Has Visa (V) Weak Share Price Created A Fresh Opening For Long Term Investors?

Visa V | 0.00 |

- If you are wondering whether Visa's share price still reflects its long term growth story or if the stock has moved ahead of its fundamentals, a closer look at its valuation can help you frame that question more clearly.

- Visa's shares last closed at US$329.24, with returns of 0.2% decline over 7 days, 4.1% decline over 30 days, 5.0% decline year to date and 5.6% decline over 1 year, while the 3 year and 5 year returns sit at 47.1% and 64.6% respectively.

- Recent coverage of Visa has focused on its role at the centre of global digital payments and the way investors think about its long term transaction volumes and competitive position. This context helps explain why, even with some short term share price softness, many market participants continue to treat Visa as a core payments infrastructure holding.

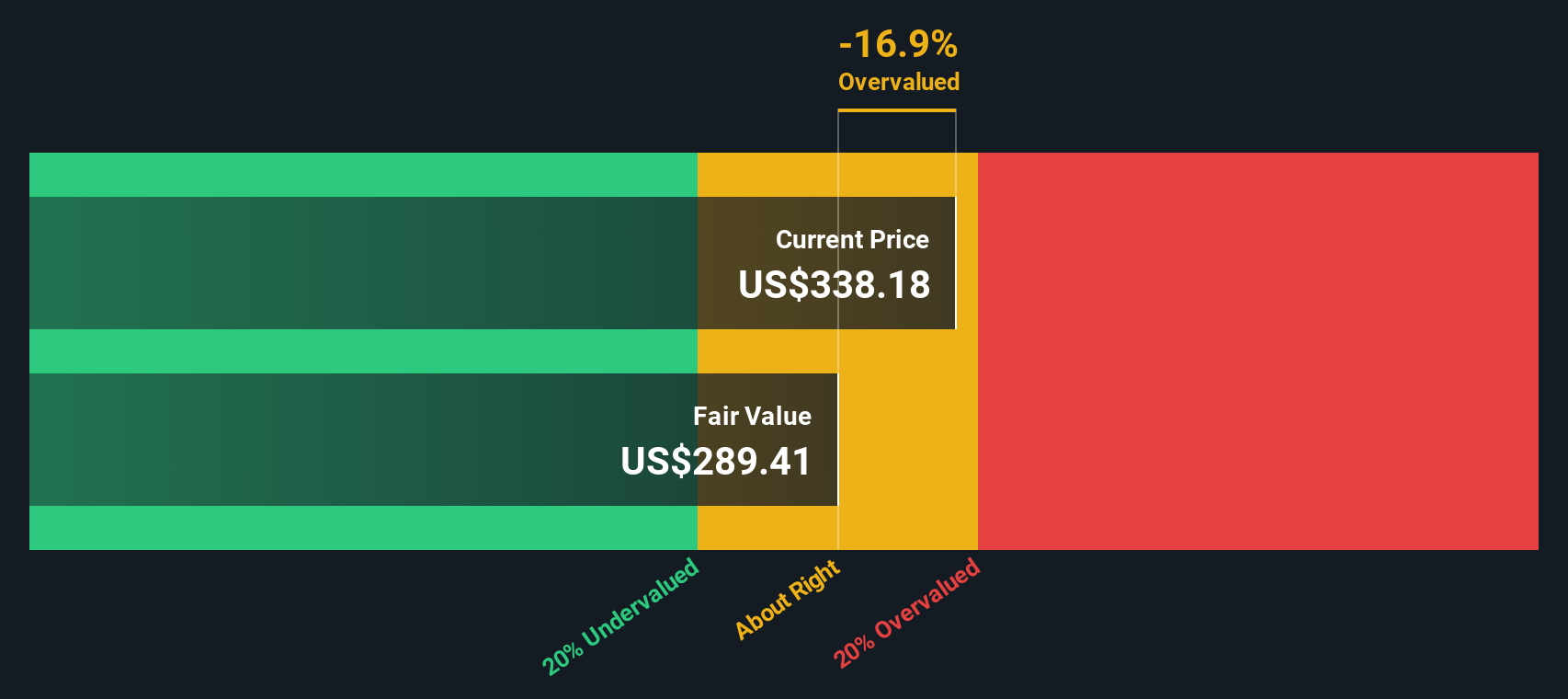

- Simply Wall St currently gives Visa a valuation score of 3 out of 6. In the next sections we will walk through the main valuation approaches behind that number, and then circle back at the end to a more holistic way to think about what the stock might be worth to you.

