Home Depot Stock and Retail Peers Facing a Key Consumer Spending Test

Home Depot, Inc. HD | 0.00 |

Immigration policy rarely shows up on a stock screener, yet the Supreme Court’s TPS decision and a surge in ICE activity could reshape spending patterns for communities and the large retail chains that serve them. With up to 1.3 million workers and consumers facing the loss of legal work status, some retailers may see pressure on store traffic and local revenue, while others might prove more resilient thanks to broad national footprints and diverse customer bases. This article looks at three large cap retail stocks exposed to this news, to help you decide which may warrant closer attention or extra caution.

Burlington Stores (BURL)

Overview: Burlington Stores operates a nationwide off price retail chain focused on branded apparel, home goods, toys, beauty and baby products for value conscious shoppers across the United States and Puerto Rico.

Operations: The company generates all of its US$11.9b in revenue from retail apparel and related merchandise in the United States.

Market Cap: US$19.4b

Investors looking at Burlington Stores are weighing a fast growing off price chain with a nationwide footprint against meaningful balance sheet and execution risks. Burlington 2.0 focuses on smaller, higher productivity stores, automation and supply chain upgrades, while store openings in selected regions are intended to help absorb demand as smaller local retailers experience workforce disruption related to tougher immigration enforcement. At the same time, leverage, insider selling and limited digital investment may leave less room for error if consumer spending changes or traffic shifts online more quickly. How that trade off compares with today’s valuation is a key consideration for investors assessing the opportunity and the risks.

Burlington’s accelerating store rollout and Burlington 2.0 upgrades can look compelling, but the real question is whether the balance sheet leaves enough cushion if spending stumbles. Get the full picture in the Burlington Stores financial health report

Williams-Sonoma (WSM)

Overview: Williams-Sonoma is an omni-channel retailer that sells cookware, furniture, and home decor under brands like Williams Sonoma, Pottery Barn, West Elm, and Pottery Barn Kids through its stores, catalogs, and e-commerce sites in the United States and abroad.

Operations: Williams-Sonoma generates about US$7.9b in revenue from home furnishing retail, with roughly US$7.6b from the United States and US$316.9m from international markets.

