Hilton (HLT) Margin Expansion Reinforces Bullish Narratives Despite Softer Revenue Outlook

Hilton Worldwide Holdings Inc. HLT | 304.95 | -1.07% |

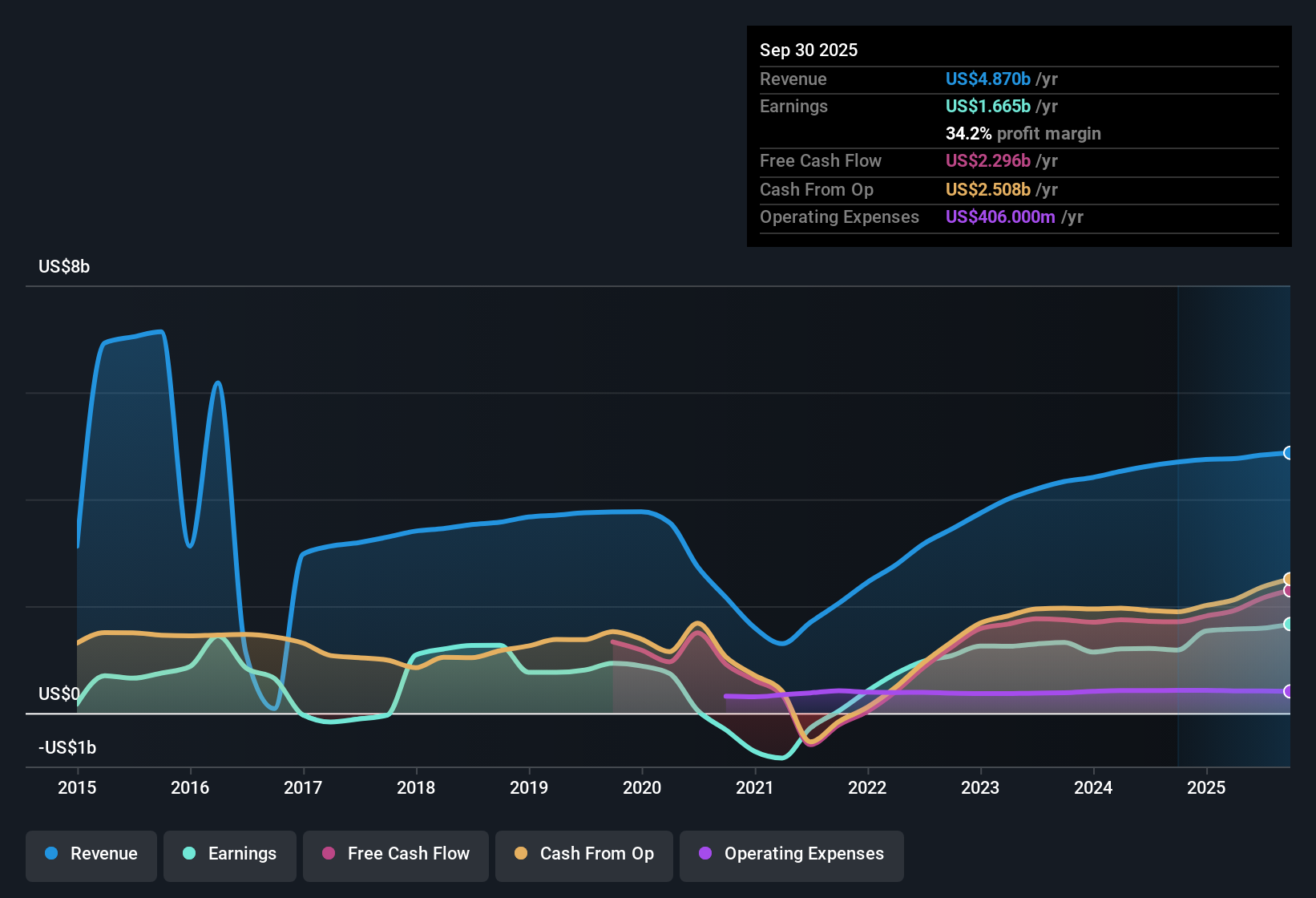

Hilton Worldwide Holdings (HLT) has put up another busy stretch of results, with Q3 FY 2025 revenue of US$1,283 million and EPS of US$1.79, backed by trailing 12 month revenue of US$4.9 billion and EPS of US$6.97 alongside a 41.5% earnings growth figure over the past year. The company has seen revenue move from US$1,196 million in Q4 2024 to US$1,326 million in Q2 2025, while quarterly EPS ranged from US$1.25 in Q1 2025 to US$2.08 in Q4 2024, giving investors a clear view of how the earnings line has tracked the top line. With net profit margin running at 34.2% compared with 25.1% a year earlier, the latest print sets up a margin centric story that investors will be watching closely.

See our full analysis for Hilton Worldwide Holdings.With the numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around Hilton's growth, profitability and longer term prospects, and where those stories might need a rethink.

TTM net income holds above US$1.6b

- On a trailing twelve month basis, Hilton generated about US$1.7b of net income on US$4.9b of revenue. This aligns with the 34.2% net profit margin mentioned earlier and shows how much of each dollar of revenue is currently dropping to the bottom line.

- Analysts' consensus view links this margin profile to Hilton's asset light model and premium mix, yet also flags risks:

- The consensus narrative points to an asset light structure and focus on lifestyle and luxury brands as supportive of high margins. The 34.2% net margin on roughly US$4.9b of revenue is consistent with that.

- At the same time, the same narrative highlights softer system wide RevPAR guidance of flat to up only 2% for 2025, which sits alongside trailing net income of about US$1.7b and suggests investors are weighing high current profitability against more moderate topline expectations.

Revenue forecasts trail broader US market

- Revenue is forecast to grow about 7.7% per year, compared with the 10.4% forecast for the broader US market, even though Hilton's trailing twelve month revenue is around US$4.9b, which is already a large base for a hotel operator.

- Consensus narrative arguments about future growth sit next to these forecasts in an interesting way:

