High Dividend Stocks Still Worth Buying After Rates Held Steady

Columbia Banking System, Inc. COLB | 0.00 |

With Kevin Warsh stepping in as Fed Chair, interest rates holding at 3.5% to 3.75%, and inflation running at 4.2% on the back of higher energy costs, income investors are facing a very different backdrop for high dividend yield stocks. Higher rates can reward strong balance sheets and expose weaker ones, so the quality of each dividend matters as much as the size. This article looks at 3 stocks from our High Dividend Yield Stocks screener that appear positively exposed to these shifts, helping you decide which opportunities might still fit a long term, income focused portfolio.

Columbia Banking System (COLB)

Overview: Columbia Banking System is a regional US bank based in Tacoma that offers a full suite of deposit, lending, mortgage, wealth management and treasury services to corporate, small business and retail customers.

Operations: Columbia Banking System generates all of its US$2.3b in revenue from banking activities in the United States.

Market Cap: US$8.9b

Income focused investors may want to pay attention to Columbia Banking System, which combines a 4.73% dividend yield with net profit margins around 28% and a long history of returning capital to shareholders. The stock is priced below one estimate of its fair value. However, its P/E sits slightly above the US banks average, so the market is already pricing in some of that quality. Recent earnings, a larger footprint following the Pacific Premier merger and active buybacks indicate confidence in the business. At the same time, past shareholder dilution, a relatively new management team and credit costs remain important considerations. A key issue for investors is whether its balance sheet and deposit base can translate higher Fed rates into a sustained income story for shareholders.

Columbia Banking System’s premium P/E, 4.73% yield and recent merger create a story that appears stronger than a simple headline ratio suggests. The 4 key rewards and 1 important major warning sign could reveal the one pressure point that changes the income thesis.

QBE Insurance Group (ASX:QBE)

Overview: QBE Insurance Group is a global general insurer based in Sydney that underwrites a wide range of commercial and personal policies, from property, motor and liability coverage to marine, energy, aviation and specialist lines, and also manages Lloyd’s syndicates and investment portfolios.

Operations: QBE Insurance Group generates about US$11.2b in revenue from its International division, US$8.2b from North America, US$5.7b from Australia Pacific and US$77m from Corporate & Other.