Approach 1: Visa Excess Returns Analysis

The Excess Returns model looks at how much profit a company can earn above the return that shareholders are assumed to require, then capitalizes those extra profits into an estimated per share value.

For Visa, the model starts with a Book Value of US$20.03 per share and a Stable EPS of US$17.07 per share, based on weighted future Return on Equity estimates from 12 analysts. The implied Cost of Equity is US$1.78 per share, so the Excess Return comes out at US$15.29 per share. That is supported by an Average Return on Equity of 69.87%, which is applied to a Stable Book Value of US$24.44 per share, based on estimates from 8 analysts.

Putting this together, Simply Wall St’s Excess Returns framework points to an intrinsic value of about US$417.91 per share. Compared with the recent share price of US$329.24, this suggests the stock is around 21.2% undervalued on this model.

Result: UNDERVALUED

Our Excess Returns analysis suggests Visa is undervalued by 21.2%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: Visa Price vs Earnings

For profitable companies like Visa, the P/E ratio is a useful shorthand for how much investors are paying for each dollar of earnings. This makes it a practical tool when earnings are positive and relatively stable.

What counts as a "fair" P/E usually reflects two big ideas: how quickly earnings are expected to grow, and how risky those earnings are. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to pull a "normal" P/E lower.

Visa currently trades on a P/E of 30.47x. That is well above the Diversified Financial industry average P/E of 15.34x and also above the peer group average of 14.77x. To refine that comparison, Simply Wall St uses a proprietary Fair Ratio metric, which estimates what P/E might make sense for Visa based on factors such as its earnings growth profile, profit margins, industry, market capitalization and risk characteristics. Because this Fair Ratio of 20.82x is tailored to Visa, it can be more informative than a simple industry or peer comparison.

Comparing Visa's current P/E of 30.47x to the Fair Ratio of 20.82x suggests the shares are pricing in richer expectations than this framework would imply.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 22 top founder-led companies.

Upgrade Your Decision Making: Choose your Visa Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives. These are simple stories you build around Visa that connect your view of its business to a set of revenue, earnings and margin estimates. Those estimates then roll into a Fair Value you can compare with today’s share price on the Simply Wall St Community page, where millions of investors already share and refine these stories in real time as new news or earnings land. You can quickly see, for example, how one Visa Narrative with a Fair Value of about US$463.49 and another at about US$243.09 reflect very different views on things like regulation, stablecoins and B2B growth, and decide for yourself whether the current price looks high, low or roughly in line with the story you find most convincing.

For Visa however we will make it really easy for you with previews of two leading Visa Narratives:

Together they show how investors can look at the same business and reach very different conclusions about what the current share price might be pricing in.

Fair value: US$397.72 per share

Implied discount to this fair value: approximately 17.2% below the narrative fair value, based on the recent price of US$329.24

Forecast revenue growth in the narrative: 10.6% a year

- Focuses on growing digital adoption, e commerce and emerging markets as key drivers of payment volumes and long term revenue.

- Highlights rapid take up of higher margin value added services, cross border solutions and stablecoin settlement as ways to broaden revenue and support margins.

- Frames strong free cash flow and buybacks as support for earnings per share and as a cushion if the current price sits below this narrative’s fair value range.

Fair value: US$284.00 per share

Implied premium to this fair value: approximately 15.9% above the narrative fair value, based on the recent price of US$329.24

Forecast revenue growth in the narrative: 11.5% a year

- Sees Visa as a high quality business but questions how much of the long term growth story is already reflected in the current share price.

- Assumes legacy growth drivers such as cash displacement and consumer spending contribute less over time, with inflation and new initiatives like Visa Direct doing more of the work.

- Flags regulatory risk, local payment networks and fintech or crypto competition as reasons to be careful about the multiple investors are willing to pay.

Both narratives are based on detailed revenue, margin and P/E assumptions, yet they arrive at very different fair values. Your task as an investor is to decide which story feels closer to how you see Visa’s future, or whether your own view sits somewhere in between.

Once you have that, you can treat the current share price as just one input alongside your preferred narrative rather than a verdict on what Visa is worth.

Do you think there's more to the story for Visa? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.