Housing Stocks Back In Focus As Cooling Inflation Revives Rate Cut Hopes

Louisiana-Pacific Corporation LPX | 0.00 |

June inflation cooling to 3.5% with a sharp pullback in gasoline prices and a softer headline consumer price index has turned the spotlight back on interest rate expectations and housing costs. For residential housing and real estate stocks, even small changes in inflation and energy prices can affect borrowing costs, construction budgets, and buyer confidence. This article looks at how this latest inflation print and the move in energy and housing components could matter for larger, housing focused companies. You will see 3 stocks exposed to this news and how this setup might support or challenge their investment appeal.

Louisiana-Pacific (LPX)

Overview: Louisiana-Pacific is a building products company that supplies engineered wood siding, trim and structural panels for new homes, remodeling projects and outdoor structures across North and South America, selling mainly to retailers, wholesalers and homebuilders.

Operations: Louisiana-Pacific generates most of its revenue from Siding at about US$1.6b, with Oriented Strand Board (OSB) contributing roughly US$733m and Other operations around US$179m.

Market Cap: US$5.3b

Louisiana-Pacific provides direct exposure to U.S. housing activity through its siding and OSB products. Recent commentary points to cooling inflation, easing gas prices and discussion of lower rate pressure as potential supports for construction and remodeling appetite, while indications of deflation in some raw materials suggest possible cost relief. The company is investing heavily in higher value siding such as SmartSide and ExpertFinish, including a new ExpertFinish facility planned in Minnesota, which management aims to use to improve product mix and margins if demand is supportive. At the same time, current margins are thin, earnings have been under pressure and the stock trades on a relatively high P/E with questions around dividend coverage, so understanding how these investment plans and cost trends interact with those risks remains important.

Louisiana-Pacific’s push into higher value siding with thin margins and a relatively high P/E can make the full picture easy to misread, so it helps to see how the growth story and pressure points actually fit together in the 2 key rewards and 3 important warning signs (1 is major!)

Fletcher Building (NZSE:FBU)

Overview: Fletcher Building is a diversified construction and building products company that manufactures and distributes materials like cement, concrete, plasterboard, steel, roofing, and plumbing supplies. It also develops and builds residential and commercial properties and delivers major infrastructure projects in New Zealand, Australia, and other markets.

Operations: Fletcher Building generates most of its segment revenue from Distribution at about NZ$1.5b. Residential and Development contributes around NZ$528m, Corporate about NZ$10m and there is a segment adjustment of roughly NZ$5.7b, alongside eliminations of NZ$725m. Geographically, it records about NZ$4.9b from New Zealand, NZ$1.8b from Australia and NZ$35m from other regions.

