Hilton Grand Vacations’ (HGV) Earnings Beat And Synergies: Efficiency Inflection Point Or One-Off Lift?

Hilton Grand Vacations, Inc. HGV | 40.49 | +0.07% |

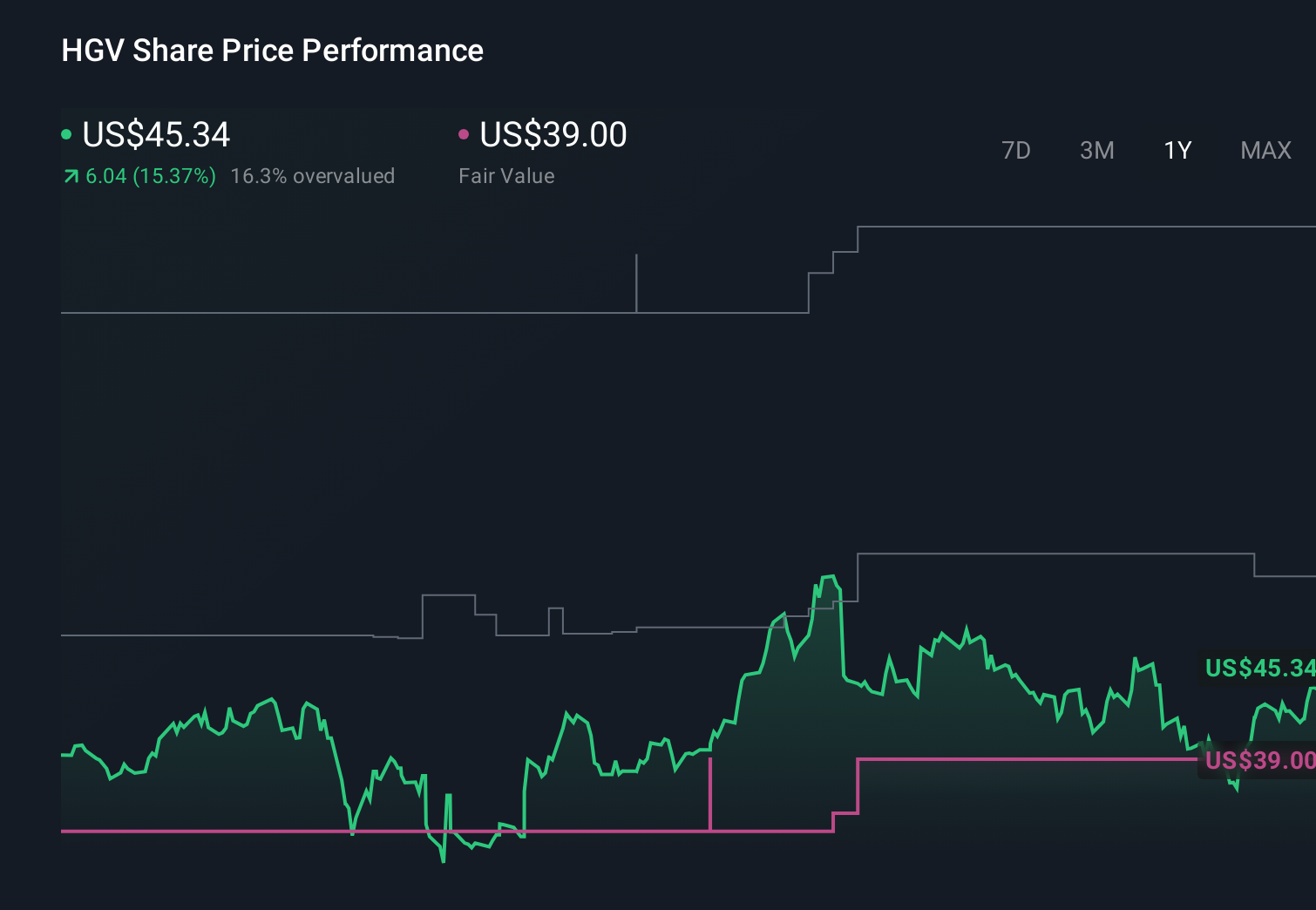

- Hilton Grand Vacations recently reported past fourth-quarter and full-year 2025 results showing higher revenue and net income year-on-year, while also completing a US$261.36 million buyback of 5,938,542 shares announced in July 2025.

- Beyond the headline earnings improvement, the company’s ahead-of-schedule US$100 million cost synergies from the Bluegreen acquisition highlight a meaningful shift in its efficiency and integration story.

- Next, we’ll explore how Hilton Grand Vacations’ strong earnings and accelerated Bluegreen cost synergies shape and potentially reinforce its existing investment narrative.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Hilton Grand Vacations Investment Narrative Recap

To own Hilton Grand Vacations, you need to believe its timeshare model, enlarged by Bluegreen and Diamond, can keep converting an engaged membership base into contract sales and earnings, while managing credit risk in its loan book. The latest results and buybacks support the near term earnings and capital return story, but they do not materially change the biggest current risk around elevated bad debt allowances and default rates in its receivables portfolio.

The most relevant update here is management reaching the US$100 million Bluegreen cost synergy target ahead of schedule, which ties directly into the integration catalyst that many investors are watching. Faster realized synergies, together with continued securitizations and access to the Japanese ABS market, give the company more flexibility to support margins and cash generation, which in turn underpins its ongoing share repurchase activity, including the recently completed US$261.36 million buyback.

Yet against this improving efficiency story, investors should also be aware that rising regulatory and data privacy obligations across key markets could...

Hilton Grand Vacations' narrative projects $6.4 billion revenue and $785.5 million earnings by 2028.

Uncover how Hilton Grand Vacations' forecasts yield a $52.00 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming revenue could reach about US$6.4 billion and earnings about US$962 million, far above consensus, but those views sit in tension with concerns about high bad debt allowances and customer defaults, showing just how differently you might interpret the same updates.

Explore 4 other fair value estimates on Hilton Grand Vacations - why the stock might be a potential multi-bagger!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hilton Grand Vacations research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Hilton Grand Vacations research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hilton Grand Vacations' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.