How Attractive Is ZIM Integrated Shipping Services (ZIM) After Recent Share Price Volatility

ZIM Integrated Shipping Services Ltd. ZIM | 26.30 | +1.35% |

- If you are wondering whether ZIM Integrated Shipping Services is priced attractively or not, you are not alone. The stock has caught a lot of attention from investors trying to work out what a fair value looks like.

- The share price last closed at US$20.73, with returns of a 4.7% decline over 7 days, a 7.5% decline over 30 days, a 5.4% decline year to date and a 29.2% gain over the past year. The 3 year return is 121.7% and the 5 year return is 304.7%.

- Recent headlines around ZIM have focused on shipping sector sentiment, industry freight rate trends and how container liners are handling changing global trade flows. These stories give useful context for the share price moves, especially for investors asking whether current expectations are already reflected in the stock.

- On our valuation checks, ZIM scores 4 out of 6 for being undervalued. This sets up a closer look at how different valuation approaches line up and hints at an even more helpful way to think about value that we will come back to at the end of this article.

Approach 1: ZIM Integrated Shipping Services Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company might be worth by projecting its future cash flows and discounting them back to today, so you can compare that value with the current share price.

For ZIM Integrated Shipping Services, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow stands at about US$2.89b. Looking ahead, the projections used in this model show free cash flow of US$731m in 2026 and US$626m in 2027, with further yearly figures out to 2035 extrapolated from these inputs by Simply Wall St.

