How AI-Driven Job Cuts And Leadership Shake-Up At Salesforce (CRM) Has Changed Its Investment Story

Salesforce.com, inc. CRM | 0.00 |

- In early February 2026, Salesforce cut nearly 1,000 jobs and reshuffled senior leadership as part of a broader shift to deepen its use of artificial intelligence and automation across the business.

- This restructuring, alongside an AI-focused acquisition and ongoing sector unease about agentic AI, highlights how Salesforce is actively reconfiguring its operations and product mix for an automation-first era.

- Against this backdrop of AI-driven restructuring and fresh layoffs, we’ll now examine how Salesforce’s operational reset reshapes the company’s investment narrative.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

Salesforce Investment Narrative Recap

To own Salesforce today, you need to believe its AI and agentic automation push will deepen customer lock‑in faster than emerging AI tools can commoditize CRM. The latest 1,000 job cuts and leadership reshuffle underscore that AI is now central to how Salesforce runs and sells, but they do not obviously change the near term catalyst of Agentforce and Data Cloud adoption or the key risk that powerful AI platforms from others could displace parts of its stack.

The Cimulate acquisition stands out here. By adding intent‑aware, AI search into Agentforce Commerce, Salesforce is reinforcing one of the very businesses investors are watching most closely as a growth driver. This move sits alongside rising concern about agentic AI encroaching on traditional SaaS, and it gives investors another concrete datapoint to weigh against both the potential upside from AI monetisation and the risk of its own tools accelerating customer cost cutting.

Yet beneath Salesforce’s AI story, one risk investors should watch carefully is how far automation might pressure margins if...

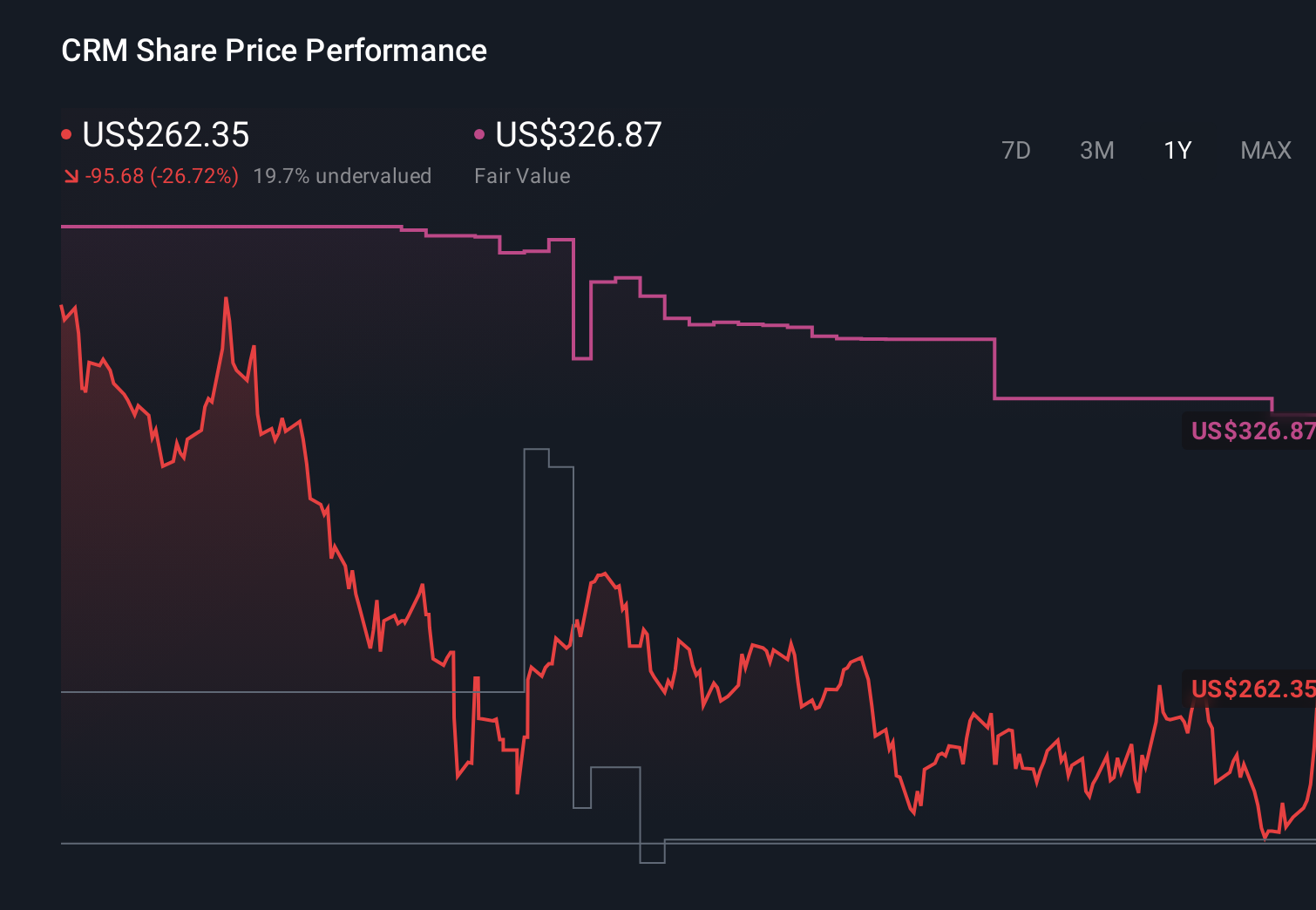

Salesforce's narrative projects $51.9 billion revenue and $10.3 billion earnings by 2028. This requires 9.6% yearly revenue growth and about a $3.6 billion earnings increase from $6.7 billion today.

Uncover how Salesforce's forecasts yield a $327.86 fair value, a 73% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Salesforce could reach about US$56.2 billion in revenue and US$12.0 billion in earnings by 2028, but after layoffs tied directly to AI and automation, you should expect that both these bullish and more cautious narratives might be revisited as investors reassess how much of that growth comes from the very automation that could also unsettle Salesforce’s core value proposition.

Explore 42 other fair value estimates on Salesforce - why the stock might be worth just $241.03!

Build Your Own Salesforce Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.