Has NVIDIA’s Valuation Shifted After H20 Chip Halt and China Tensions in 2025?

NVIDIA Corporation NVDA | 177.39 | +0.93% |

If you have been watching NVIDIA's stock lately and wondering whether now is the right time to buy, hold, or cash in, you are far from alone. NVIDIA's shares have been on an extraordinary ride, with the stock climbing nearly 36% over the last year and an astonishing 996% over the past three years. The company’s performance consistently tops headlines, and for good reason: its blend of innovation and market dominance in AI and semiconductors keeps investors talking.

But no story is ever perfectly smooth. In recent weeks, market sentiment has shifted as NVIDIA has grappled with new supply chain moves, including a pause in production of its H20 AI chip for China. That news, along with rising U.S.-China trade tensions and shifting regulatory postures, has injected a note of caution that is showing up in short-term price action. Despite these challenges, NVIDIA’s share price recently closed at $177.99, not far below its latest analyst price target, and the stock is still up nearly 36% so far this year. This resilience speaks to both the market’s faith in NVIDIA’s growth potential and its ability to navigate volatile regulatory waters.

Of course, high growth and headline risk always translate into fresh conversations about valuation. Is NVIDIA worth its lofty price, or does it risk getting ahead of itself? According to our valuation checklist, NVIDIA appears undervalued in just 1 out of 6 possible measures, giving it a valuation score of 1. In the following sections, I will break down how we arrive at that score, what each approach reveals, and why understanding the limits of traditional valuation models matters now more than ever.

NVIDIA delivered 37.6% returns over the last year. See how this stacks up to the rest of the Semiconductor industry.Approach 1: NVIDIA Cash Flows

The discounted cash flow (DCF) model estimates a company’s true worth by projecting its future free cash flows and discounting them back to today’s value. This process helps investors gauge whether the current stock price reflects the business’s underlying earning power.

For NVIDIA, the latest twelve months of free cash flow total about $72.1 billion. According to analyst projections, this figure is expected to nearly triple over the next decade, reaching an estimated $210.2 billion by 2030. These projections are based on strong secular growth in AI and semiconductors, driving robust free cash flow expansion year over year.

