How Amazon’s Move Into Rappi Impacts the MercadoLibre Investment Case in 2025

MercadoLibre, Inc. MELI | 1715.52 | -0.20% |

If you have MercadoLibre stock in your portfolio, or you are thinking about starting a position, you are hardly alone in that curiosity. This is one of Latin America’s most dynamic growth stories, and lately, it has been anything but boring for investors. MercadoLibre shares are up an impressive 27.3% so far this year, and they are holding onto a solid 141.8% gain over the past three years. Even across five years, the stock is up 93.6%. That kind of performance is what gets attention.

Of course, the past month has been a reminder that the journey is rarely smooth. In just the last week, the stock pulled back 9.9%. Over the past 30 days, MercadoLibre declined by 5.6%. Part of this may be due to broader concerns about competition, especially as reports surfaced that Amazon is making moves in Latin America by acquiring a stake in Rappi, a well-known Colombian delivery company. This has led some investors to reexamine MercadoLibre’s growth path and risk profile, but it may also be an opportunity for those who still believe in the company’s long-term edge.

When it comes to valuation, the numbers are as interesting as the headlines. According to a simple scorecard, MercadoLibre is undervalued in 3 out of 6 checks, giving it a value score of 3. That is a signal worth examining further, but not the only piece of the puzzle.

So, how do the usual valuation approaches stack up for MercadoLibre, and is there a smarter way to cut through the noise? Let’s break down the numbers, then explore an even better lens for understanding what this stock is really worth.

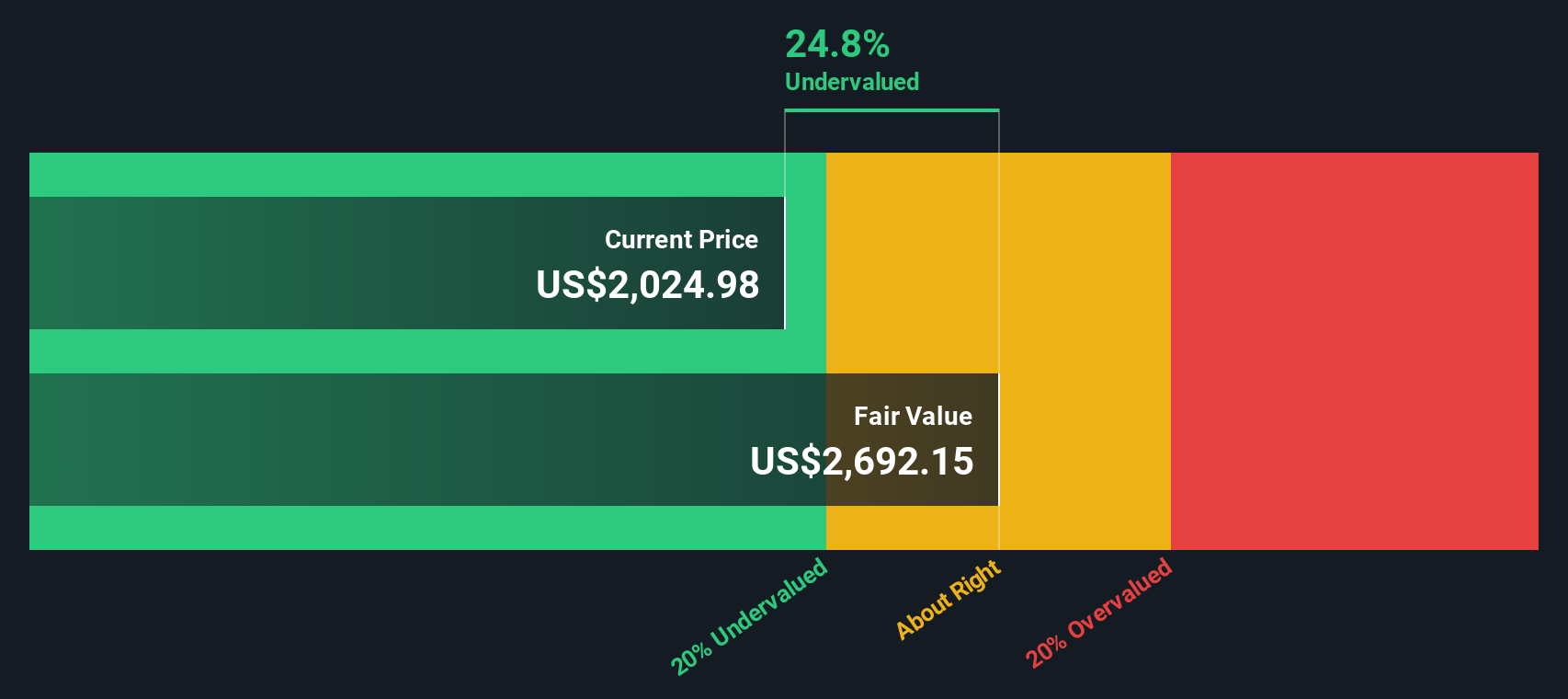

Approach 1: MercadoLibre Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model works by projecting a company’s future cash flows, then discounting them back to today’s value to estimate what the whole business is really worth in present terms. This approach aims to cut through market noise and focus on a company’s core earning power.