Market Cap: A$36.4b

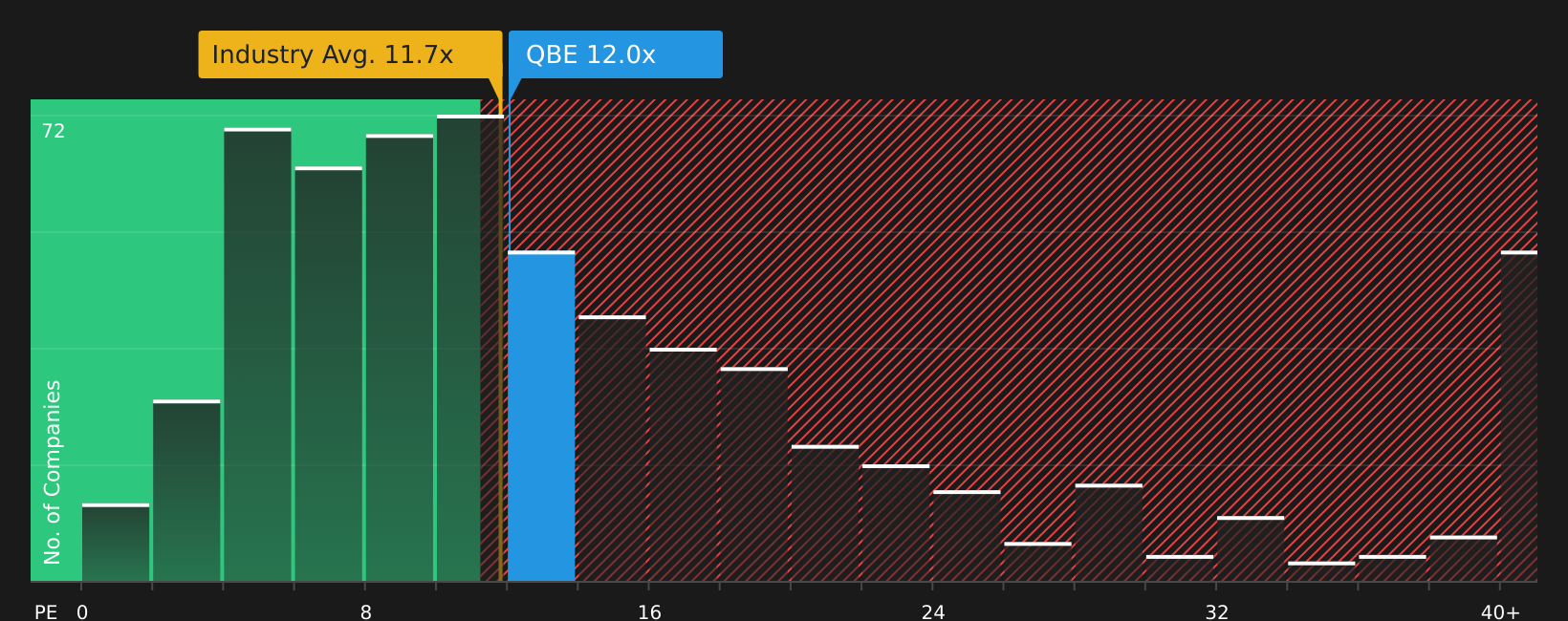

QBE Insurance Group may appeal in a higher rate environment because its core business collects premiums upfront and earns investment income on large float balances. It also currently offers a high dividend yield that is described as being backed by stable cash flows. Earnings grew 23.3% over the past year with profit margins at 11.4%, while the stock trades below one estimate of fair value and at a P/E of 11.9x versus peers at 20.4x. At the same time, management highlights pressure from softening premium rate increases, inflation risks and an unstable dividend record. Recent moves such as redeeming subordinated notes and refreshing the board indicate that the story is still evolving for income-focused investors, who may view QBE as a defensive insurer with trade offs to consider.

QBE’s earnings jump, high yield and P/E gap versus peers hint that investors may be missing how this insurer is really positioned in a 3.5% to 3.75% rate world. The 2 key rewards and 1 important warning sign could show whether that apparent value disguises one crucial weak spot or a misunderstood advantage

LCI Industries (LCII)

Overview: LCI Industries is a US based manufacturer of components used in recreational vehicles and related markets, supplying everything from chassis, axles and braking systems to doors, windows, furniture, appliances and electronics for RV makers and the aftermarket worldwide.

Operations: LCI Industries generates about US$3.2b of revenue from its Original Equipment Manufacturer segment and US$948m from its Aftermarket segment, with roughly US$3.8b coming from the United States and US$388m from international markets.

Market Cap: US$2.2b

Income investors may want to look closely at LCI Industries because it offers a 4.99% dividend yield, firmly reaffirmed even as the company manages a CEO transition, board reshuffle and talk of a potential all stock merger with Patrick Industries. Earnings grew faster than the wider Auto Components industry over the past year, the stock trades well below one estimate of fair value and analysts see further upside, yet debt levels and a weaker 5 year earnings trend mean the story is not without risk. With guidance for 2026 reiterated and the Fed holding rates at 3.5% to 3.75%, the key question is whether LCI’s mix of OEM and higher margin aftermarket cash flows can keep supporting that dividend as conditions evolve.

LCI Industries looks like an income story that could be mispriced, with that 4.99% yield, aftermarket cash flows and an all stock merger on the table, so the 6 key rewards and 1 important warning sign might be where the real tension in this setup shows up

The three high yield stocks in this article are just a starting point, with the full High Dividend Yield Stocks screener uncovering 12 more companies that pair elevated income with balance sheets and payout profiles that may support different long term income stories. Use Simply Wall St to identify, analyze and filter those ideas with the High Dividend Yield Stocks screener so you can focus on the catalysts, cash flow resilience and dividend narratives that best fit your own highest conviction income plays.

Take Control of Your Investment Journey

If QBE Insurance Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock stories can move from quiet to breakout fast, and once momentum is flying, the best entry points get caught and start dropping away, so act now.

- Spot early movers in future tech by scanning 49 AI infrastructure stocks, surfaced for investors who want exposure to the AI build out while it is still under the radar.

- Track companies quietly accumulating pricing power using the curated 67 resilient stocks with low risk scores, built to highlight resilient balance sheets and cash flows before the crowd fully catches on.

- Zero in on potential cash compounders with the targeted 7 dividend fortresses, focused on income stocks that pair elevated yields with fundamentals you can review while it still matters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.