Hayward Holdings (HAYW) Valuation Under Scrutiny As Growth Slows And Profitability Weakens

Hayward Holdings, Inc. HAYW | 13.38 | -0.82% |

Slowing fundamentals come into focus for Hayward Holdings (HAYW)

Recent analysis of Hayward Holdings (HAYW) is drawing attention to slowing organic revenue growth, weaker earnings per share, and a declining return on invested capital, factors that together may be affecting how investors view the stock.

Despite the weaker fundamentals, the share price has held up reasonably well, with a 30 day share price return of 3.45% and a 90 day share price return of 7.57%. This has contributed to a 1 year total shareholder return of 8.34%, which hints at gradually building momentum.

If Hayward’s recent moves have you reassessing the pool equipment space, it could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

With revenue of about US$1.10b, net income of roughly US$137.9m and a share price close to US$16.49, Hayward screens as a value stock using this model. The key question is whether that represents a genuine opportunity or whether the market is already pricing in any future growth.

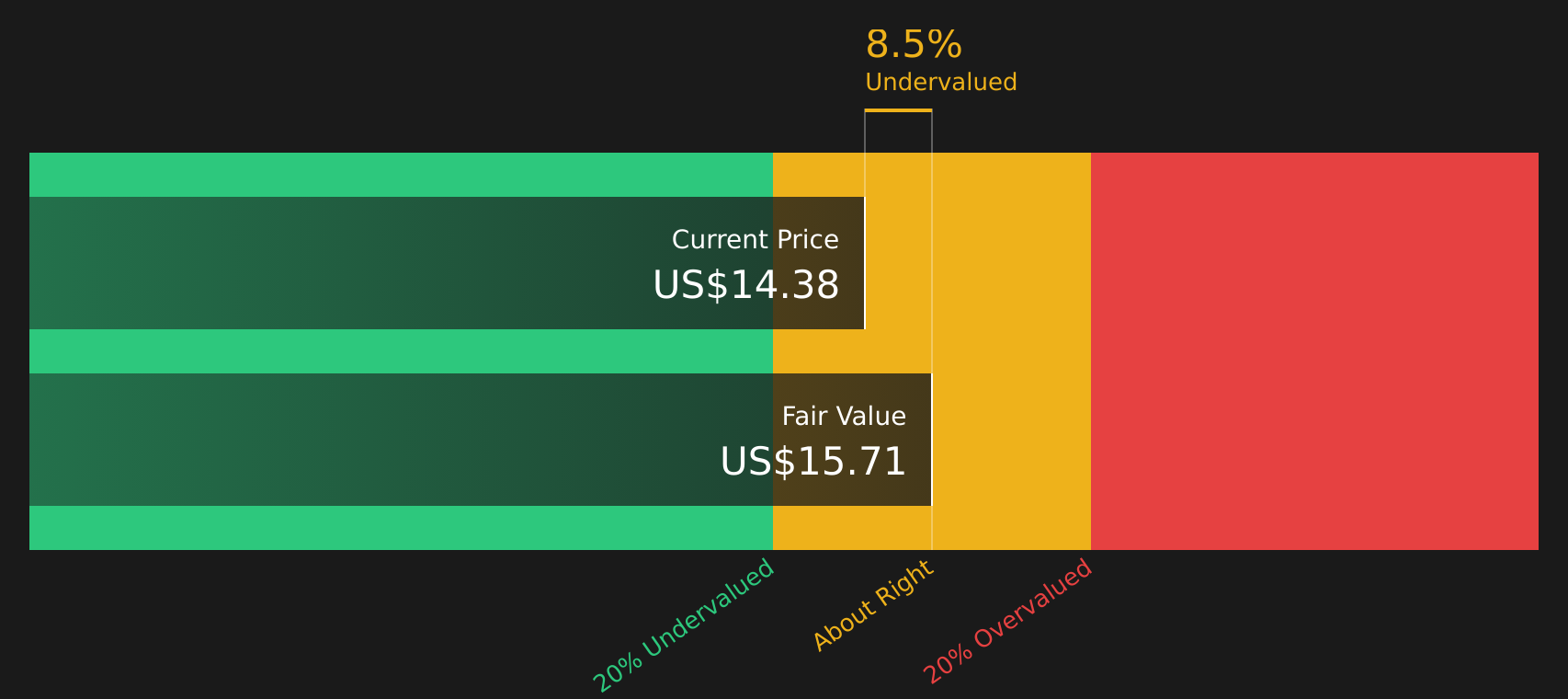

Most Popular Narrative: 7.7% Undervalued

With Hayward Holdings last closing at $16.49 against a widely followed fair value estimate of about $17.86, the current narrative sees modest upside grounded in detailed revenue, margin, and valuation assumptions.

Rising demand for energy-efficient and eco-friendly pool products, combined with an aging installed pool base in the US and Europe that requires modernization, creates a durable replacement cycle, supporting consistent aftermarket revenue and higher gross margins as product mix shifts to newer, premium solutions.

Curious what kind of revenue runway and margin profile are baked into that fair value, and how rich a future earnings multiple this narrative assumes? The full story connects moderate growth, firmer profitability, and a valuation level that still leans on confidence in Hayward’s aftermarket strength.

Result: Fair Value of $17.86 (UNDERVALUED)

However, there are clear pressure points here, including reliance on a mature residential aftermarket and the risk that repair-over-replacement habits cap both revenue and margins.

Another View: Cash Flows Paint A Tougher Picture

While the fair value narrative points to Hayward Holdings being about 7.7% undervalued at $17.86, the SWS DCF model tells a different story. On that measure, the shares at $16.49 sit well above an estimated cash flow value of $10.93, which screens as overvalued.

That gap suggests the current price leans more on confidence and sentiment than on conservative cash flow assumptions. This raises a simple question for you: are you comfortable paying a premium to those modeled cash returns, or would you rather wait for expectations to cool?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hayward Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 867 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hayward Holdings Narrative

If you see the numbers differently or prefer to rely on your own work, you can build a custom Hayward view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Hayward Holdings.

Looking for more investment ideas?

If Hayward has sharpened your thinking, do not stop here. Broaden your opportunity set with focused screeners that surface stocks matching very different return profiles.

- Spot early stage names that still clear basic quality hurdles by checking out these 3520 penny stocks with strong financials before they appear on everyone else’s radar.

- Ride the automation and machine learning wave by scanning these 23 AI penny stocks for companies tied to data processing, model training, and deployment tools.

- Zero in on cash flow backed ideas by filtering for these 867 undervalued stocks based on cash flows, where modeled intrinsic values sit above current market prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.