Has The Recent Pullback In Costco Wholesale (COST) Opened A Better Entry On Rich Valuation?

Costco Wholesale COST | 0.00 |

- Wondering if Costco Wholesale at around US$956 per share is still a solid long term hold or starting to look stretched on price? This article breaks down what the current tag might really mean for you.

- The stock is down about 7% over the last week and 4.2% over the last month, yet it is still up 11.9% year to date and has delivered gains of 94.2% over 3 years and 160.5% over 5 years.

- Recent headlines have focused on Costco Wholesale's role as a key US consumer retailer, with attention on how membership based warehouse clubs are positioned as shopping habits evolve. This context helps explain why the stock can experience short term pullbacks even after strong multi year returns.

- Despite that track record, Costco Wholesale currently scores 0 out of 6 on our valuation checks. Next you will see how traditional valuation tools stack up for this stock and why there may be an even better way to think about value by the end of the article.

Costco Wholesale scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

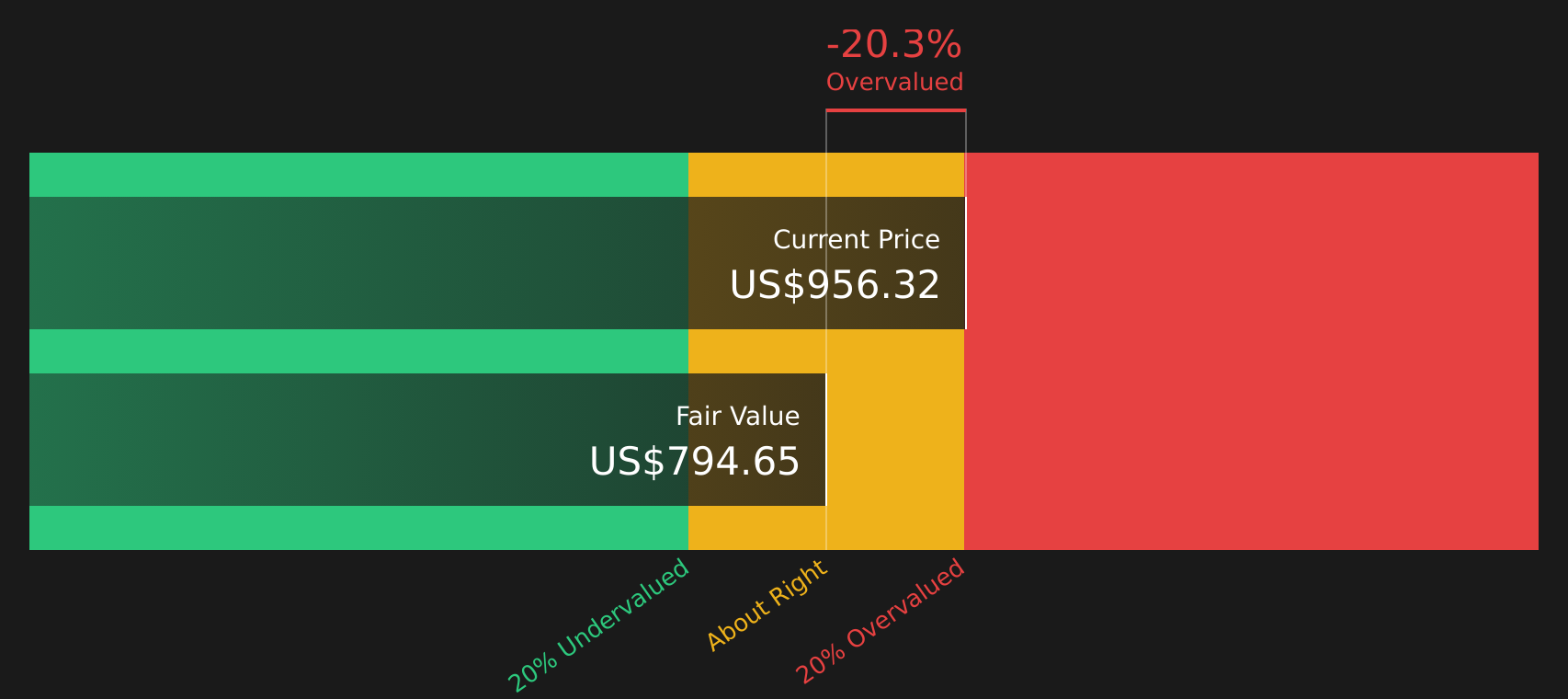

Approach 1: Costco Wholesale Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock might be worth by projecting future cash flows and then discounting them back to today, using a required rate of return.

