How Bank of America’s Earnings Beat and Policy Pressures Could Reshape BAC’s Investor Narrative

Bank of America Corp BAC | 49.38 | +0.22% |

- In recent days, Bank of America reported fourth-quarter results that surpassed analyst expectations and continued to roll out new fixed‑income offerings and preferred dividends, while also extending partnerships such as its Volvo Car Financial Services financing agreement through 2030.

- At the same time, the bank is weighing 10% interest‑rate credit cards under political pressure and committing fresh employee and child savings support via Trump accounts, underscoring how regulation, policy and product design are increasingly shaping its business mix.

- Next, we’ll examine how Bank of America’s strong earnings beat, alongside cautious operating leverage guidance, is influencing its broader investment narrative.

We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

What Is Bank of America's Investment Narrative?

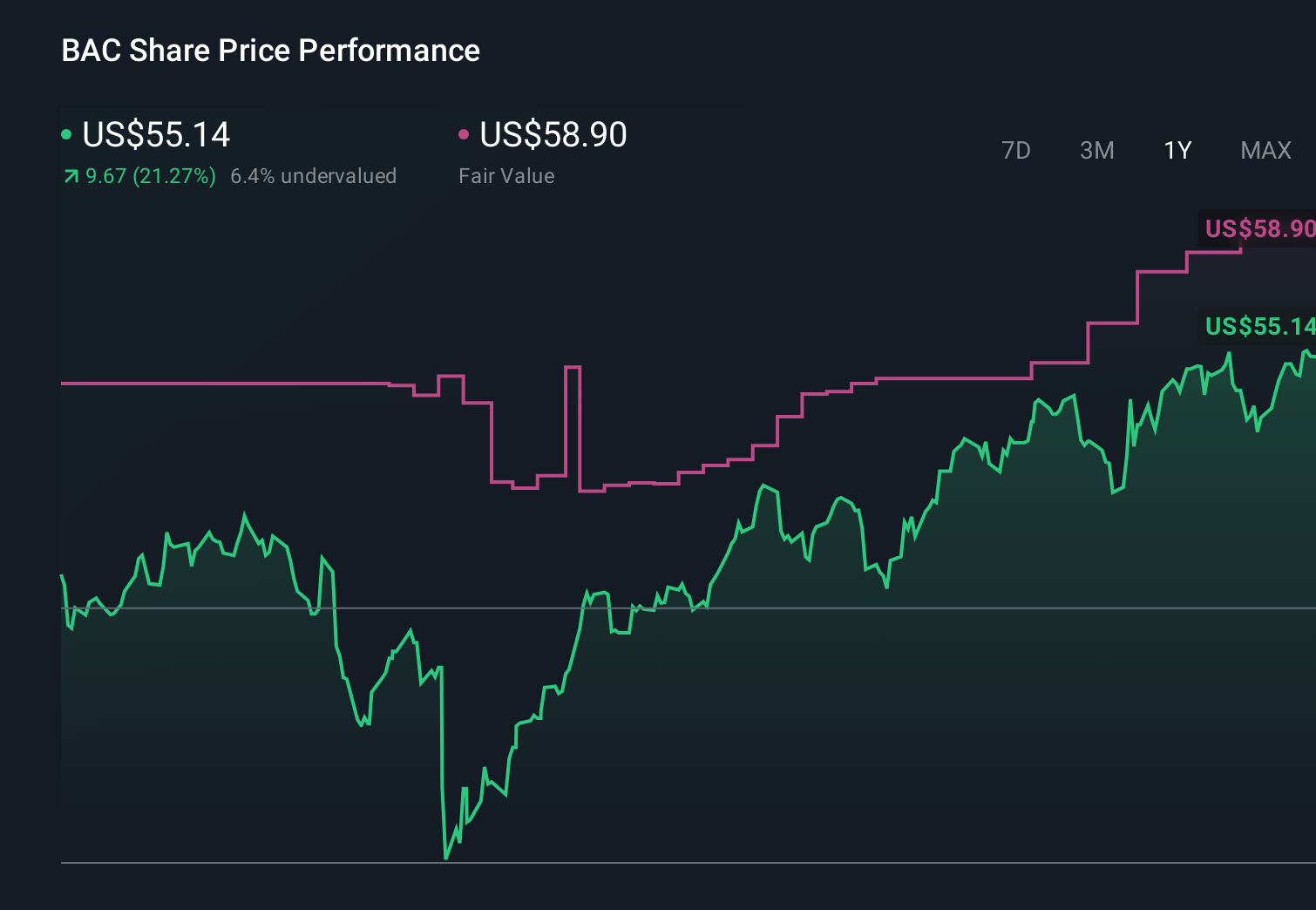

To own Bank of America today, you need to be comfortable with a large, slower‑growing franchise that leans on scale, net interest income and steady capital returns rather than rapid expansion. The recent earnings beat reinforces that core story, but the stock’s 2% pullback and modest year‑to‑date decline suggest investors are questioning how much operating leverage is left in the near term. The flurry of new senior note issuances and ongoing preferred dividends look like routine balance sheet and capital management, so they do not obviously alter the short‑term thesis. What could, however, is the bank’s response to political pressure on credit card pricing and its participation in Trump accounts, which bring regulatory and reputational risk closer to the center of the investment case.

However, the potential credit card rate cap is a shift investors should not ignore. Despite retreating, Bank of America's shares might still be trading 17% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Seventeen members of the Simply Wall St Community currently see Bank of America’s fair value spanning roughly US$43 to just under US$63 per share, reflecting very different expectations. Set against recent earnings strength but softer operating leverage guidance and rising regulatory pressure on consumer lending, this spread underlines why it can be worth weighing several viewpoints before deciding how the story fits your own portfolio.

Explore 17 other fair value estimates on Bank of America - why the stock might be worth 16% less than the current price!

Build Your Own Bank of America Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.