For MercadoLibre, the current Free Cash Flow stands at $7.52 Billion. Analyst forecasts project continued growth, with cash flows expected to reach $9.58 Billion by the end of 2027. After that, further increases are extrapolated. By 2035, projections have Free Cash Flow above $14 Billion, though those later years are based on assumptions rather than analyst consensus.

Using these projections, the DCF model calculates an estimated intrinsic value of $2,698 per share. Compared to the stock’s current price, this valuation implies the shares are trading at a 16.7% discount, suggesting MercadoLibre is undervalued by the market at these levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests MercadoLibre is undervalued by 16.7%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

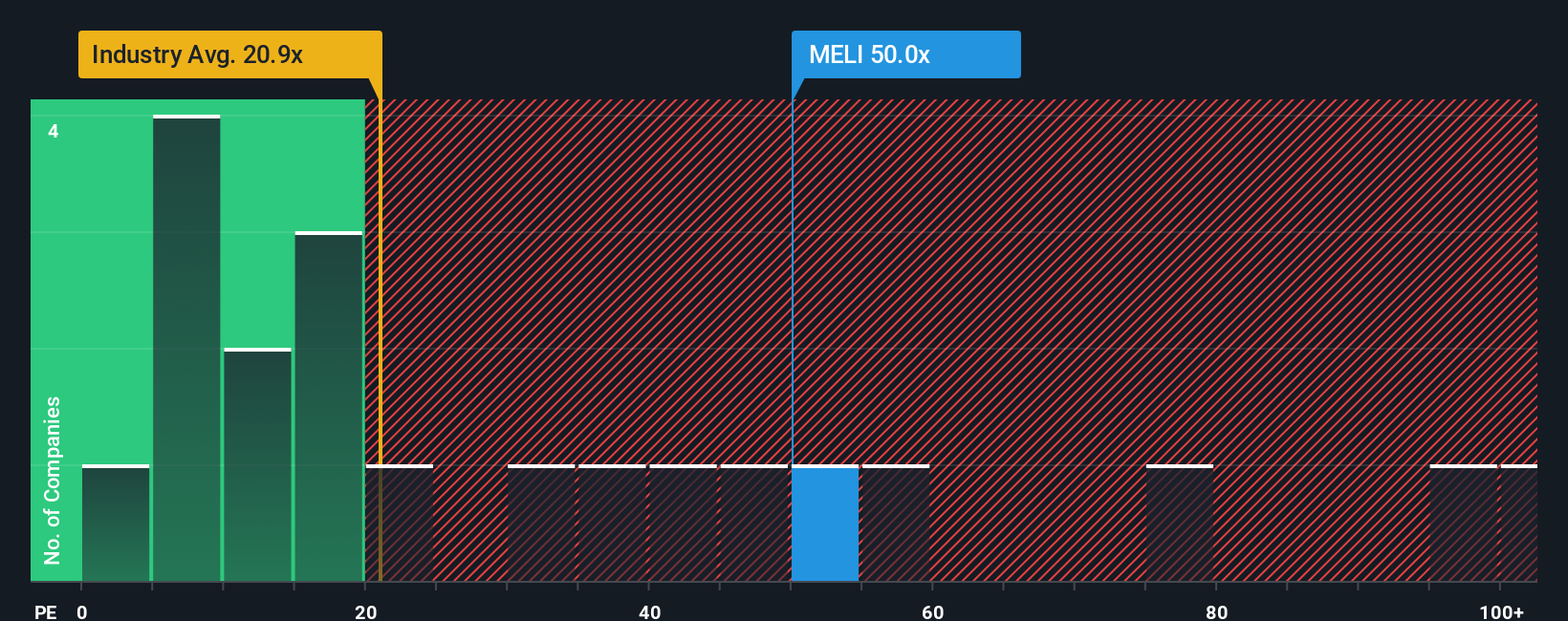

Approach 2: MercadoLibre Price vs Earnings

The Price-to-Earnings (PE) ratio is widely regarded as the go-to metric when valuing profitable companies, since it connects a stock’s price directly to the earnings generated for shareholders. For growing, established businesses like MercadoLibre, the PE ratio is especially relevant because it reflects both current profitability and the market’s outlook for future growth and risk.

Growth expectations and risk both play a crucial role in determining what counts as a “fair” PE ratio. Companies with higher earnings growth or more stable operations often trade at higher multiples, while riskier or slower-growing peers generally have lower valuations.

