How Alphabet’s (GOOGL) Antitrust Court Victory Has Changed Its Investment Story

Alphabet Inc. Class A GOOGL | 295.77 | -0.54% |

- Earlier in September 2025, a federal judge ruled that Alphabet would not have to divest its Chrome browser or make structural changes, easing one of its most significant antitrust risks.

- This legal outcome preserves Alphabet's core ecosystem, allowing the company to focus on AI integration and expanding its cloud computing capabilities amid rising industry competition.

- We'll now explore how the court’s removal of major regulatory risks could influence Alphabet’s investment narrative and future prospects.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 29 companies in the world exploring or producing it. Find the list for free.

Alphabet Investment Narrative Recap

To stand behind Alphabet as a shareholder, you need confidence in its ability to sustain global leadership in AI-driven search, digital advertising, and cloud computing, while managing high capital expenditures and persistent regulatory risks. The recent court ruling relieves near-term structural uncertainty, keeping investor focus sharply on the pace of AI integration and competition as the primary catalyst, and on growing regulatory and industry challenges as the key risk. With the core ecosystem intact, the news does not materially alter Alphabet’s top short-term catalyst or its largest ongoing risk.

Alphabet’s Q2 2025 earnings underscore the resilience behind recent optimism: sales climbed to US$96.4 billion while net income reached US$28.2 billion, both showing solid growth year-over-year. This financial momentum, paired with the court victory, maintains focus on scaling AI monetization in Search and Cloud, even as competition and regulatory scrutiny remain persistent concerns. The company’s continued strong results reinforce why investor attention is centered on the pace of AI-enabled business evolution, post-litigation.

Yet, even as legal clouds clear, investors should not lose sight of the ongoing risk from intensifying AI and digital ad competition, which ...

Alphabet's outlook anticipates $512.6 billion in revenue and $148.4 billion in earnings by 2028. This projection is based on an expected annual revenue growth rate of 11.3% and represents a $32.8 billion increase in earnings from the current $115.6 billion.

Uncover how Alphabet's forecasts yield a $231.48 fair value, a 3% downside to its current price.

Exploring Other Perspectives

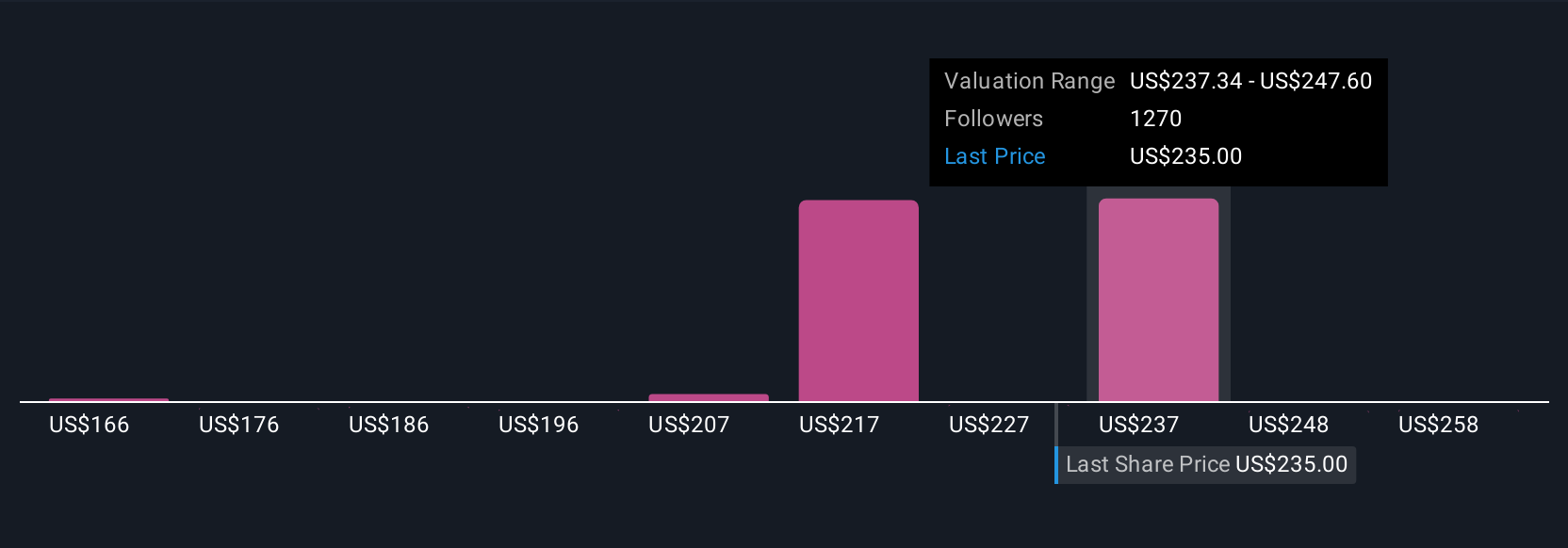

Nearly 200 individual fair value estimates from the Simply Wall St Community span US$165.53 to US$268.42 per share. As you explore these diverse opinions, keep in mind that Alphabet’s biggest catalyst remains scaling AI monetization, which could influence long-term revenue and margin performance.

Explore 197 other fair value estimates on Alphabet - why the stock might be worth 31% less than the current price!

Build Your Own Alphabet Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Alphabet research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Alphabet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alphabet's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 9 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.