For Costco Wholesale, the model uses last twelve months Free Cash Flow of about $9.50b and a 2 Stage Free Cash Flow to Equity approach. Analyst estimates cover several years, and Simply Wall St then extrapolates those forecasts further out, with projected Free Cash Flow reaching about $18.09b in 2035 based on the supplied projections.

Bringing all those projected cash flows back to today gives an estimated intrinsic value of about $792.68 per share. Compared with the current share price of around $956, the DCF output suggests the stock is about 20.6% above this intrinsic estimate, which points to Costco Wholesale trading on the expensive side using this model alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Costco Wholesale may be overvalued by 20.6%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Costco Wholesale Price vs Earnings

For a profitable company like Costco Wholesale, the P/E ratio is a useful yardstick because it ties the share price directly to the earnings that support it. The level of P/E investors are usually comfortable with tends to reflect what they expect for future growth and how much risk they see in those earnings.

Costco Wholesale currently trades on a P/E of about 49.6x. That is higher than the Consumer Retailing industry average of roughly 18.5x and also above the peer group average of about 22.8x, so on simple comparisons the stock sits at a premium. To go a step further, Simply Wall St’s Fair Ratio for Costco Wholesale is 41.0x. This Fair Ratio is a proprietary estimate of what the P/E might be given factors such as the company’s earnings growth profile, its industry, profit margins, market cap and risk characteristics.

Because the Fair Ratio folds in these company specific factors, it can be more informative than just lining up Costco Wholesale against broad industry or peer averages. With the current P/E of 49.6x sitting above the Fair Ratio of 41.0x, the multiple points to the stock looking expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Costco Wholesale Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives on Simply Wall St give you a simple way to attach your story about Costco Wholesale to the numbers by linking your view of its membership strength, margins, revenue growth and fair value to a financial forecast, then comparing that Fair Value with today’s price. Each Narrative lives on the Community page and updates automatically when fresh news or earnings arrive. You can see, for example, how one Costco Wholesale Narrative with a Fair Value near US$489 and another closer to US$1,529 reflect very different expectations about future margins, growth and P/E multiples, yet both use the same underlying framework to help you decide whether the current price feels high, low or about right for your own thesis.

For Costco Wholesale, we will make it really easy for you with previews of two leading Costco Wholesale Narratives:

These give you two clearly framed viewpoints around the same stock, so you can see which assumptions feel closer to your own.

Fair value in this narrative: about US$1,047.90 per share.

Price gap to this fair value: the stock is about 8.7% below this estimate on the latest close of US$956.32.

Revenue growth input: 7.52% a year.

- Focuses on continued warehouse expansion, longer gas station hours and strong e commerce growth as drivers of higher membership, traffic and sales.

- Highlights international roll out and Executive Membership growth as ways to broaden earnings, while also flagging risks from labor costs, tariffs, supply chains and foreign exchange.

- Frames analyst targets around US$1,072.67 as broadly aligned with current pricing. Encourages you to stress test the revenue, margin and P/E assumptions against your own view of Costco Wholesale.

Fair value in this narrative: about US$726.29 per share.

Price gap to this fair value: the stock is about 31.7% above this estimate on the latest close of US$956.32.

Revenue growth input: 7.0% a year.

- Emphasizes Costco Wholesale as a high quality, wide moat business, but argues the stock is priced for perfection with a high P/E that could limit long term returns if the multiple falls.

- Lays out bull, base and bear scenarios to 2031 where strong operations meet possible valuation compression, tariffs on key product categories and rising competition, including from Sam's Club.

- Summarizes the stance as holding Costco Wholesale while being price sensitive, with more attractive long term return potential if the share price pulls back closer to the analyst's base case targets.

Do you think there's more to the story for Costco Wholesale? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.