How Avista’s Stronger Q1 EPS and Maintained Dividend Will Impact Avista (AVA) Investors

Avista Corporation AVA | 0.00 |

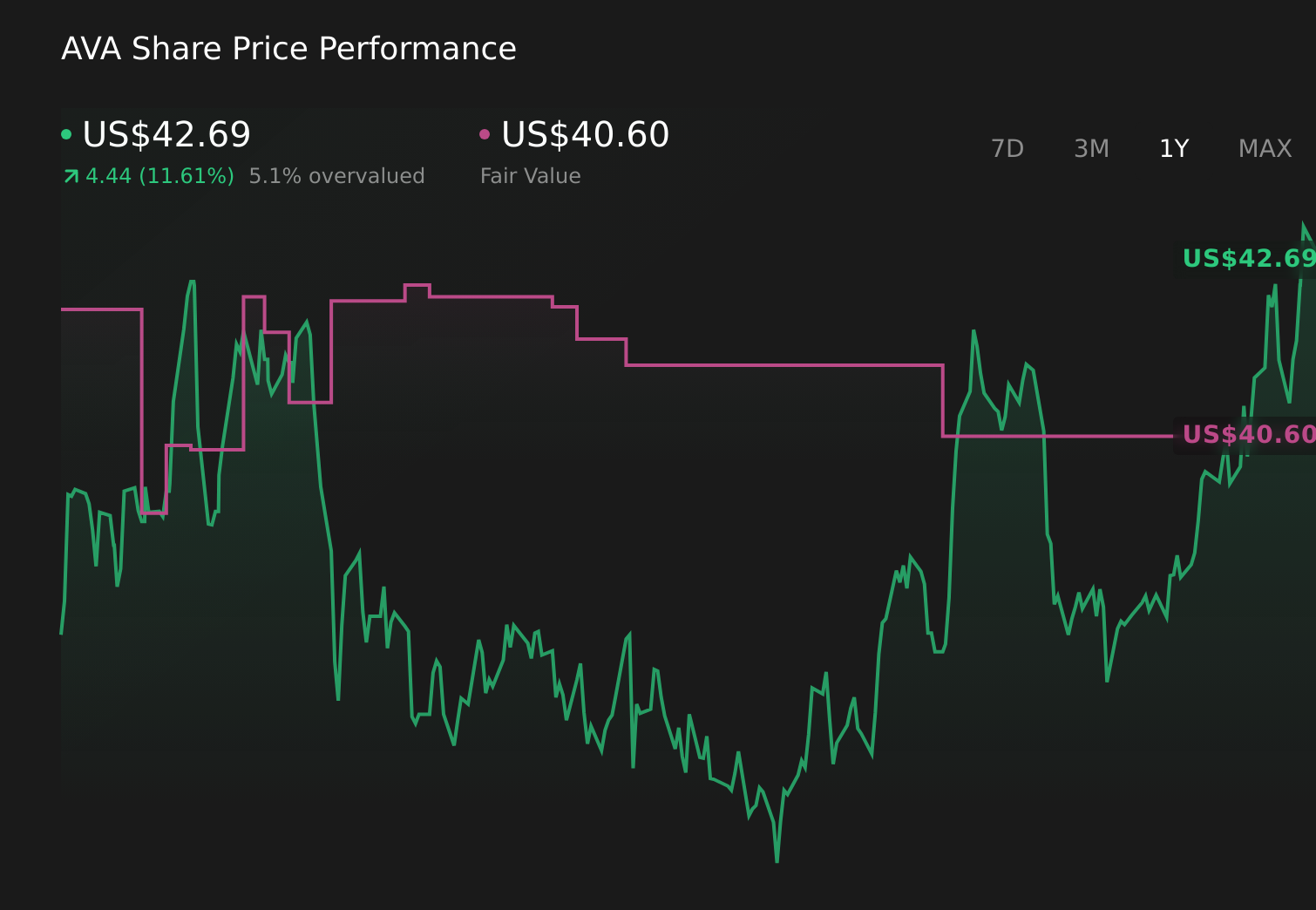

- Avista Corporation recently reported past first-quarter 2026 results, with revenue of US$570 million versus US$617 million a year earlier, while net income rose to US$92 million and diluted EPS reached US$1.11 from US$0.98, alongside announcing a quarterly dividend of US$0.4925 per share payable on June 12, 2026.

- The combination of higher earnings despite lower revenue and the continued dividend payout highlights Avista’s ability to support shareholder returns while managing operational efficiency.

- We’ll now examine how Avista’s stronger first-quarter profitability and affirmed dividend policy influence the company’s broader investment narrative and outlook.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Avista Investment Narrative Recap

To own Avista, you need to be comfortable with a regulated utility focused on steady earnings, heavy capital needs, and regional regulatory oversight. The latest quarter showed higher earnings on lower revenue and an affirmed dividend, but this does not materially change the key short term catalyst of large load growth opportunities, nor the biggest near term risk around rising capital spending and the ability to recover those costs through regulators.

The most relevant recent development here is Avista’s first quarter 2026 result, where net income rose to US$92 million and diluted EPS reached US$1.11 despite revenue declining to US$570 million. That mix of margin strength and continued dividend payments sits alongside a multi year, roughly US$3 billion capital program, which keeps the spotlight firmly on regulatory outcomes and how effectively Avista can translate new investment into allowed returns.

Yet behind the steady dividend, investors should be aware of how rising grid and wildfire investments could strain cash flows and...

Avista's narrative projects $2.2 billion revenue and $253.4 million earnings by 2029.

Uncover how Avista's forecasts yield a $42.80 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Two members of the Simply Wall St Community currently see Avista’s fair value between US$35.94 and US$42.80, underlining how far opinions can differ. When you set those views against the company’s growing capital expenditure needs and dependence on constructive regulatory outcomes, it becomes even more important to compare several perspectives before deciding how Avista might fit in your portfolio.

Explore 2 other fair value estimates on Avista - why the stock might be worth 12% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Avista research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.