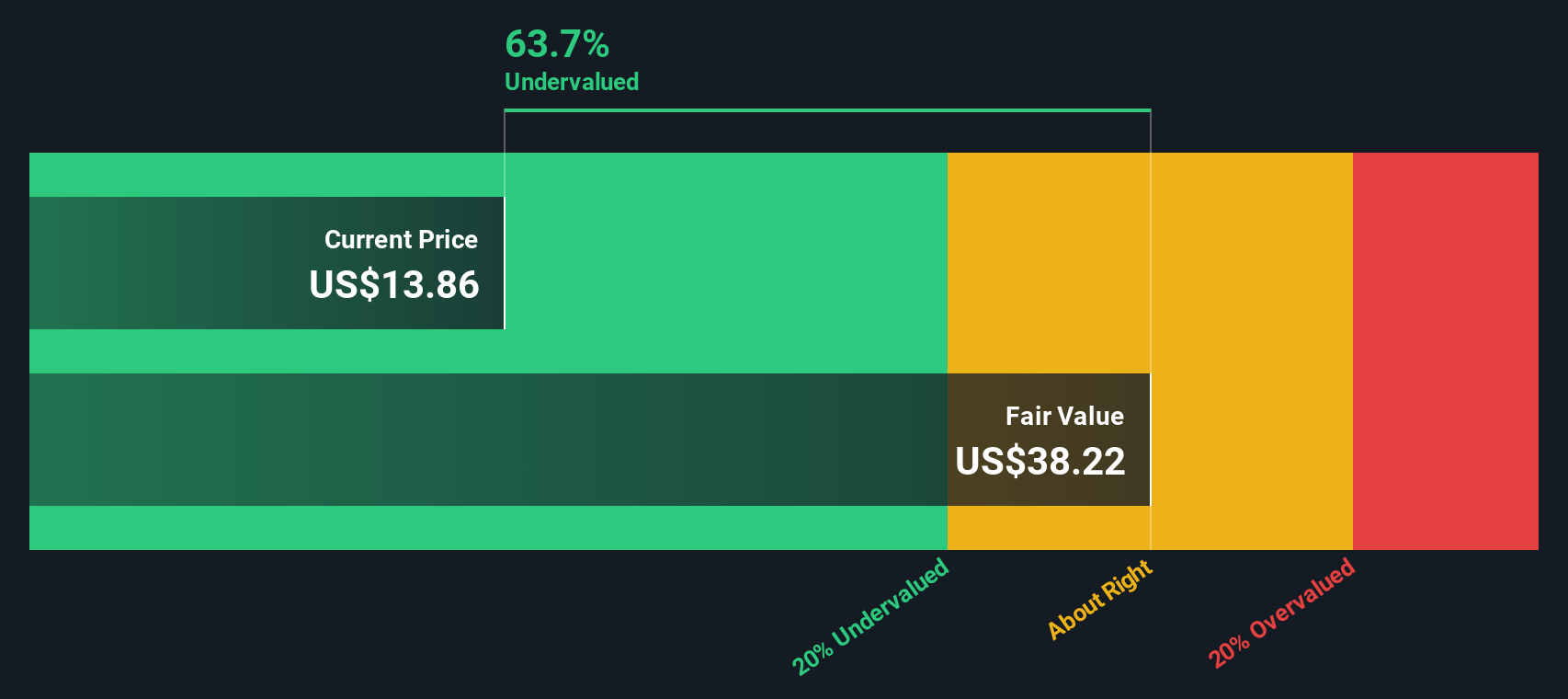

Bringing all those projected cash flows back to today gives an estimated intrinsic value of US$37.36 per share. Compared with the recent share price of US$20.73, the DCF output implies the stock trades at roughly a 44.5% discount, which indicates that, on this model alone, ZIM appears to be undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ZIM Integrated Shipping Services is undervalued by 44.5%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

Approach 2: ZIM Integrated Shipping Services Price vs Earnings

P/E is a common way to value profitable companies because it links what you pay for each share to the earnings that business is currently generating. In general, higher expected growth or lower perceived risk can justify a higher P/E ratio, while lower growth expectations or higher risk tend to be associated with a lower, more cautious P/E.

