Helix Energy Solutions (HLX) Stock Valuation After Sector Gains On Rising Middle East Geopolitical Tensions

Helix Energy Solutions Group, Inc. HLX | 0.00 |

Helix Energy Solutions Group (HLX) moved higher after a 5.2% gain that tracked a broader lift in energy stocks, as investors reacted to the recent escalation in conflict between Israel and Iran.

Beyond the latest move, Helix’s recent trading has been shaped by both company specific news, including its planned merger with Hornbeck Offshore and a revenue result that differed from EBITDA expectations, as well as shifting geopolitical risk in energy markets. At a share price of US$9.77, the stock shows a strong year to date share price return of 52.66% alongside a 1 year total shareholder return of 38.19%. This points to momentum that has cooled slightly over the past month but remains positive over the medium term.

If heightened energy market tensions have your attention, it can be useful to see what else is moving in related areas of the market using our 34 power grid technology and infrastructure stocks

With Helix trading at US$9.77 alongside a reported intrinsic discount of 35.78% and a 27.94% gap to the price target, you have to ask: is this a genuine mispricing, or is the market already baking in future growth?

Most Popular Narrative: 20% Overvalued

At a last close of $9.77 versus a widely followed fair value estimate of $9.75, the current price sits slightly above that narrative anchor while still reflecting a sizeable modelled discount to future cash flows.

The analysts have a consensus price target of $10.125 for Helix Energy Solutions Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $11.0, and the most bearish reporting a price target of just $9.0.

Curious what earnings path and margin profile sit behind that fair value and price target spread? The narrative leans on steady revenue expansion, a higher profitability mix, and a future earnings multiple that assumes investors keep assigning a premium to this offshore services business.

Result: Fair Value of $9.75 (OVERVALUED)

However, the story can change quickly if contract awards are pushed out again or if spot market exposure leaves key vessels sitting underutilized.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

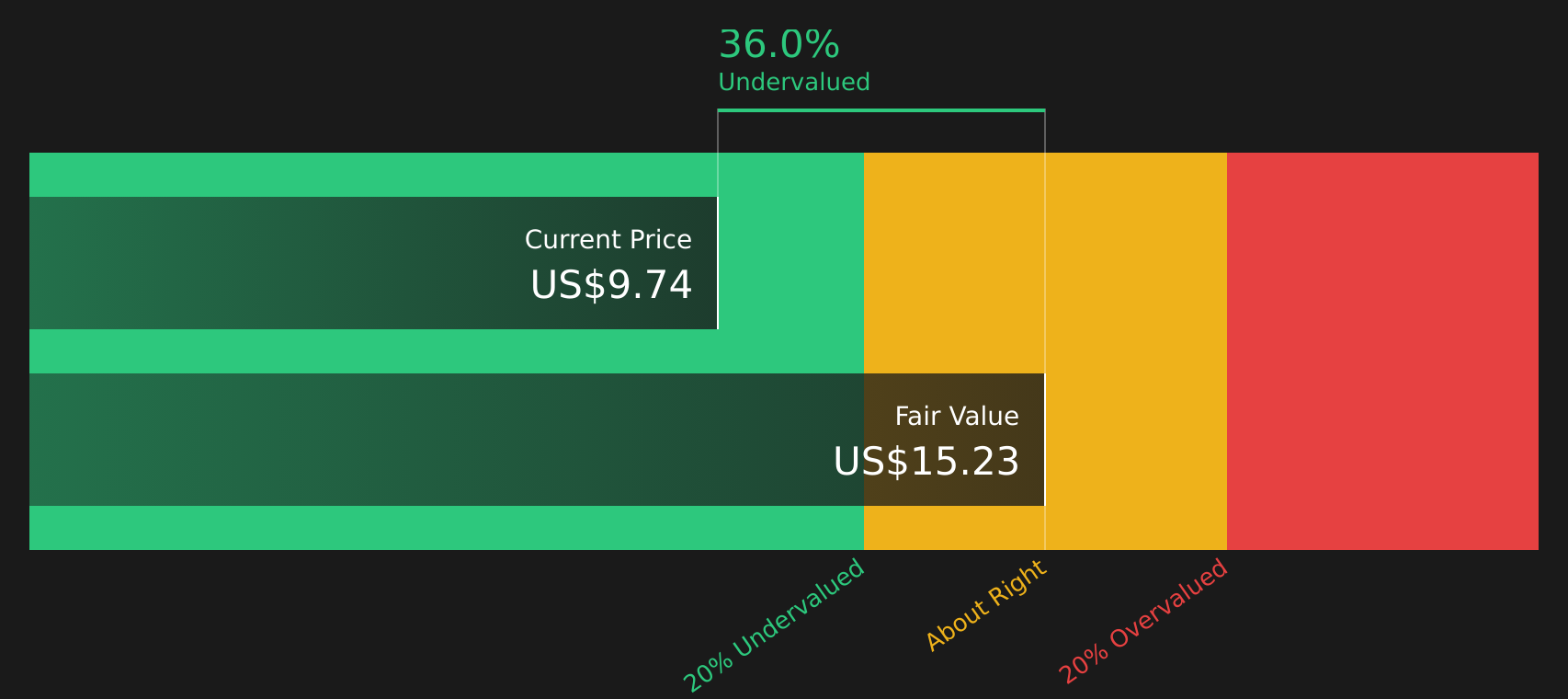

Another View: Cash Flows Tell a Different Story

While the popular narrative tags Helix as about 20% overvalued around a fair value of $9.75, the SWS DCF model presents a different picture. On that cash flow view, Helix at $9.77 screens as undervalued versus an estimated future cash flow value of $15.21. This raises the question of which lens may be more useful for long-term analysis.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Helix Energy Solutions Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals in this article, it makes sense to move quickly and check the underlying numbers yourself so you are not leaning on a single viewpoint. To weigh both the concerns and the potential upside, take a closer look at the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing out on other opportunities that better match your goals, risk tolerance and income needs.

- Spot potential value opportunities early by scanning 46 high quality undervalued stocks that pair solid fundamentals with pricing that may not fully reflect their underlying business strength.

- Secure potential income ideas by reviewing 8 dividend fortresses that focus on higher yielding companies with room for investors to assess the sustainability of those payouts.

- Sleep a little easier at night by checking 67 resilient stocks with low risk scores where financial strength and lower risk scores take center stage for capital preservation minded investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.