Herbalife (HLF) Valuation Check After Sharp 3 Month Share Price Rebound

Herbalife Nutrition Ltd. HLF | 13.89 | -3.47% |

Herbalife stock moves catch investor attention

Recent trading in Herbalife (HLF) has drawn attention after a sharp share price move over the past 3 months. This has prompted investors to reassess the company’s fundamentals and valuation signals.

With a recent close of US$16.64 and an intrinsic discount estimate of 32%, some investors are comparing this to Herbalife’s reported revenue of US$4.96b and net income of US$320.8m to gauge how the current pricing lines up with fundamentals.

That recent 99.5% 3 month share price return and 17.4% 1 month share price return sit alongside a 157.98% 1 year total shareholder return, even though the 5 year total shareholder return remains 67.35% lower.

If Herbalife’s swing in sentiment has you thinking about what else might be moving, it could be worth scanning fast growing stocks with high insider ownership as a next step.

So with Herbalife trading at US$16.64 alongside an estimated 32% intrinsic discount and a mixed track record of shareholder returns, is this a genuine mispricing, or is the market already baking in future growth?

Most Popular Narrative: 18.9% Overvalued

Herbalife’s most followed valuation narrative pegs fair value at about $14, below the last close of $16.64, which sets a cautious tone around pricing.

The analyst price target on Herbalife in our model has moved from US$12 to US$14, as analysts point to a recovery path supported by a healthier profit margin outlook, a slightly lower discount rate, and recent research highlighting ongoing business model improvements despite tempered revenue growth expectations and cautious sector valuations.

Curious what kind of margin rebuild and future earnings multiple need to work together to reach that number? The full narrative spells out the revenue path, profit profile, and valuation math in detail.

Result: Fair Value of $14 (OVERVALUED)

However, if Herbalife’s push into personalized wellness products and tech platforms gains more traction, or if North America volume growth broadens, this cautious valuation story could shift.

Another Angle: Earnings-Based Multiples Paint A Different Picture

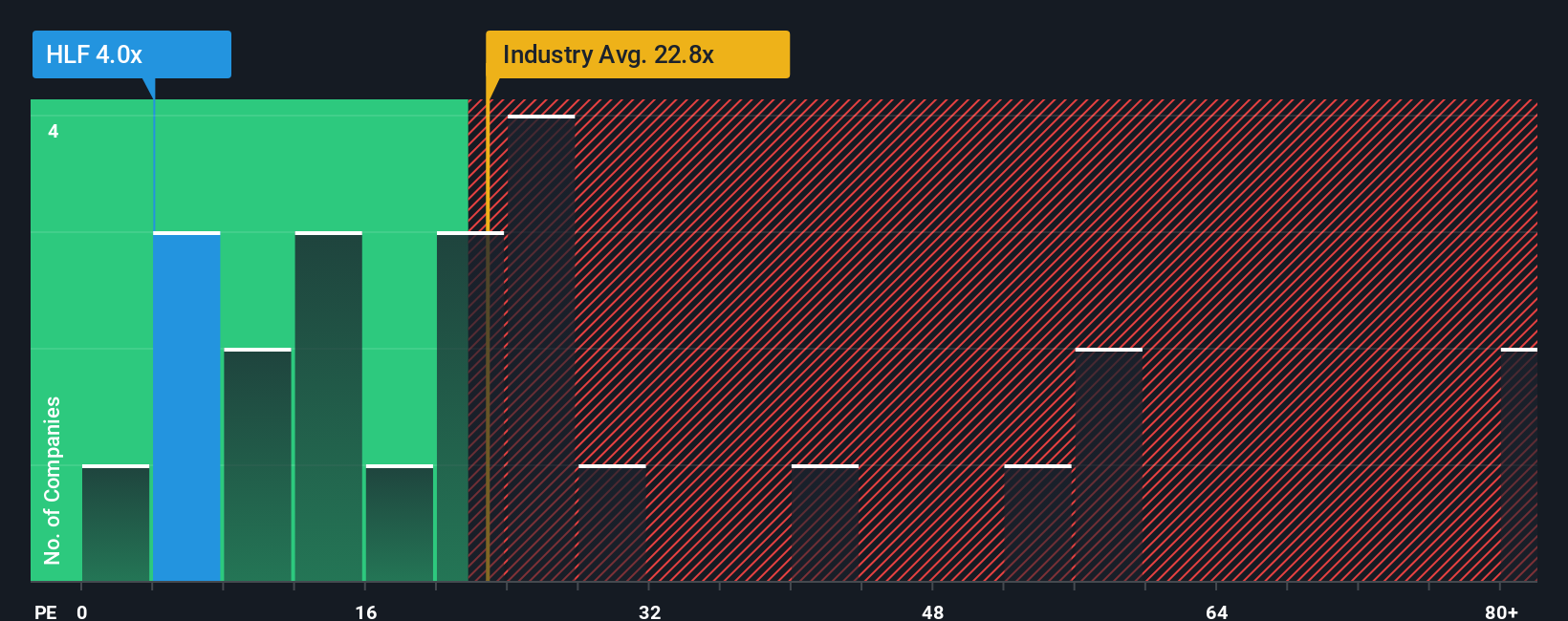

While the most popular narrative sees Herbalife as about 18.9% overvalued at $16.64 versus a fair value of $14, the earnings-based view looks very different. Herbalife trades on a P/E of 5.4x, compared with an estimated fair ratio of 12.1x, peers at 22.2x and the North American Personal Products industry at 22.9x.

That kind of gap suggests the market is pricing in a lot of risk already, even with earnings expected to decline by an average of 0.8% per year over the next 3 years. The real question is whether you think current concerns already more than cover those headwinds.

Build Your Own Herbalife Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can reshape the story in just a few minutes with Do it your way.

A great starting point for your Herbalife research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Herbalife has sharpened your thinking, do not stop there. Your next strong idea could be sitting in the screener waiting to be noticed today.

- Spot potential value opportunities early by scanning these 864 undervalued stocks based on cash flows that line up current prices with underlying cash flow strength.

- Ride the momentum of cutting edge technology by checking out these 24 AI penny stocks that link artificial intelligence themes with listed companies.

- Add diversification beyond traditional sectors by reviewing these 18 cryptocurrency and blockchain stocks tied to cryptocurrency and blockchain developments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.