- The narrative highlights a record 510,000 rooms in progress and 221 hotel openings in one quarter as long term growth drivers, which would normally be associated with stronger revenue growth than the 7.7% figure implied here.

- It also calls out structural demand softness in segments like business and group travel and flat to slightly higher RevPAR guidance, which could help explain why forecast revenue growth sits below the broader US market despite the large development pipeline.

Rich valuation versus DCF and P/E peers

- Hilton trades on a P/E of 45.4x with a current share price of US$325.13, compared with a DCF fair value of US$132.93 and a hospitality industry P/E of 21.8x and peer average of 25.5x, so the stock is priced well above both the provided cash flow estimate and sector multiples.

- Consensus narrative expectations for growth and profitability meet this pricing in a way that careful investors will likely want to unpack:

- The narrative leans on aggressive global expansion, a large development pipeline and an asset light model as reasons why earnings might hold up over time. This aligns with trailing earnings growth of 41.5% and analysts' expectations for about 12% annual earnings growth.

- However, those same views sit beside a forecast that profit margins could shrink from around the low 30s to 16.6% in three years and that Hilton carries a high level of debt. This combination can make a 45.4x P/E and a price far above the US$132.93 DCF fair value look demanding if future conditions turn out differently from these assumptions.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Hilton Worldwide Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a fresh look at the data, shape your own view in just a few minutes and Do it your way

A great starting point for your Hilton Worldwide Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Hilton combines high margins and earnings growth with a P/E of 45.4x and a share price far above the US$132.93 DCF fair value, which makes the valuation look demanding.

If that kind of pricing makes you cautious, put your capital to work by scanning our 51 high quality undervalued stocks to quickly compare companies where the valuation hurdle looks less steep.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.