Price Jump

Marriott International, Inc. Class A MAR | 0.00 |

- If you are wondering whether Marriott International at around US$330.93 is offering value or asking you to pay up, you are not alone. It is a question worth unpacking carefully.

- The stock has returned 1.2% over the last 7 days, 2.2% over 30 days, 5.6% year to date, 58.2% over 1 year, 108.0% over 3 years and 131.0% over 5 years, so the current price reflects a long stretch of strong share performance.

- Recent coverage has focused on Marriott International's position within the broader travel and hospitality sector and how the business model responds to shifting demand patterns between leisure and business travel. This context helps frame why investors have been willing to reprice the shares over time and why the current level attracts attention.

- Even so, Marriott International currently scores just 0 out of 6 on Simply Wall St's valuation checks for being undervalued. This sets up a closer look at traditional valuation tools like P/E and cash flow models, before finishing with a different way to think about what "fair value" really means for this stock.

Marriott International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

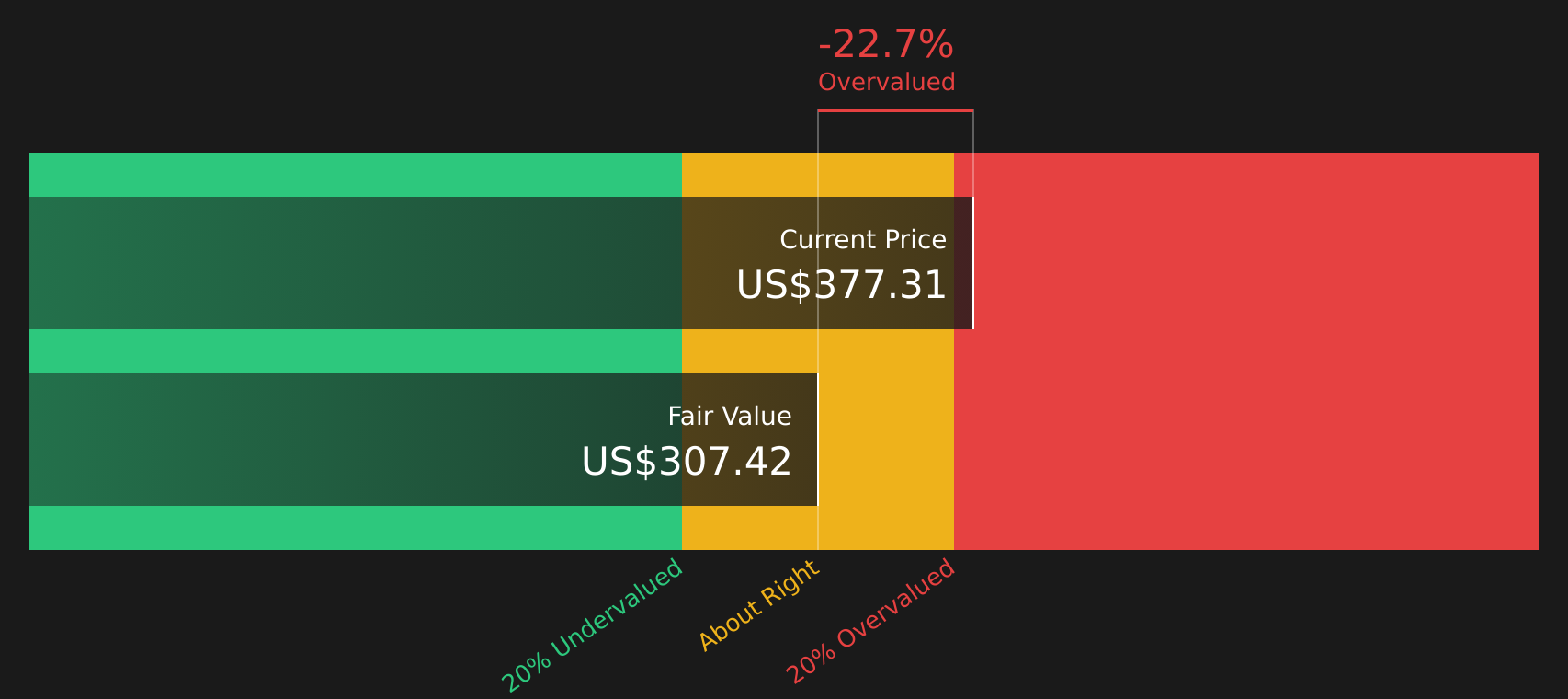

Approach 1: Marriott International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projected future cash flows, then discounts them back to today to estimate what the business might be worth right now. It focuses on cash generated for shareholders rather than accounting earnings.