MercadoLibre currently trades at a PE ratio of 55.5x. This is considerably higher than the Multiline Retail industry average of 21.7x and also above the average of its direct peers at 69.3x. However, these comparisons do not tell the whole story.

This is where Simply Wall St’s Fair Ratio becomes relevant. Unlike simple industry or peer multiples, the Fair Ratio is a dynamic benchmark, estimating the suitable PE multiple for MercadoLibre by factoring in its anticipated earnings growth, risk profile, profit margins, industry conditions, and even its market capitalisation. In this case, MercadoLibre’s Fair Ratio is 33.6x, which gives a more tailored sense of its valuation than the flat industry or peer averages.

With MercadoLibre’s actual PE (55.5x) above the Fair Ratio (33.6x), the shares appear to be trading at a premium, reflecting the market’s high expectations for future performance.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

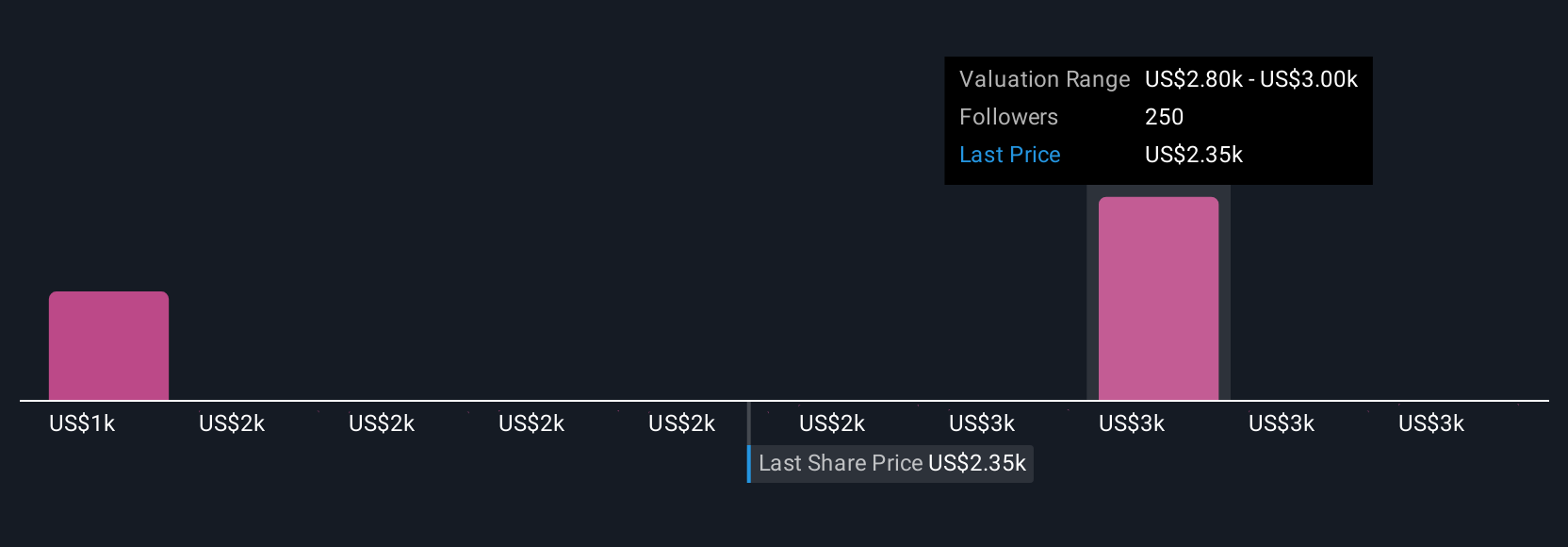

Upgrade Your Decision Making: Choose your MercadoLibre Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. Narratives are a more dynamic and insightful tool for making investment decisions. A Narrative is simply your story about a company: the perspective you take on its future prospects, supported by your own assumptions for fair value, revenue growth, earnings, and profit margins. Rather than just relying on numbers, Narratives connect your view of MercadoLibre’s business story to a financial forecast and, ultimately, to a personalized fair value estimate.

This approach is easy and accessible, offered right on Simply Wall St’s platform (in the Community page used by millions of investors). It allows anyone to create or follow Narratives that reflect different expectations or risk tolerances. Narratives empower you to see, at a glance, whether your fair value estimate suggests MercadoLibre is a buy, hold, or sell compared to its current market price. They also auto-update whenever fresh news, earnings, or data become available, so your insights stay relevant in real time.

For example, the most bullish MercadoLibre Narrative sees massive fintech adoption driving a price target as high as $3,500, while the most cautious expects competitive pressures to limit growth and values it as low as $2,170.

Do you think there's more to the story for MercadoLibre? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.