Has The Strong 1 Year Rally Left KeyCorp (KEY) Fully Priced Or Still Attractive?

KeyCorp KEY | 0.00 |

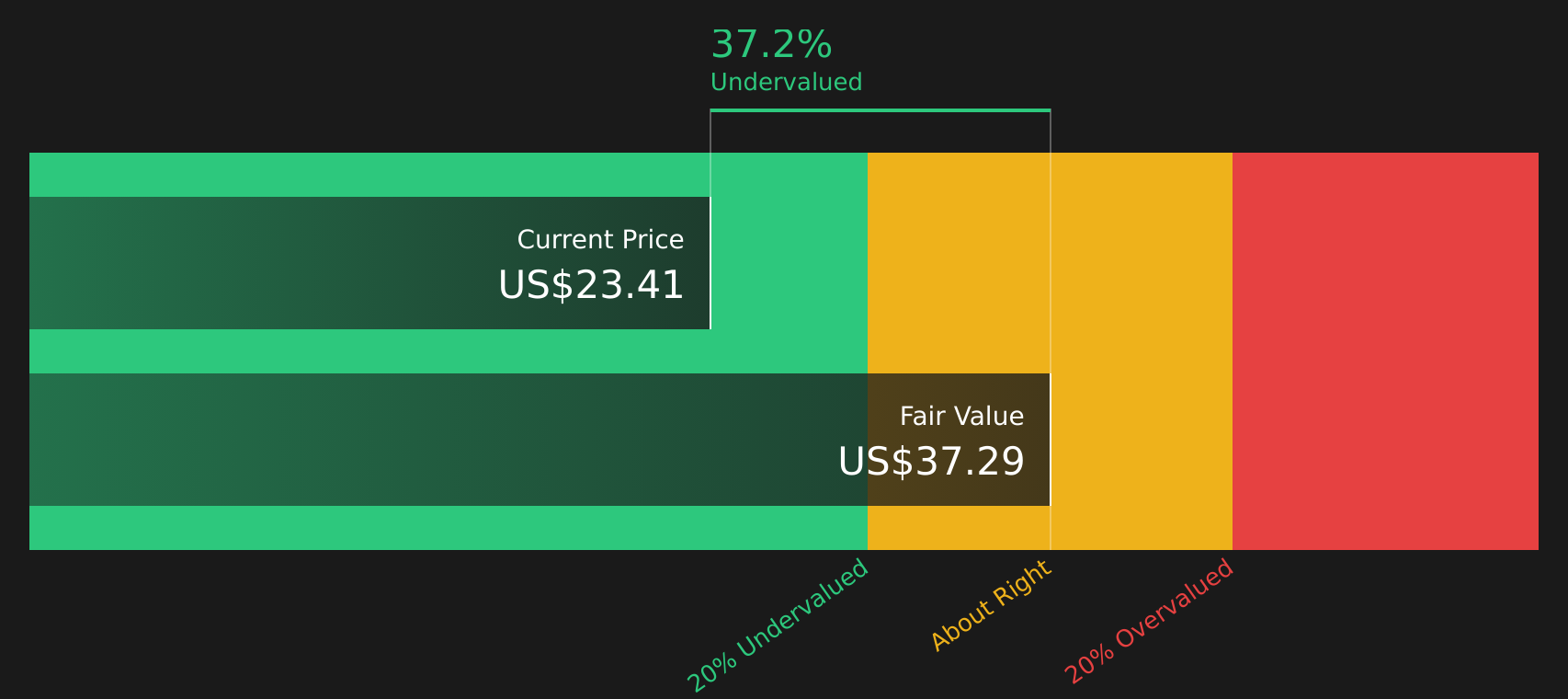

- Wondering if KeyCorp's share price still reflects good value after a strong run, or if most of the easy gains are behind it? This article walks through what the current valuation actually says.

- KeyCorp shares last closed at US$21.76, with the stock up 2.0% over the past week, slightly down 2.1% over the past month, up 3.7% year to date, and up 38.9% over the past year, while the 3 year and 5 year returns stand at 137.8% and 26.4% respectively.

- Recent price moves sit against a backdrop of ongoing sector wide attention on US regional banks, including how they manage deposits, interest rate exposure, and credit quality. For KeyCorp, headlines around capital strength, funding mix, and regulatory scrutiny give useful context for judging whether the current share price still lines up with the fundamentals.