For Marriott International, the latest twelve month Free Cash Flow (FCF) is about US$2.41b. The model used here is a 2 Stage Free Cash Flow to Equity approach, which combines analyst forecasts and longer term projections. Analysts supply FCF estimates out to 2028, where FCF is projected at US$3.36b, and Simply Wall St extrapolates further out to 2035 using modest year on year adjustments.

When all those projected cash flows, from 2026 through 2035, are discounted back and combined with a terminal value, the DCF model arrives at an estimated intrinsic value of about US$214.34 per share. Against a current share price around US$330.93, this implies the stock is about 54.4% above the model’s estimate of fair value, which points to a full valuation on this measure.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marriott International may be overvalued by 54.4%. Discover 61 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Marriott International Price vs Earnings

For profitable companies, the P/E ratio is a useful check on how much you are paying for each dollar of earnings. It quickly shows whether the market is attaching a richer or leaner price tag to those earnings compared with other options.

What counts as a “normal” P/E depends on how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can support a higher multiple, while slower growth or higher risk usually lines up with a lower one.

Marriott International currently trades on a P/E of 33.71x. That is higher than the Hospitality industry average of 20.90x, and also above a peer group average of 29.92x. Simply Wall St’s Fair Ratio for Marriott International is 29.33x, which is its proprietary view of what a suitable P/E could be after factoring in elements like earnings growth, profit margins, industry, market cap and specific risks.

This Fair Ratio approach goes beyond simple peer or industry comparisons, because it adjusts for the company’s own profile rather than assuming every Hospitality stock deserves the same multiple.

Compared with the Fair Ratio of 29.33x, Marriott International’s current P/E of 33.71x appears higher than that implied level.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Marriott International Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you connect your view of Marriott International’s story to concrete numbers by pairing your assumptions on future revenue, earnings and margins with a fair value, then comparing that fair value to today’s price. This all happens inside an easy tool on the Community page where different investors can, for example, treat Marriott’s asset light model, Bonvoy economics and growth options as supporting a fair value around US$269 at the cautious end or around US$415 at the optimistic end. Each Narrative updates automatically as fresh news, earnings and room pipeline data are added, so you can see in real time whether your story still justifies the price on screen.

For Marriott International however, we will make it really easy for you with previews of two leading Marriott International Narratives:

These sit on opposite sides of the debate, so you can quickly see how different assumptions on growth, profitability and valuation lead to very different fair value ranges.

Fair value: US$569.07

Implied discount to this fair value: 41.9%

Revenue growth assumption: 19.23%

- Sees Marriott as a resilient global travel platform built on an asset light model that focuses on management and franchise fees rather than owning hotel real estate.

- Emphasizes the role of the Marriott Bonvoy loyalty ecosystem and brand trust in driving recurring demand across regions and price points.

- Frames the opportunity around long term global mobility, scalable fee based cash generation and disciplined capital allocation.

Fair value: US$313.94

Implied premium to this fair value: 5.4%

Revenue growth assumption: 2.36%

- Focuses on how the asset light franchise and management model produces high margins and strong returns, but questions whether the share price already reflects these strengths.

- Highlights risks tied to macro cycles, brand quality control, technology spending and loyalty program perceptions, which could pressure future economics.

- Uses a forward valuation framework that points to a fair value close to, but below, the current share price, suggesting limited room for error.

If you want to see how other investors are connecting their stories, assumptions and fair values for Marriott, there is a wider set of community views you can reference in one place, alongside tools to build and track your own narrative over time.

Do you think there's more to the story for Marriott International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.