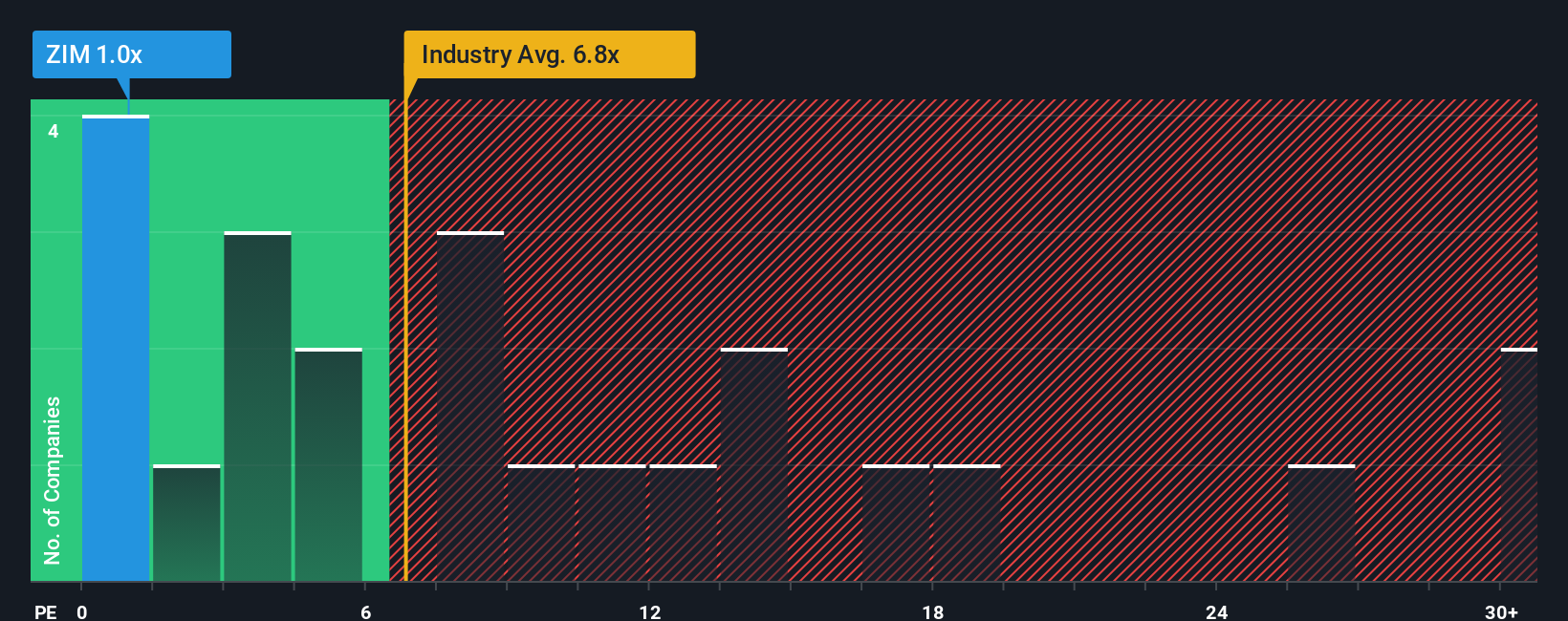

ZIM Integrated Shipping Services currently trades on a P/E of 2.49x. That sits well below the Shipping industry average P/E of 10.17x and the broader peer group average of 16.42x. On these simple comparisons alone, the shares look inexpensive relative to many listed shipping names.

Simply Wall St also calculates a Fair Ratio, which here is 0.76x. This is a proprietary estimate of what a more tailored P/E might look like after considering factors such as the company’s earnings profile, its industry, profit margins, market capitalization and specific risks. Because it adjusts for these elements, the Fair Ratio can give a more nuanced anchor point than raw peer or industry averages. Comparing the Fair Ratio of 0.76x with the current P/E of 2.49x suggests the stock is trading above this tailored reference level, indicating it screens as overvalued on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your ZIM Integrated Shipping Services Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simple stories that you or other investors attach to the numbers, linking your view of ZIM Integrated Shipping Services’ business, its future revenue, earnings and margins to a financial forecast and a fair value that you can compare directly with today’s share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. Each Narrative sets out assumptions and a resulting fair value, then continuously updates as new information like news or earnings is added. This allows you to see in real time whether your fair value is above or below the current price and to decide whether that means ZIM is a potential buy, a hold, or something you might sell.

For ZIM, for example, one Narrative on the platform currently anchors on a fair value around US$452.35 per share, while another sits closer to US$9.80. This shows how two investors can look at the same company, build very different stories from the same data, and reach sharply different conclusions about what the stock is worth today.

For ZIM Integrated Shipping Services however we will make it really easy for you with previews of two leading ZIM Integrated Shipping Services Narratives:

Fair value in this Narrative: US$452.35 per share

Implied discount to this fair value: about 95% based on the last close of US$20.73

Revenue growth assumption: 55%

- Frames the Panama Canal bottleneck as an overplayed risk and highlights recent rainfall data that supports a more constructive view on shipping routes.

- Points to ZIM's limited share count of about 220 million as a key reason the author believes total returns can be sustainable.

- Argues that ZIM is insulated from broader international stagflation concerns, linking this view to currency moves and comparisons with other shipping and commodity names.

Fair value in this Narrative: US$13.78 per share

Implied premium to this fair value: about 50% based on the last close of US$20.73

Revenue growth assumption: 14.57% decline

- Highlights pressure on China U.S. trade, industry overcapacity and a charter heavy fleet as key risks for revenue and margin stability.

- Uses analyst assumptions for shrinking profit margins and revenue to arrive at earnings forecasts and a higher future P/E multiple, then discounts these back to a present value.

- Notes that while there are potential positives around fleet modernisation, new trade lanes, digital tools and LNG vessels, the base case Narrative sees these as insufficient to offset earnings and valuation headwinds in the near term.

Do you think there's more to the story for ZIM Integrated Shipping Services? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.