- On Simply Wall St's valuation checks, KeyCorp scores a 4 out of 6. The rest of this article will walk through the different valuation methods behind that score, before finishing with a broader way to think about what the stock might be worth in your portfolio.

Approach 1: KeyCorp Excess Returns Analysis

The Excess Returns model looks at how much profit a company is expected to earn over and above the return that shareholders require, then adds the value of those excess profits to the underlying book value of the equity.

For KeyCorp, the starting point is an estimated Book Value of $16.08 per share and a Stable EPS of $2.05 per share, based on weighted future Return on Equity estimates from 9 analysts. The model applies an Average Return on Equity of 11.97% to a Stable Book Value of $17.09 per share, from weighted future Book Value estimates from 10 analysts.

The Cost of Equity is put at $1.26 per share, which leads to an estimated Excess Return of $0.79 per share. By capitalising these expected excess returns and combining them with the stable book value, the model arrives at an intrinsic value of about $37.57 per share.

Compared with the recent share price of $21.76, this indicates the stock is 42.1% undervalued according to this approach.

Result: UNDERVALUED

Our Excess Returns analysis suggests KeyCorp is undervalued by 42.1%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: KeyCorp Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of current earnings. This makes it a practical cross check against more complex models like discounted cash flows.

What counts as a "normal" P/E depends on how the market views a company’s growth prospects and risk, with higher expected growth or lower perceived risk often supporting a higher multiple, while slower growth or higher risk can justify a lower one.

KeyCorp currently trades on a P/E of 13.09x. That sits above the Banks industry average of 11.62x, but below the peer group average of 14.56x. Simply Wall St’s Fair Ratio for KeyCorp is 13.63x, which is a proprietary estimate of what the P/E might be given its earnings growth profile, industry, profit margins, market cap and risk factors.

This Fair Ratio offers a more tailored reference point than a simple comparison with peers or the wider industry. It adjusts for company specific fundamentals rather than assuming all banks should trade on the same multiple.

The current P/E of 13.09x is slightly below the Fair Ratio of 13.63x, which indicates that the stock may be modestly undervalued on this measure.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your KeyCorp Narrative

Earlier the article mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St give you a simple story for KeyCorp that links your view of its future revenue, earnings and margins to a financial forecast, a fair value, and a clear comparison with today’s price. Different investors in the Community page can set very different narratives, such as a bullish one that lines up with fair value near the upper analyst target of US$43.0 or a more cautious one closer to US$18.0. Those narratives then update automatically as new news or earnings arrive to help you decide if the stock still fits your thesis.

For KeyCorp, however, we will make it really easy for you with previews of two leading KeyCorp Narratives:

Narrative fair value: US$25.03 per share

Implied pricing gap vs last close (US$21.76): about 13.1% below this narrative fair value

Analyst revenue growth assumption: 9.02% a year

- Analysts build a case around a shift in net interest income from headwind to tailwind, supported by how KeyCorp prices loans, manages swaps and handles deposit costs.

- Noninterest income, from areas such as wealth management, commercial payments and commercial loan servicing, is used to frame a more diversified and potentially steadier earnings mix.

- The consensus price target of US$25.03 sits within a wide analyst range. The thesis therefore depends on your comfort with assumptions about revenue of US$9.3b, earnings of US$2.5b and a P/E of 13.1x by 2029.

Narrative fair value: US$18.00 per share

Implied pricing gap vs last close (US$21.76): about 20.9% above this narrative fair value

Bear cohort revenue growth assumption: 16.37% a year

- This narrative focuses on KeyCorp’s reliance on commercial borrowers, fee heavy businesses and assumed margin gains, and questions how resilient those are if loan demand or capital markets activity soften.

- It highlights the risk that higher ongoing spending and any change in credit quality or regulation could limit capital returns and pressure earnings, even if headline growth numbers look solid.

- The implied fair value of US$18.00 reflects analysts who expect the stock to trade on a lower P/E multiple of 8.8x by 2028, even though they use relatively robust revenue and earnings forecasts.

Put simply, one narrative views today’s price as sitting below a fair value built on improving loan economics and capital return. The other treats the same stock price as rich compared with more cautious assumptions for margins, credit risk and future multiples. Your own view on which set of assumptions feels more realistic will drive how KeyCorp fits into your portfolio and risk tolerance.

Do you think there's more to the story for KeyCorp? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.