Market Cap: NZ$3.9b

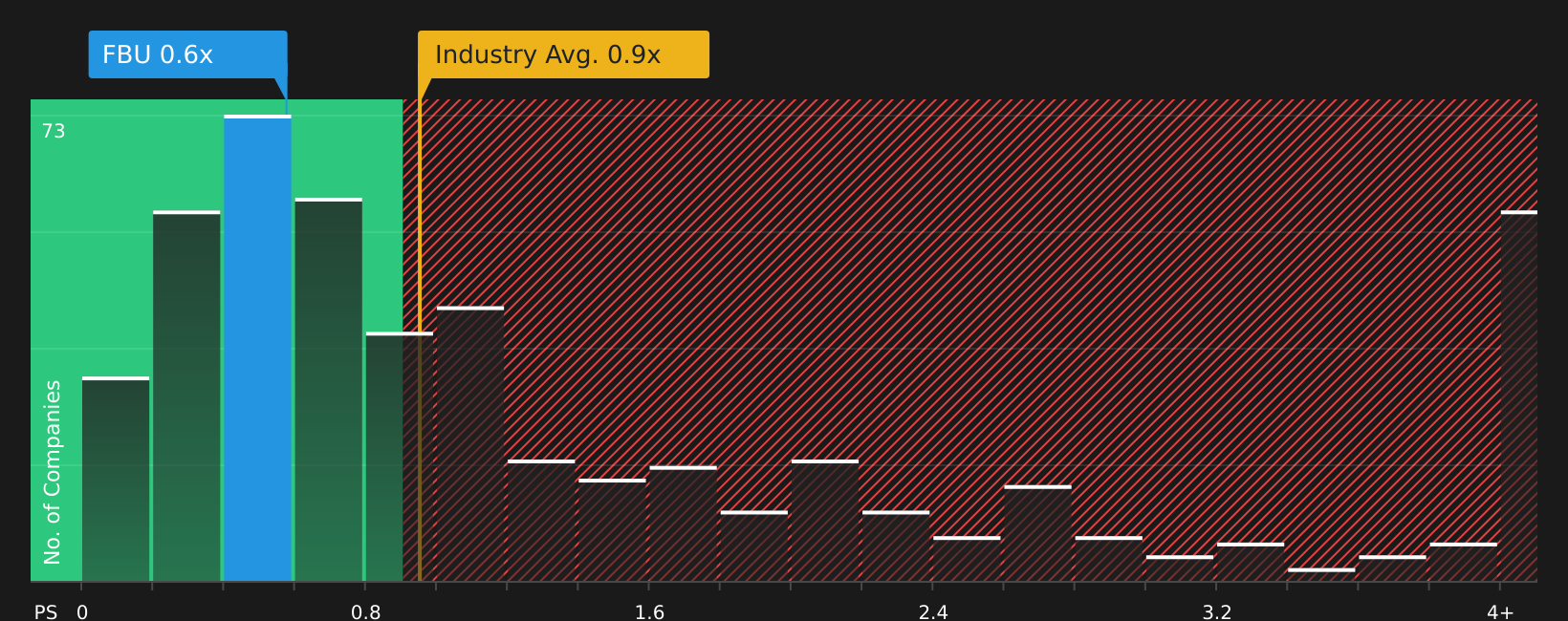

Fletcher Building gives you broad exposure to housing and infrastructure activity at a time when inflation and energy costs are showing signs of relief, which can help construction budgets and project confidence. The company is still loss making with a weak recent return on equity and relies on external borrowings. Analysts currently anticipate a path to profitability within roughly three years and have published forecasts that show higher future earnings alongside modest revenue growth. Management has also lifted earnings guidance for FY2026, which indicates confidence in current initiatives to manage costs and improve performance. With the stock trading at a low P/S multiple compared with peers and the New Zealand building industry, the balance between relatively low pricing and ongoing execution and funding risks is what makes Fletcher Building a candidate for further research.

Fletcher Building’s mix of construction exposure, easing cost pressures and a low P/S hints that the market may be missing something. See how that combination stacks up in the analysis report for Fletcher Building

Taylor Wimpey (LSE:TW.)

Overview: Taylor Wimpey is a long-established homebuilder that designs, builds, and delivers residential communities across the United Kingdom and Spain, offering a range of homes from first-time buyer properties to larger family houses.

Operations: Taylor Wimpey generates the majority of its revenue from the United Kingdom at about £3.7b, with Spain contributing around £193m.

Market Cap: £2.9b

Taylor Wimpey provides focused exposure to UK new-build housing at a time when inflation is cooling and borrowing cost expectations are easing. This environment can support buyer confidence and affordability, even though the company still faces margin pressure. A deep land bank, experienced management and efforts to improve build efficiency and sustainability sit alongside a 9.25% dividend yield that is not well covered, a recent one-off loss of £243.8m, and a high profile class action that could weigh on sentiment and future liabilities. With analysts expecting faster earnings growth than the wider UK market but profitability currently subdued, investors who understand how these strengths and risks fit together may see more than the headline P/E suggests.

Taylor Wimpey’s high headline yield, recent one off loss and class action risk make the story feel stalled. Yet the real tension sits in how those pieces fit with the analyst forecasts for Taylor Wimpey

The three stocks covered here are just the starting point, with the full U.S. Housing and Real Estate Stocks screener uncovering 13 more companies that share similar housing focused themes and equally detailed narratives. Use Simply Wall St to evaluate specific catalysts, balance sheet strength, and business profiles so you can focus on the highest conviction housing and real estate ideas.

Take Control of Your Investment Journey

If Fletcher Building or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Housing?

Fresh stock ideas do not stay under the radar for long. Use these screeners to spot momentum before the crowd catches on. While it matters, aim to get in early.

- Target dependable income streams by scanning a curated set of high-yield companies with the 10 dividend fortresses before rising attention narrows the most attractive entry points.

- Spot potential infrastructure leaders by reviewing the 34 power grid technology and infrastructure stocks while these grid and electrification companies are still priced for early movers rather than late followers.

- Explore the next wave of automation by checking the 32 robotics and automation stocks where select companies could benefit if demand continues and efficiency trends remain in focus.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.