Market Cap: US$26.4b

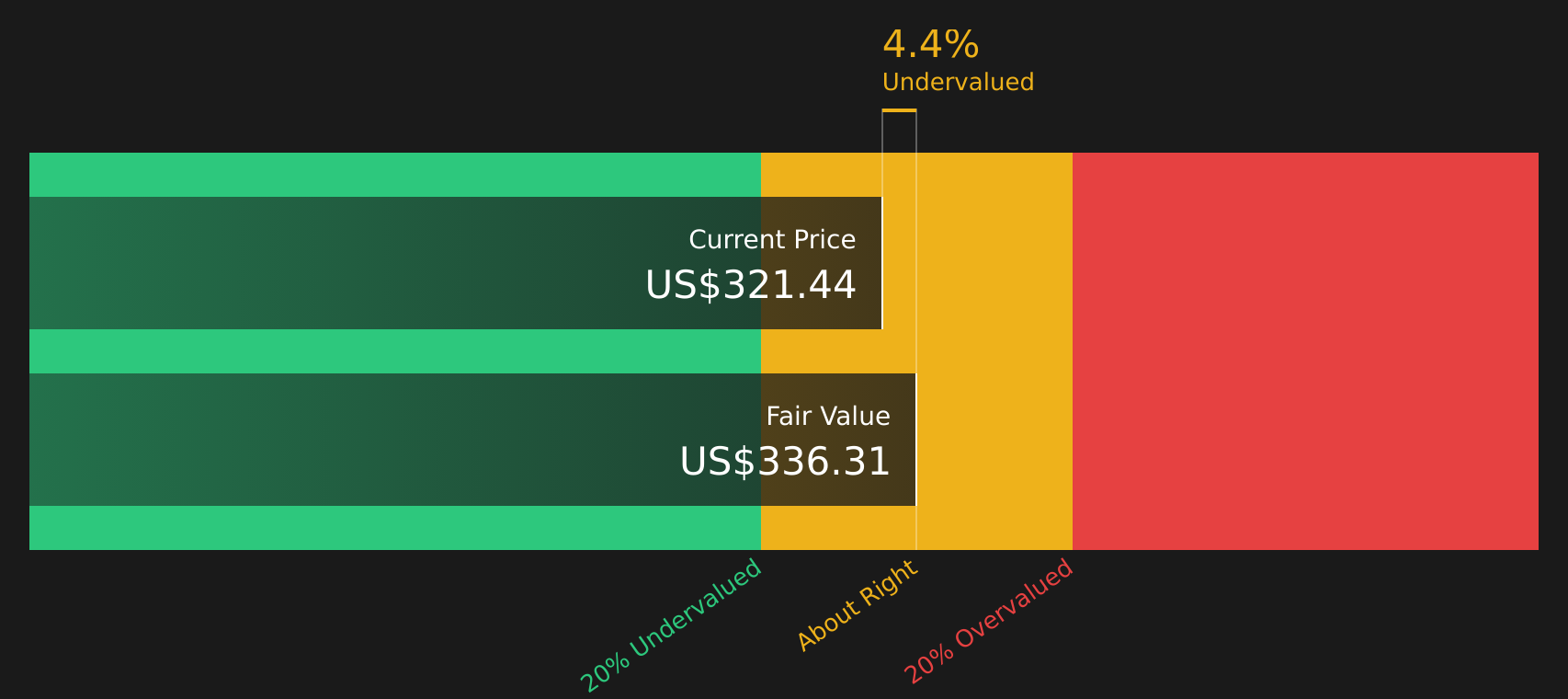

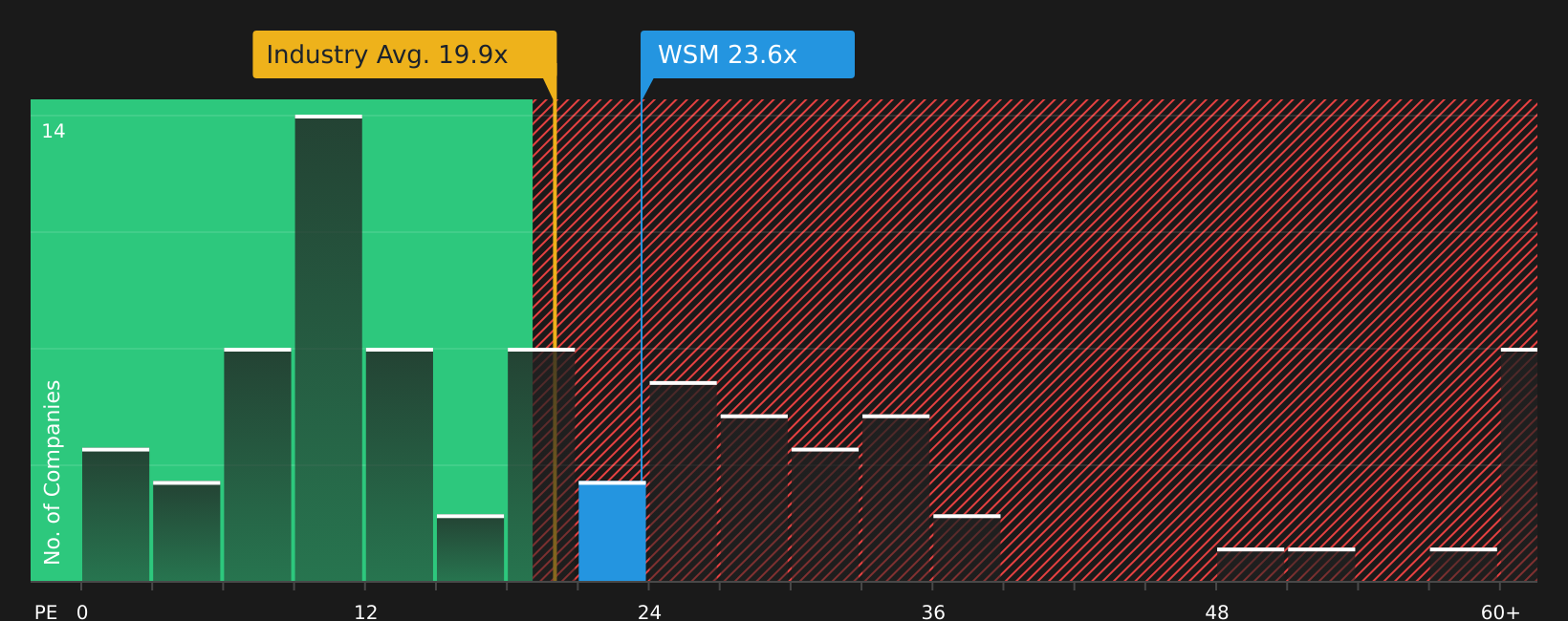

Williams-Sonoma offers a mix of premium home brands and digital capabilities at a time when smaller local retailers may be more exposed to immigration related disruption and weaker foot traffic. The company pairs a 1.37% dividend, net margins of 13.8%, and a 58.2% ROE with active buybacks, even as growth forecasts are modest and management uses external borrowing. Recent collaborations across Pottery Barn and Williams Sonoma indicate brand momentum, but revenue softness, store closures, and a P/E above peers mean investors may be paying a premium for quality and resilience. A key consideration is whether its margin profile and affluent customer base justify that premium as conditions evolve.

Williams-Sonoma’s rich margins, dividend, and buybacks suggest strength; however, the premium P/E raises questions about what is already priced in. Get the fuller story in the analysis report for Williams-Sonoma

Home Depot (HD)

Overview: Home Depot is a home improvement retailer that sells building materials, décor, lawn and garden products, and maintenance supplies to both households and professional contractors, while also offering installation, tool rental, and a suite of online channels across North America and selected international markets.

Operations: Home Depot generates about US$166.6b in revenue, with roughly US$152.4b from U.S., Canada, and Mexico retail operations and US$14.2b from other revenue streams.

Market Cap: US$349.6b

Home Depot stands out in this screener because it combines a large store and distribution network with a growing ecosystem for professional customers. This comes at a time when immigration crackdowns could weigh more heavily on smaller, locally focused rivals. The company’s investments in technology, Pro services, and acquisitions such as