Honeywell International (HON) As Its AI Automation Push Reshapes The Valuation Debate

Honeywell Technologies Inc. HON | 0.00 |

Honeywell International (HON) is in the spotlight after unveiling Experion Cognition, an AI powered autonomous control system; spinning off into a standalone automation focused business; and completing a recent reverse stock split.

Despite the automation spin off, Experion Cognition launch and reverse stock split drawing fresh attention, Honeywell International’s share price is down 42.55% year to date. Its 5 year total shareholder return of 12.81% points to weaker recent momentum versus longer term results.

If these shifts toward AI and automation have you rethinking your exposure to the theme, this could be a useful moment to scan 52 AI infrastructure stocks

Honeywell International’s share price slide, recent reverse split, and new focus on automation leave a wide gap between today’s US$225.05 price and published fair value estimates. How does that spread compare with the valuation work that follows?

Most Popular Narrative: 29.7% Undervalued

The most followed Honeywell International narrative points to a fair value of $320.19 per share, well above the last close at $225.05, and frames the current discount through the lens of automation, energy technology and policy aligned quantum exposure.

HON RemainCo is a pure-play industrial automation and energy technology compounder with a confirmed June 29 catalyst, $19B+ in contracted backlog, a sold-out LNG order book, a global SAF technology licensing position, a recurring revenue platform transition underway via Forge, and an embedded position on both sides of the energy transition, all trading at a conglomerate discount that disappears in 53 days.

The headline figure is only part of the story. The full narrative leans on a specific revenue mix shift, margin profile, and valuation multiple that together do the heavy lifting for that $320.19 figure.

Result: Fair Value of $320.19 (UNDERVALUED)

However, this Honeywell International thesis could be pressured if automation growth falls short of expectations or if the planned separation fails to close the current valuation gap.

Another View on Honeywell International’s Valuation

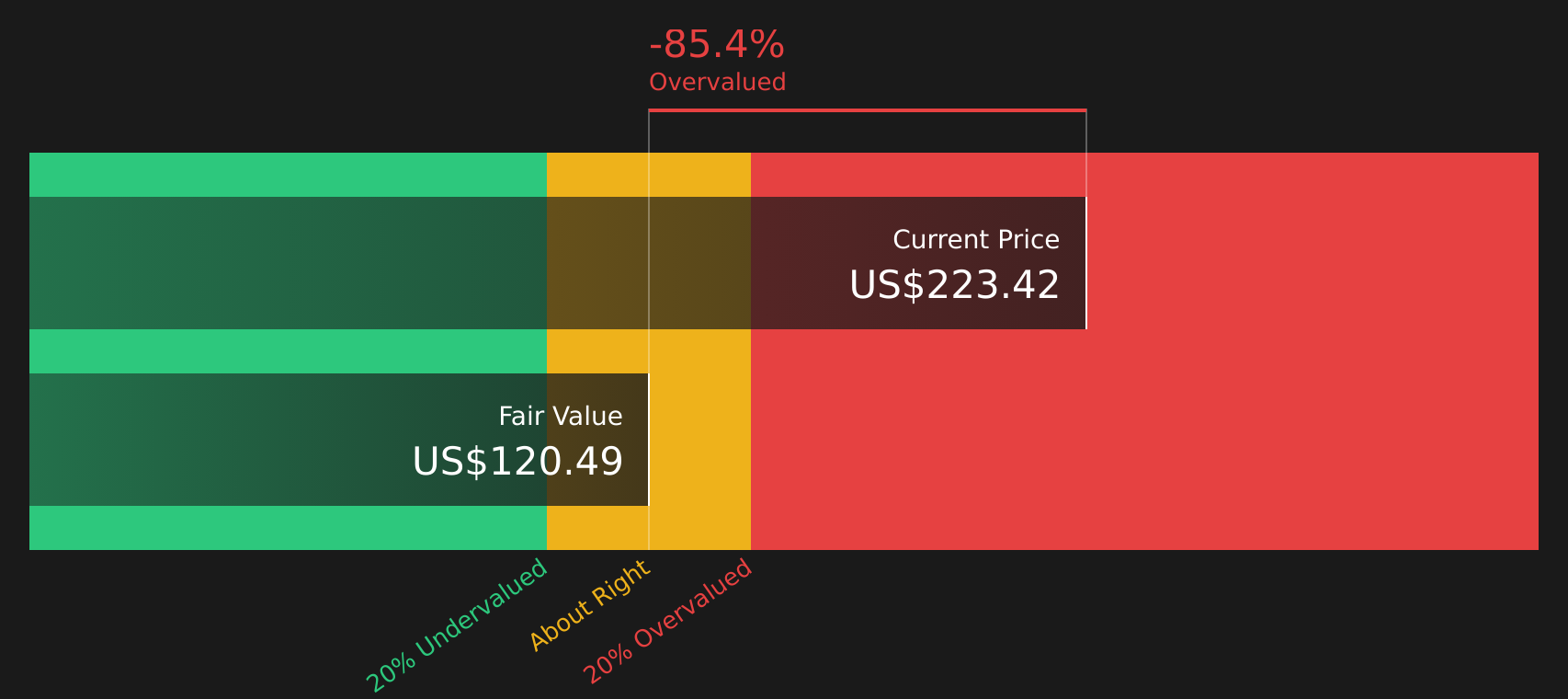

The user generated narrative argues Honeywell International is around 29.7% undervalued at $225.05 versus a fair value of $320.19, but the SWS DCF model paints a very different picture. On that framework, the stock trades well above an estimated future cash flow value of $124.49, which points to a rich price rather than a bargain. Which lens feels more realistic given your own expectations for cash generation, margins, and growth?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Honeywell International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on Honeywell International’s valuation and outlook, this is a good time to move quickly, review the data, and weigh both 2 key rewards and 4 important warning signs

Looking for more Honeywell International sized investment ideas?

If Honeywell International has you thinking harder about where your capital is working hardest, do not stop here; broaden your watchlist before the next move.

- Target dependable cash generators by scanning 45 high quality undervalued stocks that pair quality fundamentals with prices that still sit below many investors’ radar.

- Anchor your portfolio with income focused opportunities by reviewing 9 dividend fortresses offering higher yields that may complement Honeywell International’s risk profile.

- Sleep easier through market swings by checking 74 resilient stocks with low risk scores built around companies with lower risk scores and sturdier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.