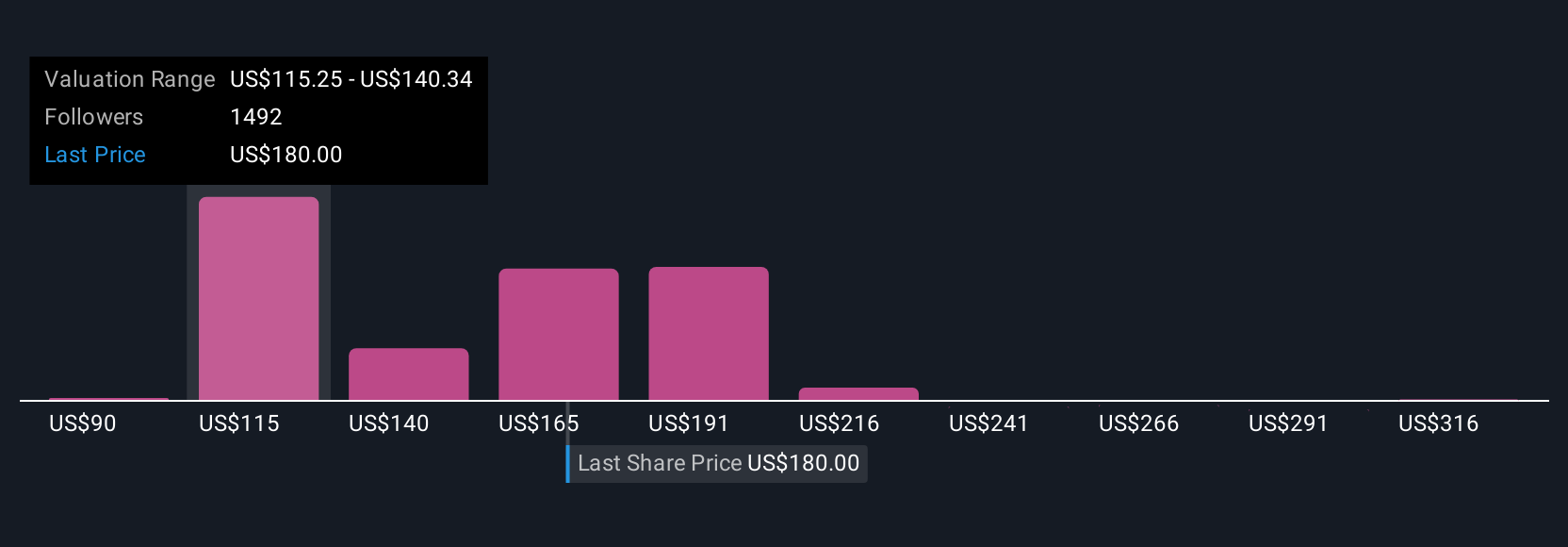

When all of these forecasts are discounted to present value, the DCF model arrives at an intrinsic fair value of $115.56 per share. With NVIDIA’s current share price at $177.99, this represents an implied discount of -54.0%. In other words, the stock is calculated to be 54.0% overvalued based on this approach.

Result: OVERVALUED

Approach 2: NVIDIA Price vs Earnings

Price-to-earnings (PE) ratio is a fundamental metric for evaluating companies like NVIDIA that generate consistent profits. It helps investors compare what the market is willing to pay today for a company’s earnings relative to its peers and industry benchmarks. For profitable, fast-growing businesses, the PE ratio is a quick way to measure whether shares are expensive or cheap based on earnings power.

Growth expectations and risk both shape what a “fair” PE ratio should look like. Fast-growing, highly profitable companies with strong leadership can often justify a PE above the industry average as investors are willing to pay up for future earnings growth. Meanwhile, heightened risk or market uncertainty tends to put downward pressure on valuations and keep the PE in check.

Currently, NVIDIA trades at a PE ratio of 56.6x. For comparison, the average PE across the semiconductor industry is 30.1x. Among peers, the group average is about 60.0x, suggesting NVIDIA is in line with direct competitors but well above the broader sector. Looking at Simply Wall St's proprietary Fair Ratio, a custom benchmark considering factors like growth, margins, and risk, NVIDIA’s fair PE is calculated at 55.4x. With the actual PE ratio just 1.2x above the Fair Ratio, the stock appears to be valued about right based on this approach.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose Your NVIDIA Narrative

Narratives are an intuitive, powerful way to make investment decisions. Think of them as your own story or perspective about NVIDIA that links what you know about the company (and where you believe it’s headed) directly to your financial forecast and an estimated fair value.

Unlike traditional models that focus solely on numbers, Narratives let you connect your outlook for NVIDIA’s revenue, earnings, and margins to its unique competitive strengths or risks. This approach encapsulates both the facts and your personal viewpoint in a transparent, actionable way.

On Simply Wall St, millions of investors use Narratives to quickly test and refine their thinking, compare scenarios, and decide when to buy or sell by seeing how their assumed Fair Value stacks up against the current market price.

The best part is that Narratives update in real time as new data, earnings, or news come in, keeping your investment thesis responsive and relevant.

For example, one investor might forecast ongoing market dominance and high switching costs, leading to a Fair Value of $316 per share. Another investor could see increased competition and margin pressure, resulting in a much lower Fair Value, such as $67.

This flexible, dynamic approach makes it easy for users of all experience levels to explore “what if” scenarios, understand different viewpoints, and craft smarter, more confident decisions about NVIDIA’s future.

For NVIDIA, here are previews of two leading NVIDIA Narratives: 🐂 NVIDIA Bull Case Fair Value: $341.12 Undervalued by: -47.8% Forecast Revenue Growth: 25.46% - NVIDIA is positioned as a leader in AI and data centers, supported by strong innovation, a robust ecosystem, and financial resilience. - Growth catalysts include rapid AI adoption, expansion into automotive and edge computing, and the launch of advanced GPU platforms. - Risks include a high current valuation, dependence on the Chinese market amid geopolitical tensions, and increasing competition from both established and emerging chipmakers. 🐻 NVIDIA Bear Case Fair Value: $141.74 Overvalued by: 25.6% Forecast Revenue Growth: 17.2% - NVIDIA’s dominance in data centers and AI is driving strong sales, but potential competition in hardware and the GPU market could pressure margins and growth. - Challenges may arise from increasing energy demands due to generative AI workloads, regulatory obstacles for acquisitions, and possible supply chain disruptions. - While gaming and automotive remain promising, factors such as slowing growth rates, pricing strategies, and strong competition from AMD and Intel could limit future potential. Do you think there's more to the story for NVIDIA? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.