SRS and the planned GMS deal are aimed at winning complex, higher ticket projects. Its long dividend record and “high quality earnings” may appeal to income focused investors. However, high leverage, recent earnings softness, and pressure on margins mean any hit to housing related demand or contractor activity could be more significant than in the past. Understanding the balance between its scale advantages and debt load is therefore important.

Home Depot’s scale, Pro ecosystem, and long dividend record suggest a stronger earnings engine than many assume. However, its debt and housing exposure could be hiding a crucial twist revealed in the analysis report for Home Depot

The three stocks here are just a starting point, with the full Large-Cap National Retail Chains screener uncovering 21 more large cap retail companies that share similarly compelling risk and reward stories. Use Simply Wall St to identify and analyze the exact catalysts, financial traits, and narratives that matter most so you can focus on your highest conviction ideas across this group.

Take Control of Your Investment Journey

If Home Depot or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Fresh Investing Alternatives?

Markets move fast and fresh ideas do not stay under the radar for long. Spot potential breakouts and momentum plays before the crowd, while it matters. Act now.

- Target steady income hunters by scanning a curated set of reliable payers with the 9 dividend fortresses before yields get compressed by price momentum.

- Catch early movers in real assets by reviewing a hand picked group of 33 elite gold producer stocks while they are still flying under most investors’ radar.

- Position for the next wave of industrial growth by checking a focused basket of 8 top copper producer stocks before capital flows reprice these producers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.