How Atlassian’s (TEAM) Acquisition of The Browser Company Has Changed Its AI Investment Story

Atlassian Corp Class A TEAM | 68.25 | +2.05% |

- Atlassian recently completed its acquisition of The Browser Company of New York Inc. to advance development of an AI-powered browser for knowledge workers, and is set to release its first-quarter fiscal 2026 earnings report on October 30.

- This move highlights Atlassian’s ongoing investment in AI innovation, which may enhance its competitive positioning in the enterprise software sector.

- Next, we'll examine how the addition of AI-powered browser capabilities could influence Atlassian's investment narrative and growth prospects.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Atlassian Investment Narrative Recap

Atlassian investors often share a belief in the company's ability to drive long-term growth through deepening enterprise cloud adoption and product innovation, particularly in AI. The recent acquisition of The Browser Company of New York Inc. is a visible step in this direction, though the most immediate catalyst remains the Q1 FY2026 earnings report and the ongoing pace of cloud migrations; this development does not materially change near-term risks, which are still centered on complex enterprise migrations and effective go-to-market execution.

Of this month's company news, the multi-year partnership with Google Cloud stands out in the context of Atlassian's AI and cloud ambitions. This collaboration could accelerate the rollout and integration of AI-powered features, supporting the thesis that differentiated AI functionality will increase user engagement and help drive premium upsells, a core long-term growth lever highlighted by management and analysts alike.

But while expectations for new AI solutions are high, investors should also keep an eye on the ongoing challenge of persuading large enterprise customers to...

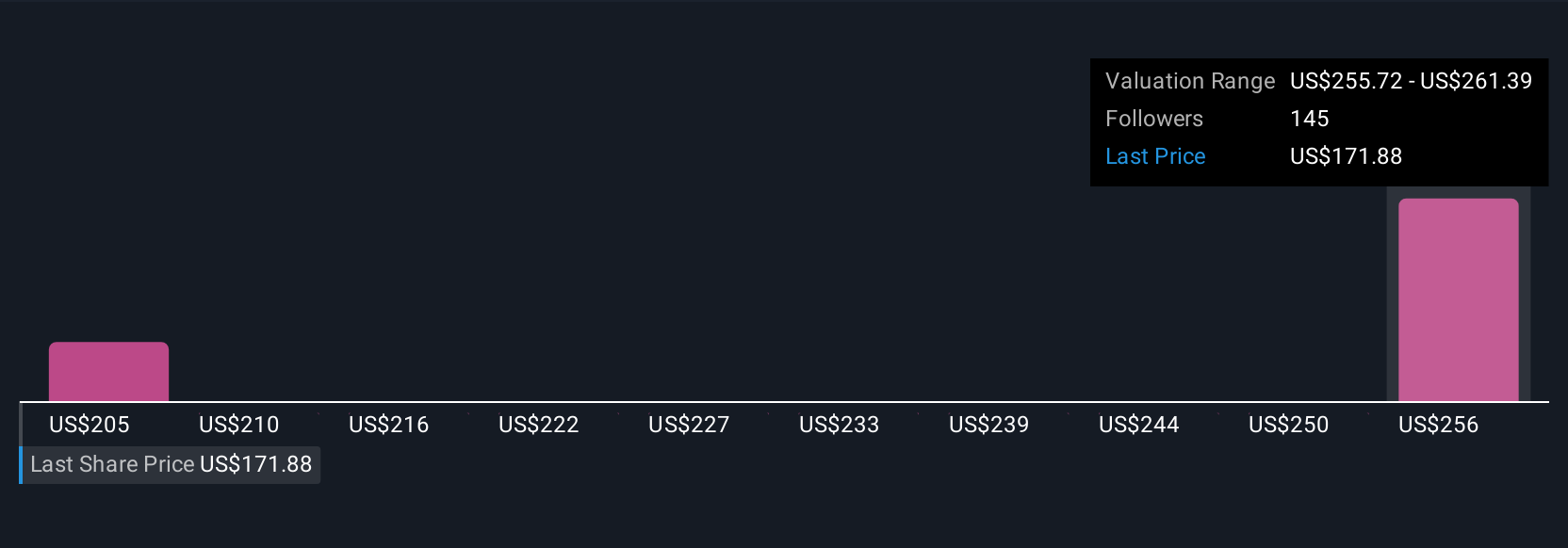

Atlassian's outlook anticipates $8.7 billion in revenue and $310.2 million in earnings by 2028. This scenario implies 18.7% annual revenue growth and a $566.9 million increase in earnings from the current level of -$256.7 million.

Uncover how Atlassian's forecasts yield a $249.51 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided 9 separate US$ fair value estimates for Atlassian, spanning US$201.40 to US$279.41 per share. Against this backdrop, the focus on accelerating cloud migration and AI-powered user growth continues to shape wider debate about Atlassian’s future earnings potential.

Explore 9 other fair value estimates on Atlassian - why the stock might be worth just $201.40!

Build Your Own Atlassian Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Atlassian research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Atlassian research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Atlassian's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.